Infosys reported an interesting set of Q3 FY19 earnings that had its fair share of positives and negative surprises as well.

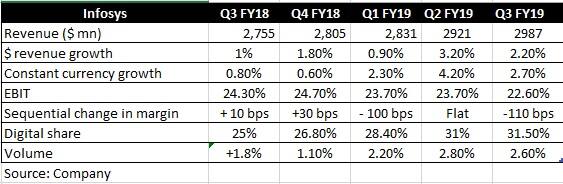

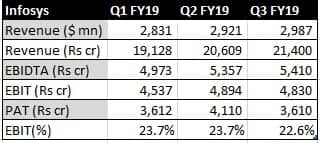

Key positives- Revenue momentum was strong - up 2.2% sequentially to $2,987 million. Sequential growth in constant currency was 2.7% and YoY growth of 10.1%.

- Digital continued to grow much higher than the company average at 33% YoY and 5% sequentially and constitutes 31.5% of revenue

- Infosys has revised its FY19 revenue growth guidance to 8.5-9% from 6-8%

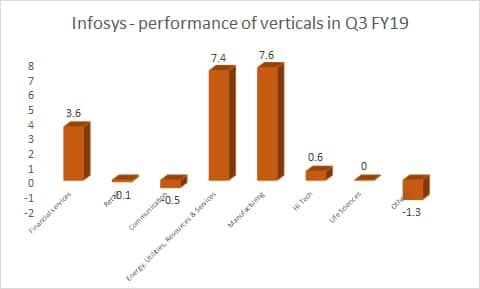

- Geographically, the key markets of Europe and North America performed well. In terms of services, energy utilities, manufacturing as well as financial services stood out

Source: Company

- Demand environment remained extremely strong with the company announcing 14 large deals worth $1.57 billion. Deal wins in the first nine months of FY19 stood at $4.7 billion as against $2.2 billion in the year ago period

- Attrition rate declined by close to 210 bps sequentially

- Strong payout (additional dividend of Rs 4 per share and buyback of shares worth Rs 8,260 crore)

Source: Company

Key negatives- FY19 margin guidance maintained at 22-24%

- Steep decline in margin (110 bps sequentially) to 22.6% in the quarter under review. Reversal of the decision to sell assets like Panaya and Skava led to additional depreciation, impacting margin by 40 bps

- Company continues to invest to enhance digital capabilities and bolster sales force, hence margin may remain weak in Q4 as well

- Decline in utilisation rate (number of people on billable projects compared to overall employee strength) to 83.8% versus 85.6% in the previous quarter

Key observations- Widespread macro concerns have had no impact on the demand environment so far

- Infosys expects client budgets for FY20 to remain flattish with a focus on newer areas

- The management sticks to accelerated investment plan to enhance capabilities in FY19. Hence, investments are unlikely to go up incrementally in FY20

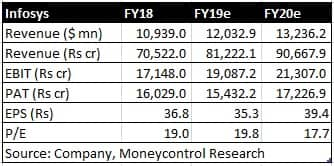

Source: Company, Moneycontrol Research

OutlookWe see Infosys gradually enhancing its core capabilities and competitive positioning to capitalise on strong demand. Hence, adverse macro developments need to be monitored closely. While the Infosys has not yet alluded overtly to supply-side concerns, investors got to be mindful of this challenge as well.

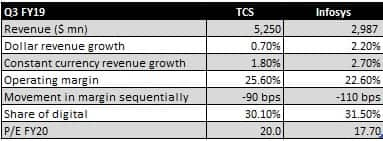

While margin may remain weak in the near term, the revenue traction cannot be ignored. With Infosys back on the growth trajectory it is likely to close the valuation gap with bigger rival Tata Consultancy Services (TCS).

With the hefty payout ratio (close to 4.4% pre-tax) limiting downside, we recommend buying Infosys.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!