Sreeleathers (market cap: Rs 564.5 crore) is a Kolkata-based manufacturer cum retailer of footwear and leather products. Though eastern and central states of India are Sreeleathers’ primary markets, of late, the company seems to be building its presence in northern India.

The company’s impressive performance in the quarter gone by was attributable to sales growth on the back of a low base (demonetisation in Q3FY17) and network augmentation, operating leverage, and reduced dependence on debt for business operations.

As seen in the exhibits below, though sales from a company-specific perspective over a period of time is a function of numerous factors (such as seasonality, number of outlets, realisations per unit, quantity sold etc), Sreeleathers has clearly been way ahead of the competition in terms of margins.

Unlike most other footwear players, Sreeleathers hasn’t altered its business model significantly by venturing into markets across India. The company continues to capitalise on its strengths by adding new outlets mainly in its target markets. Consequently, economies of scale can help boost operating margins.

In a bid to achieve higher returns on capital employed, Sreeleathers’ plans for the upcoming fiscals entails signing up with more franchise partners to enhance its distribution channels effectively, particularly in Uttar Pradesh and Delhi.

Operating leverageSreeleathers is unlikely to change its tried and tested strategy of laying impetus on volume-driven sales growth in price-sensitive tier 2/3/4 territories. Furthermore, in the long-run, the company’s plan entails outsourcing a higher share of manufacturing activities to third-party vendors as well.

GST benefitIndia’s footwear industry is significantly led by the unorganised sector, that constitute nearly 70-80 percent of the overall size. Post-GST, transition of market share in favour of organised entities augurs well for Sreeleathers in due course. From the company’s standpoint, the GST rates are pretty tax-neutral too.

Should you invest?In spite of the tailwinds stated above, unresolved GST-related teething issues at the small dealers’ end could play spoilsport. Secondly, an increase in raw material prices could impact margins since it’ll be hard for the company to pass on the entire price increase to its target audience (aspirational customers).

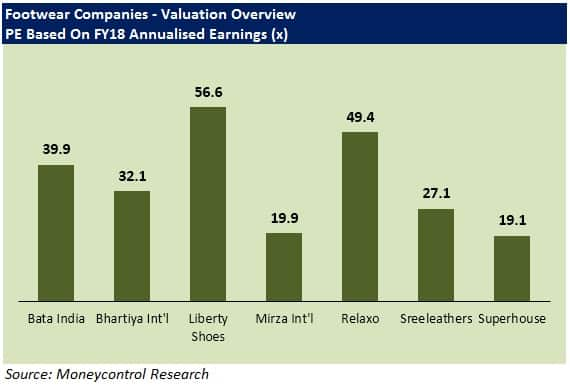

Despite a sharp rally in the stock’s price over the past three months, the stock, valued at 27.1x FY18 annualised earnings, trades at a steep discount to industry leaders such as Bata and Relaxo. Therefore, investors shouldn’t overlook this opportunity.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.