How hard is it to generate returns from an assured interest fixed-income investment? So, you just invest some amount for a few years, enjoy an assured interest and get your principal back at the end of the tenure, right?

Well, not quite. From defaults and downgrades that impacted your debt funds to sharply reduced interest rates in small savings instruments, your fixed-income portfolio has been facing some tough headwinds.

But there are ways to build your portfolio smartly and use debt securities to not only guarantee you a fixed income, but also minimise volatility. To make things simple, we have curated fixed income strategies for three broad classes of investors – senior citizens (above the age of 60), the 50s age group (these are approaching their retirement), and the rest. The latter category could comprise those in their 20s, 30s or even 40s.

Senior citizens: Safety firstRetired and with no pension or professional income, you need a monthly inflow that is preferably assured. Volatility is best avoided. Some of you may be in the higher tax bracket, others could be in the lower slabs. Interest rates have shrunk. What should you do in such a scenario?

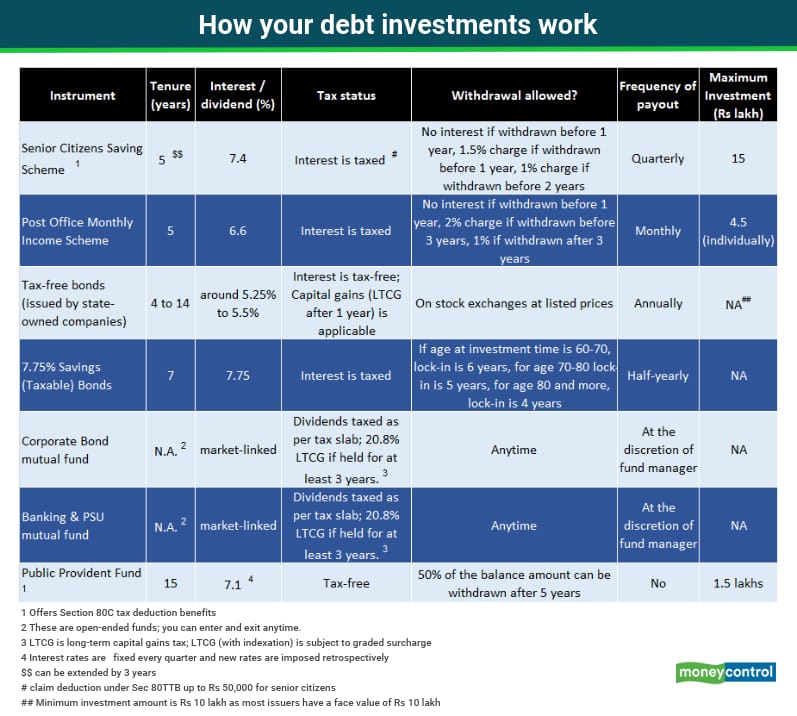

Start with the Senior Citizen Saving Scheme (SCSS). Despite the cut in rates (7.4 percent; down from 8.6 percent earlier), SCSS remains, arguably, your best option as it comes with a government guarantee. A basis point is one-hundredth of a percent point. You can invest a maximum of Rs 15 lakh in your name; maximise this. “The government will never go belly up, so the chances of default are nil,” says Suresh Sadagopan, Founder of Ladder7 Financial Advisories. Its tenure is five years and pays quarterly interest.

Your second option ought to have been Pradhan Mantri Vaya Vandana Yojana – a 10-year senior citizen scheme. Unfortunately, investments were barred from March 31, 2020. But keep an eye out on this scheme. With several tax-related and regulatory deadlines extended to help citizens tide over the COVID-19 crisis, this scheme could get an extension. It aimed to give regular interest payouts monthly, at eight percent.

Next in line is the 5-year post office monthly income scheme (POMIS). With an interest rate of 6.6 percent, it still beats bank FDs on returns – a five-year State Bank of India FD gives you six percent interest. You could invest a maximum of Rs 4.5 lakh in the scheme in a single account and Rs 9 lakh in a joint account.

