The GDP (gross domestic product) and GVA (gross value added) back data reported last week removes the niggling question of non-comparability of the past series. With comparable data now available, some interesting but rather disturbing trends come to light. It was earlier believed that the real GDP growth was higher during the UPA regimes pre-2014 and that the domestic economy remained largely insulated from the global recession in 2009. But the new numbers now reflect a much greater impact on domestic growth during that period.

With comparable data now available for past years, we observed that the growth in real GDP has been noticeably higher in the last 4 years, than the growth during 2006-2014. Though the nominal GDP throws a different picture showing a higher growth in the earlier years, we believe this was majorly accountable to a high inflation.

GDP higher post-2014, what about corporate performance?Curious about whether this corroborates with the earnings and profitability of corporate India, we analysed the long-period annual data of growth of GDP and GVA as well as corporate performance of listed companies to gauge the correlation between the two. While there appears to be a strong correlation between the growth in GVA/GDP and growth in sales of India Inc, there exists a much weaker correlation with corporate profitability.

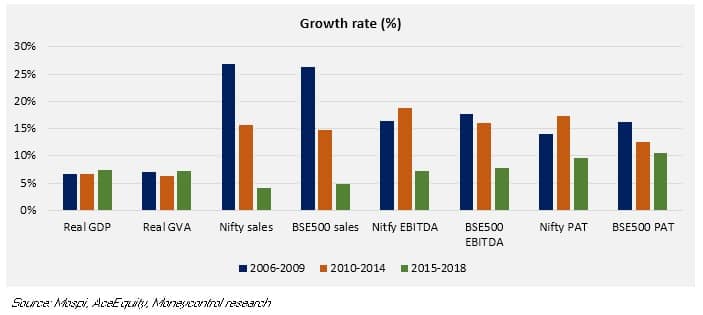

We observed that the real GDP growth had improved in the last 4 years going up from an average 6.7 percent in 2006-2014 to 7.3 during 2015-2018. However, the sales growth of India Inc had seen a sharp slowdown during this period. From a high of 20.6 percent growth in 2006-2014 it has fallen to a mere 4.3 percent during 2015-2018. Though still correlated, we observed that the correlation coefficient has gone down in recent times. Moreover, the growth in operating and net profits of corporates has also declined sharply in the last 4 years.

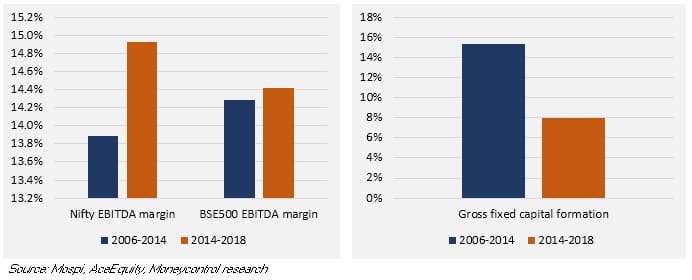

However, operating margins have improved during 2014-2018. At the same time, growth in gross fixed capital formation in the economy has gone down from 15.4 percent during 2006-2014 to 8 percent in 2015-2018 period. This means the overall productivity has improved in the economy, which can be attributed to numerous external factors.

Our analysis across sectors suggests that most companies resorted to cost management to stay afloat in a challenging macro environment, which improved margins. Better productivity in recent years could also be attributed to lower input costs as commodity prices were soft between 2014 and 2018. Barring the recent spike, crude oil prices remained low during the last 4 years, thereby reducing input costs for companies and leading to improved margins. Technological advancements (including labour saving technologies) also enabled companies to save up on costs.

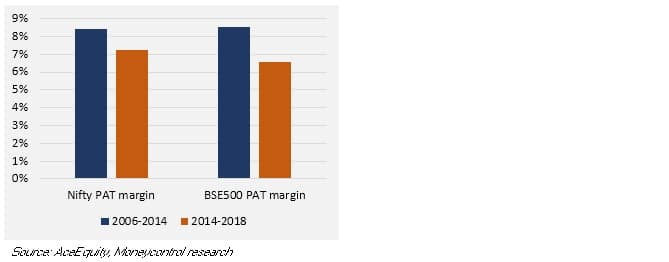

Another interesting observation was that while the operating margins have improved, the net margins have contracted. This highlights increasing interest cost for companies which is impacting net profitability. Also, debt to equity ratio has risen in the last 4 years for both Nifty and BSE500 companies. While the uptick in debt equity is only marginal, the contraction in net profits is much aggravated, indicating that incremental capital is coming at a higher cost for companies?

Comparing the GDP series with other macro variables throws some interesting insights as well. Over the years, the growth in bank credit has gone down substantially. This points towards greater access to alternate capital sources for businesses.

A sector-wise analysis of the long-term data shows that while there was little slowdown in most consumer sectors, the overall slow growth was essentially due to a sharp slowdown in agriculture, mining and construction. Agriculture has fallen sharply in the later years, which might be a worrisome trend, given the agri dependency of our economy.

OutlookWhile fundamentally GDP should reflect the gross produce in the economy and corporate earnings should move in tandem with the GDP of the economy, the weakening correlation reflects limitations in the GDP coverage. Moreover, a revised series now shows that Indian economy never went through the double-digit growth phase. Steep contraction in economic growth during years of global recession comes as a warning that the domestic economy is not so much insulated from the vagaries of world economics.

The improved GDP performance in 2014-2018 period was is in sharp contrast to the muted trend in corporate India’s earnings performance. In fact, the better operating result was aided by low commodity, crude and input costs which enabled a margin growth for Indian corporates and does not necessarily reflect an improvement in the business environment.Follow @RuchiagrawalFollow @krishnakarwa152For more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!