Tata Motors reported a disappointing set of Q3 FY19 earnings, led by pain in its Jaguar-Land Rover (JLR) business. In fact, deterioration in domestic market conditions led to subdued numbers from its standalone business as well.

JLR is expected to continue to face challenges in various economies, including uncertainty in UK, Europe and China. This, coupled with huge investment requirement to revamp the ageing portfolio and inclusion of electric vehicle (EV) in its portfolio, would continue to weigh on the business. Domestic business outlook is sluggish on the back of multiple macroeconomic challenges, leading to muted consumer sentiments. We advise investors to wait until the dust settles.

Quarter snapshot

JLR - challenges galore JLR’s (excluding Chery joint venture) wholesale volumes declined 2.8 percent year-on-year (YoY) and Chery JV (in China) volumes saw a significant decline (54.5 percent). Total volume declined 11 percent YoY. The sales decline is primarily on the back of deteriorating market conditions in China that led the company to stop production to maintain inventory. Decline in UK and Europe was on account of concerns over more restrictions on diesel vehicles. JLR’s European and UK portfolio are predominantly diesel.

Earnings before interest, tax, depreciation and amortisation (EBITDA) margin witnessed a YoY contraction of 350 basis points (100 bps=1 percentage points) due to de-stocking, warranty costs and higher marketing expenses.

JLR reported a loss for third consecutive quarter at 258 million pounds as compared to profit of 88 million pounds in the same quarter last year. The company also impaired its asset (to the tune of £3.1 billion) in use to factor in significant market, technological and regulatory challenges.

Also read | Tata Motors revises margin guidance downwards to 3-6% from 4-7%

Domestic business – subdued numbers Amid multiple macroeconomic challenges, the standalone business posted a weak set of numbers. Volumes declined 0.5 percent due to muted consumer sentiment. EBITDA margin remained stable at 9.1 percent. Commercial vehicle (CV) margin saw a 50 bps dip to 11.6 percent on negative operating leverage. Passenger vehicle (PV) segment, on the other hand, continued its recovery in operating profitability, which stood at 0.9 percent.

Notably, the company continues its market share gain in CVs as well as PVs and gained 60 bps and 50 bps, respectively.

OutlookWeak JLR Outlook for JLR continues to remain weak on the back of multiple challenges, which it faced in various geographies. The management expects FY19 retail sales to be negative though it sees strong growth coming in from premium segments between FY20 and FY22. It also expects inventory de-stocking to continue in Q4 FY19.

In order to arrest the fall in operating margin, the management has taken various steps to cut costs and expects annual saving of 1.3 billion pounds through operating leverage, employee costs (reduced workforce), its modular platform and low cost Slovakia plant.

Despite these, the management expects negative earnings before interest and tax (EBIT) margin for FY19 and has slashed its EBIT guidance by 3-6 percent for the next three fiscals from 4-7 percent earlier. It would be difficult for the company to go back to its previous margin levels, which were north of 10 percent.

Investments over a billion pounds, coupled with working capital outflow towards re-launches, resulted in negative free cash flow of 661 million pounds in Q3 FY19. Major technology changeovers and portfolio rejig need higher investment for the long-term. This will add to existing pressure from tough market conditions and continue to hurt operating margin. The management maintained its investment guidance to 4 billion pounds for FY19 and FY20.

Domestic outlook – sluggish in the near term The domestic market has been facing challenges on the back of weakening macroeconomic environment, leading to muted sentiments for the automobile sector, including CV and PV segments. Subdued market sentiments are on account of liquidity problems, financing issues, rising interest rates and slowdown in economic activity. This was further aggravated by the lag impact of new axle load norms in the CV segment.

We expect demand to remain weak in the short term but long-term growth outlook remains promising on the back of economic growth, rising income levels, lower penetration, government’s thrust on increasing rural income and focus towards infrastructure and construction.

Upcoming Bharat Stage VI emission norms is the near-term driver for the company. This is expected to lead to advancement in buying as new BS-VI compliant vehicles would be expensive than current vehicles. The government’s scrappage policy would potentially lead to replacement of 200,000-300,000 trucks, which are over 20 years old.

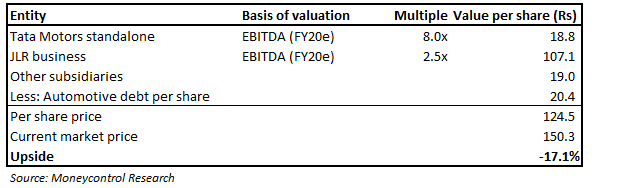

Valuation The stock is down 61 percent from its 52-week high hit in February last year due to weak outlook and weakness in the business. We would recommend avoiding the stock for the time being, amid multiple challenges that are yet to abate.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!