Not all advisors suggest POMIS though. “A post office is not available at all locations, especially one that allows you to make investments. But it’s always easy to find a bank branch in your locality,” says Jitendra Solanki, Founder of Plan Special Needs. Poor service standards are a problem as well. Besides, you need to open a savings account also for your POMIS interest to get credited in it.

For those in the higher tax brackets, advisors often suggest tax-free bonds available on the stock exchanges. “With a post-tax yield of 5.25 percent to 5.50 percent, it is better than even the SCSS, if you are in the higher tax brackets,” says Vikram Dalal, founder and managing director, Synergee Capital Services. Or, if you are in the low tax brackets, go for the RBI 7.75 per cent Savings (Taxable) Bonds. Although the interest is taxable, it won’t add a burden to those in the lower tax brackets.

Both are safe; state-owned companies issue tax-free bonds, so there is an implicit government guarantee and the RBI’s 7.75 percent bonds carry the highest safety.

You’re approaching retirement, but not quite there. You are at the peak of your career. Because you are still earning, you don’t need regular income from your investments. Some risk is fine since you are still a few years away from retirement. But since you still need better tax-adjusted returns.

Try debt mutual funds, especially corporate bond funds and banking & PSU schemes. These invest in high-quality debt instruments, so the chances of credit accidents are minimal. Start a systematic investment plan to deploy sums every month, till you retire. After 60, you can opt for a systematic withdrawal plan to get yourself a regular income from it.

Presently, since you do not need regular income, you can also afford to lock away your money in a slightly high-yielding instrument. Suresh also recommends fixed maturity plans or a corporate fixed deposits, though most planners these days, including Suresh, prefer to stick to HDFC Ltd’s FD due to its high pedigree. Flexible tenures (33 and 66 months) are an added advantage. Returns here are higher than bank FDs as well as the National Saving Certificate – a five-year post office savings instrument that now gives you 6.8 percent interest.

That brings us to a critical question. How much returns should you expect from a debt instrument? Ashish Shah, founder of Wealth First says: “Investors should only expect inflation plus 1.5 percent points return from their fixed income investments and nothing more. Inflation these days is around 4.5 percent to five percent. So a return of around 6.5 percent today from your debt instruments should suffice. You should feel happy,” he adds.

Avoid credit risk funds; they’ve become too unsafe. A March 3 report by India Ratings & Research said that 16 percent of the domestic corporate debt is vulnerable to default over the next three years. This prediction was made before the full-blown impact of the COVID-19 induced stress on industries and companies.

Don’t forget your equity investments here. If you have too much of equity funds, then switch a portion to debt (preferably debt MFs) in your 50s. As you approach your retirement, you need to increase the safety quotient in your portfolio.

The rest: Debt plays a supporting roleYou are building your wealth for your retirement, and various other goals such as buying a house, securing your children’s future as well as for short-term goals such as buying a car or going on a holiday. You do not need liquidity from your debt instruments because, as Suresh says, “they would yield nominal income that would land up in your bank account, you wouldn’t even come to know and you’d spend it.” In your 20s, 30s and even 40s, your equity allocation will be higher than in debt.

But there is still room for your fixed-income instruments. Continue with your Employer’s Provident Fund contribution; you can even increase your own contribution. The Public Provident Fund (PPF) still remains one of the best long-term debt instruments for this age group, with 7.10 percent interest and a tax-free status. And you can maximise your section 80C investments between EPFO and PPF. Use these as your compulsory long-term savings meant for your retirement. You can also invest in the National Pension Scheme and get tax deduction benefits.

Use shorter tenured debt funds and even corporate bond and Banking & PSU schemes if you are saving up for the next 2-4 years.

More importantly, focus on your asset allocation at this stage of your life. Depending on how much risk you wish to take, strike a balance between equity and debt. While equities should be used for long-term wealth creation, debt is your safety net that earns you stable returns.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.