Highlights: - Muted overall volume growth in Q4 FY19 driven by decline in scooter and Moped volumes - Improved realisation led by price hike, rich product mix and weakening of rupee - Business outlook for 2W segment is weak in the short-term, positive for long-term - 3W continues to show strong momentum - Priced to perfection --------------------------------------------------

TVS Motor (TVS) (CMP: Rs 486.00, Mcap: Rs 23,090 crore) posted better-than-expected set of numbers driven by improved realisation. Operating margin remained stable in the environment of rising raw material (RM) prices.

Despite its strong position in the domestic market, we have a neutral stance on the company. This is, primarily because the share price is priced to perfection (27.4 times FY21 projected earnings) and hence valuation leaves little room for comfort.

Quarter in numbers:

Key positives

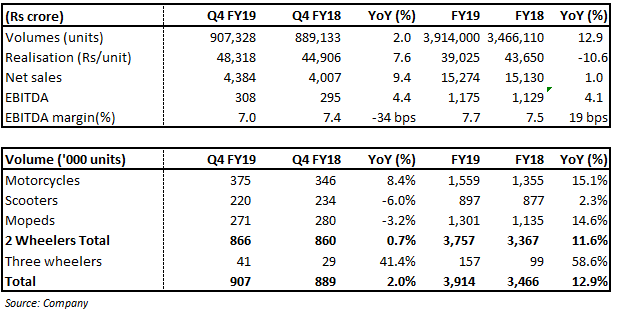

Volume – motorcycle and three-wheeler witnesses growth In Q4 FY19, TVS posted a year-on-year (YoY) volume growth of 2 percent driven by 8.4 percent YoY growth in motorcycles, which got offset by a 6 percent and 3.2 percent decline in scooters and mopeds volume, respectively. Three-wheeler (3W) continued to post a stellar show with volume showing YoY growth of 41.4 percent on the back of strong demand after the end of Raj Permit. In terms of exports, TVS posted a volume growth of 22 percent (YoY).

Improved realisation Overall realisation improved 7.6 percent (YoY) led by rich product mix, multiple price hikes taken by the company to pass on the rise in RM prices and higher export revenue due to weakening of rupee.

Volume growth and improvement in realisation led to 9.4 percent YoY growth in net revenues for the company.

Key negatives RM prices continue to exert pressure on the profitability of the company and hence earnings before interest, tax, depreciation and amortisation (EBITDA) margin witnessed marginal blip of 34 bps YoY. EBITDA margin for the company continues to be much lower than the double-digit margin guidance given by the management.

Outlook

2W industry outlook sluggish in near term The short-term outlook for overall two-wheeler industry continues to be sluggish on the back of muted consumer sentiments driven by restricted availability of retail finance, higher interest rates and higher insurance cost.

The environment for two-wheeler segment in India would continue to be challenging and would witness flat volume growth in the first half of FY20. However, second half of FY20 is expected to be strong.

Management of TVS cited pre-buying ahead of BS VI implementation, possibility of good monsoon, good festive season and reduction in the interest rate as the key trigger for the industry.

In the long-term, we, however, believe, there is a huge potential for two-wheelers in India and strong demand is expected to come from both rural and urban areas on the back of very low penetration and rising disposable income. It is expected to get a boost from rural market led by government's focus on rural areas and increase in minimum support price (MSP).

Strong 3W market The overall three-wheeler market continues to gain strength after the end of the Raj Permit. This has led the company to post strong volume growth in the segment. We believe TVS would continue to perform well in this space.

Improving export markets The overall export markets seem to be stabilising and benefiting TVS as is evident from its quarterly volume numbers. Weakening of rupee is also aiding growth for the company.

Currently, TVS caters to 62 countries and has been gaining significant market share there. In fact, it has been outperforming industry growth in those markets, primarily, due to its product range.

Operating margin – far away from double-digit guidance EBITDA margin continues to be under pressure primarily due to RM prices and increasing competitive intensity. The company is still far away from its target of achieving double-digit EBITDA margin. The management has highlighted that new launches, strong traction in export market and cost efficiencies would help the company achieve its target.

Valuation continues to be at elevated levels Despite 30 percent fall in stock price from its 52-week high level, the valuation of TVS continues to be at elevated levels. The company is currently trading at 27.4 times FY21 projected earnings, which leaves little room for comfort.

For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!