Nitin Agrawal Moneycontrol Research

Motherson Sumi Systems (MSSL), India’s largest automotive wiring harness company and one of the largest auto ancillary players, posted a disappointing set of Q2 FY19 earnings on the back of a demand slowdown in international markets and contraction in margins for Samvardhana Motherson Peguform (SMP) and its India business.

The new plants are being commissioned and that should result in increasing revenue and operating leverage. This, coupled with the push towards electric vehicles (EVs), should result in healthy topline growth and gradual increase in margin. MSSL is currently trading at a reasonable valuation, which warrants investor attention.

Quarter in a nutshell

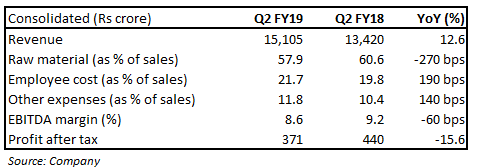

While consolidated revenue grew 12.6 percent year-on-year (YoY), earnings before interest, tax, depreciation and amortisation (EBITDA) margin was marred by poor operating performance of SMP and India business.

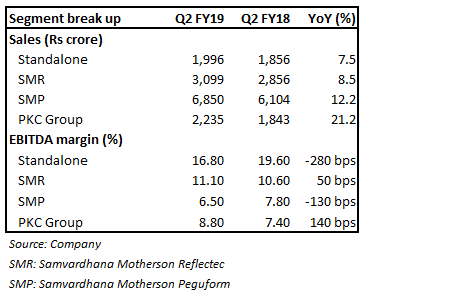

Segment-wise, the standalone business saw a revenue growth of 7.5 percent (YoY), led by a 6 percent and 23.2 percent growth in domestic and international business, respectively. EBITDA margin, however, contracted 280 basis points (100 bps = 1 percentage point) due to a weaker rupee and significant rise in raw material prices, which was partially offset by cost control measures undertaken by the management.

SMP, which produces modules and polymer components and is a leading global supplier of door and instrument panels and bumpers, posted flat revenue growth in euro terms due to subdued demand from Germany. EBITDA margin declined 130 bps led by start-up cost, negative operating leverage and weak margin from Reydel Automotive Group. Revenue for Samvardhana Motherson Reflectec (SMR, a leading global supplier of exterior mirrors) remained flat, while the same for PKC, a Finland-based wiring harness specialist company, grew 12.3 percent in euro terms. Its EBITDA margin expanded 140 bps.

Factors working in favour of the company:

Strong order book MSSL has a robust order book, which offers strong earnings visibility going forward. Its order book at the Samvardhana Motherson Automotive Systems Group BV (SMRPBV) level stands at Rs 164,315 crore (19.53 billion euro).

Expansion on track The company has many plants at various stages of completion. The management said SMP’s Kecskemet and Hungary plants are operational and that its US plant (Tuscaloosa) is likely to turn operational by Q3 FY19. These three new plants are expected to add $1 billion to revenue on a full ramp-up in H2 FY20.

Once the new plants begin operations and ramp-up fully, operating leverage will kick-in and start up costs would wane, thereby contributing to margin expansion.

Strong volume growth The management attributed growth in India topline to demand accruing from new model launches and refreshers. The growth was also led by an increase in content per vehicle. Its outlook for the Indian automobile industry continues to remain positive, with demand picking up as soon as macro-economic challenges wane.

PKC – a growth driver Integration of PKC with MSSL has been happening smoothly and is evident from the strong growth during Q2. The latter was driven by healthy growth from the North American and European truck market. PKC has received a 280 million euro order from Bombardier and is in discussion with various original equipment manufacturers (OEMs) to develop and supply electric systems.

EVs an important growth driver Given the global focus on EVs, we feel it would be an important growth driver for the company going forward. As per the management, battery driven vehicles would need more wiring components, which would increase the content per vehicle by close to 10-20 percent, benefiting MSSL. Other businesses related to polymer and mirror-based products are immune to the shift to EVs.

Valuations In light of the subdued demand and outlook, the stock has corrected quite significantly and is down 44 percent from its 52-week high, which is a very reasonable valuation for a strong franchise like MSSL. The counter currently trades at 25.1 times FY19 and 19.7 times FY20 projected earnings.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!