Mahindra & Mahindra Financial Services (M&M Finance) reported a weak headline number in Q3 FY19, although some of its core parameters have been gaining strength. The headline number was muted on account of the Rs 65 crore exceptional income in the year-ago quarter as well as a surge in operating expenses.

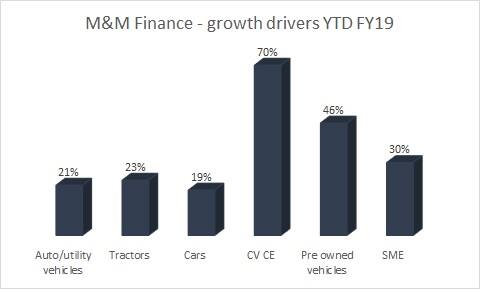

Key positivesBusiness momentum remains strong, with assets under management growing by over 30 percent at the end of December 2018, driven principally by commercial vehicles (CVs), pre-owned vehicles as well as lending to small & medium enterprises (SMEs). Growth in disbursement was in excess of 24 percent.

Source: Company

The quarter under review saw the lingering impact of the Infrastructure Leasing & Financial Services (IL&FS) crisis and tightness in liquidity. However, the management said there was no funding constraint for M&M Finance, although the company carried some excess liquidity as a precaution. The end-market still looks good, with no pressure on lending yields. Despite the challenges, the company was able to maintain its interest margin.

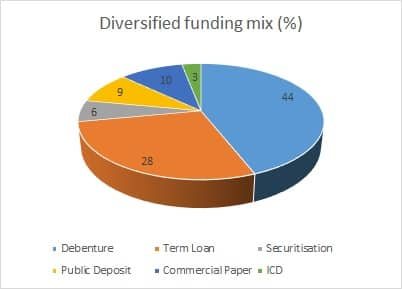

The lending book remains diversified and so is the source of funding, thereby de-risking the business.

Source: Company

Source: Company

Asset quality improvement continues with Q3 witnessing a 10 percent sequential decline in gross non-performing assets (NPAs). Gross and net NPAs at the end of the quarter stood at 7.7 percent and 5.8 percent, respectively.

Some of the important subsidiaries of the company are showing improvement. Mahindra Rural Housing (88.75 percent stake) reported 32 percent growth in after-tax-profit for the first nine months of FY19, with a gradual improvement in asset quality. Mahindra Insurance Brokers (80 percent stake) reported a 46 percent growth in profit after tax for 9M FY19.

Key negativesAfter a blistering pace of growth in the past, volumes for the automobile industry appear to be on a slow lane and that could impact demand from its end-customers.

There was a significant increase in operating expenses in Q3, leading to a surge in the cost-to-income ratio to 39.4 percent from 35.1 percent in the preceding quarter. The management indicated an ex-gratia payment to employees on account of the company’s silver jubilee and some increase in advertising spend.

While underlying asset quality has improved, provision cover (provision held against non-performing assets) has actually declined to 26.9 percent from 34.9 percent in the previous quarter. The management, however, maintained that the overall loss given default (LGD) is close to its current level of coverage.

Other observationsThe management isn’t too worried about its growth outlook and feels 20 percent asset growth is achievable as most of the products financed are not aspirational but are driven by necessities.

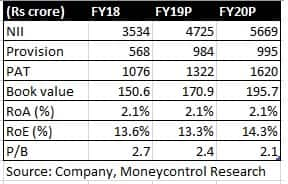

On the back of improvement in net interest margin (NIM), productivity and decline in provisions, the management is hopeful of reaching three percent return on assets (RoA) in the next couple of years from the present 2.2 percent.

OutlookM&M Finance, with its deep rural penetration, has carved a niche for itself. Diversification in asset as well as funding book makes the business relatively de-risked and the marquee parentage insulates it from the funding issues that has engulfed the non-banking financial company (NBFC) space. We see M&M Finance as a vantage player to wean away market share from weaker competition.

The decline in credit cost could be a trigger for earnings going forward. While we do not rule out temporary weakness in the stock due to the overall slowdown in the automobile end-market, the weakness may be a perfect time to accumulate the stock for the long term.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!