India is gearing up for the Union Budget 2026, to be presented on Sunday, February 1. Ahead of the announcement, Finance Minister Nirmala Sitharaman has begun pre-budget consultations with states and UTs.

As she prepares her ninth consecutive budget, here’s a recap of income tax slabs announced in previous budgets, and the current tax slabs under the old and new tax regimes.

Remember, old tax regimes offer various tax deductions and exemptions, though the new tax regime is attractive for lower tax rates and a higher basic exemption limit.

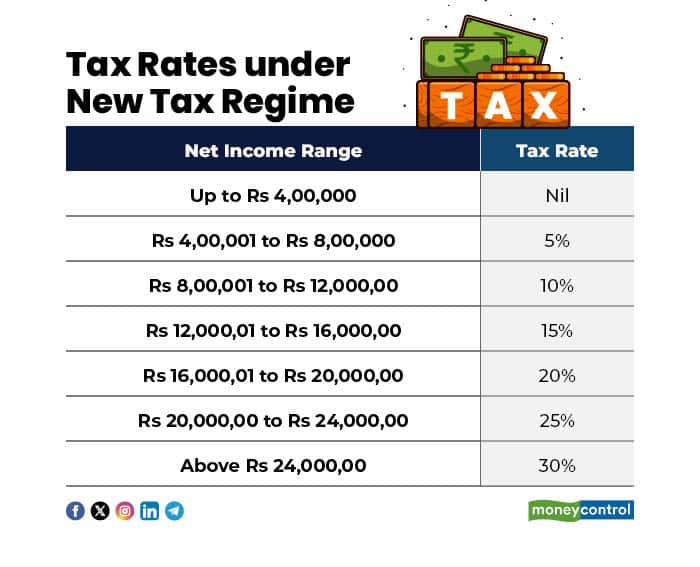

New Tax Regime

The Union Budget 2020 introduced the new tax regime under Section 115BAC of the Income Tax Act, effective from the financial year 2020–21, offering taxpayers an alternative to the existing old tax regime.

In the Union Budget 2023, the new tax regime was made the default option, particularly for new taxpayers, unless they specifically chose the old regime. The Budget also increased the basic exemption limit from Rs 2.5 lakh to Rs 3 lakh and raised the income threshold for claiming a full tax rebate under Section 87A to Rs 7 lakh. Additionally, the standard deduction was enhanced to Rs 50,000 for both salaried individuals and pensioners.

Further strengthening the regime, the Union Budget 2025 increased the standard deduction to Rs 75,000 and raised the basic exemption limit to Rs 4 lakh.

Currently, the new tax regime applies as the default option for individuals as well as Hindu Undivided Families (HUF), Associations of Persons (AOP), Bodies of Individuals (BOI), and Artificial Juridical Persons (AJP) of all ages.

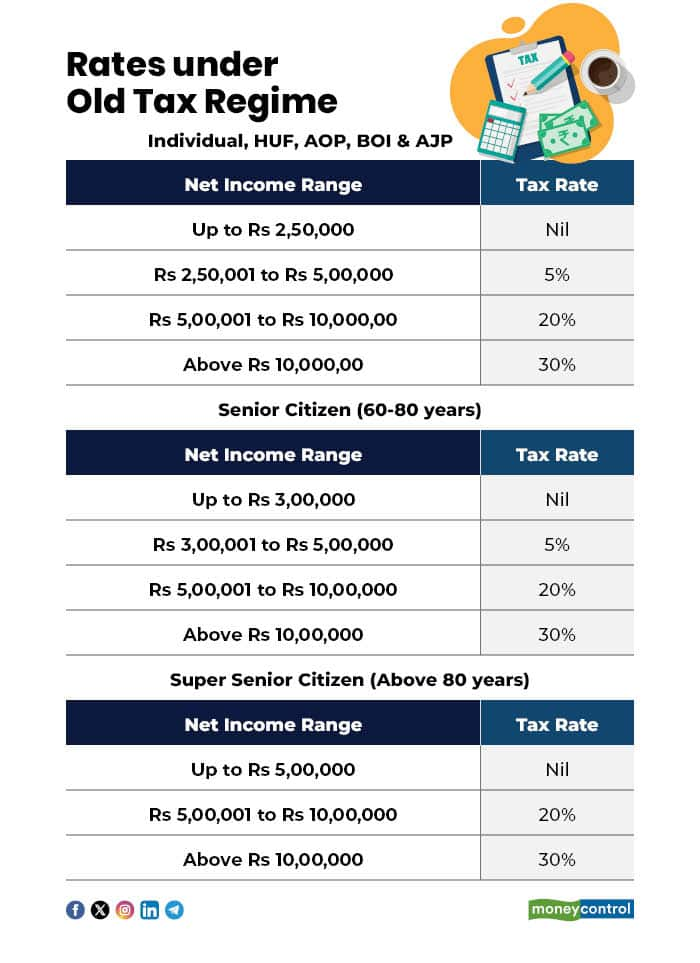

Old Tax Regime

Taxpayers choose to remain within the old tax regime to avail of over 70 deductions and exemptions under various sections of the Income Tax Act. Taxpayers who are enrolled under the default new tax regime can choose to return to the old tax system as per Section 115BAC(6) of the Income Tax Act.

Rates are generally high under the old tax slab as compared with the new tax regime. Taxpayers must carefully analyse their exemptions and deductions before choosing to return to the old tax regime.

Unlike the new tax regime, which has introduced a fixed rate for all age-groups, the old tax regime has separate tax slabs for individuals up to 60 years of age, senior citizens (60-80 years), and super senior citizens (above 80 years).

Here are the latest rates under the tax regime for individuals (Hindu United Family, Associations of Persons, Bodies of Individuals, and Artificial Juridical Persons), senior citizens and super senior citizens.

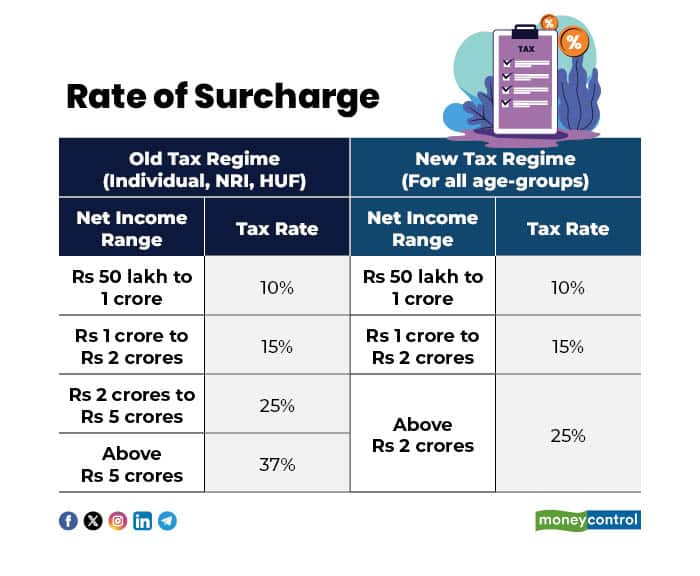

Surcharge for Old and New Tax Regime

The Government of India imposes an additional surcharge on individual taxpayers, regardless of age, whose annual income exceeds Rs 50 lakh. Under the new tax regime, the maximum surcharge for individuals earning more than Rs 5 crore is capped at 25 percent, while the old tax regime levies up to 37 percent.

With Budget 2026 nearing, having clarity on existing income tax slabs is essential for effective financial planning. Taxpayers should carefully compare deductions available under the old regime with the lower rates and higher exemptions offered by the new regime to determine the most suitable option.

Read more: Latest update on Budget 2026.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.