Dyes and dye intermediates major Bodal Chemicals saw a recovery in topline growth in Q1 FY19 aided by better realisations and increased contribution from the commissioning of new capacity. Similarly, food colour major Vidhi Specialty Food Ingredients witnessed higher production due to debottlenecking at its Roha plant. While both companies are key beneficiaries of environmental compliance and favourable supply-demand dynamics in their respective segments of dyes and colour industry, their focus on vertical integration and capacity expansion provides impetus to earnings growth.

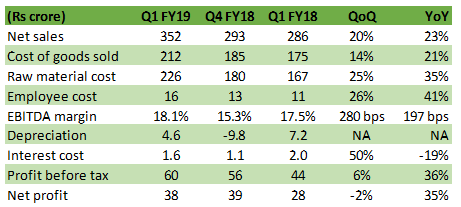

Bodal Chemicals: Margin expansion in Q1

Source: Company

Bodal Chemicals reported a 23 percent year-on-year (YoY) increase in Q1 sales on a consolidated basis, driven by improved volumes and sales realisation of key dye intermediates. Production volume of dye intermediates (48 percent of sales) increased 21 percent in the quarter under review. Exports, which constitute 43 percent of sales, grew 86 percent YoY and has been another strong lever for the company.

Raw material prices remained elevated though the management said prices of late have stabilised, particularly that of caustic soda. Standalone operating profit, adjusting for forex, improved 100 basis points YoY.

Core and allied businesses continue to improveIts core business is on track. New dyestuff capacity has started contributing to topline, with around 10 percent capacity utilisation and is expected to reach optimum level by next fiscal. New capacity is expected to aid net revenue (adjusting for captive consumption of intermediates) of about Rs 140 crore next fiscal.

The management expects improved performance for Trion Chemicals, a joint venture for the water treatment chemical business. It plans to start operations by September-end as some raw material prices have softened and expects it to break-even next quarter. Subsidiary SPS Processors has started contributing to profitability. New vinyl sulphone capacity is still to turn operational, pending regulatory permission for the usage of ethylene oxide.

Core business prospects encouragingOur positive stance on the company is driven by its core business (dyes value chain) prospects. We remain positive on the traction towards vertical integration and capacity expansion. Ongoing environmental restrictions in both China and India is helping maintain the favourable supply-demand dynamics for integrated players like Bodal Chemicals (8.6 times FY20e).

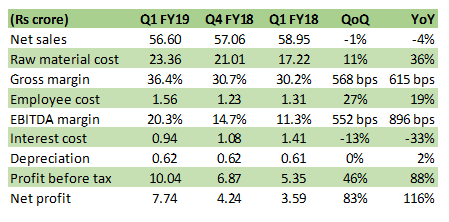

Vidhi Specialty’s Q1 sales witnessed a slight YoY decline on account of declining share of its trading business. In FY17, trading accounted for 45 percent of sales, which is about 26 percent as per our estimates. Higher absolute sales from manufacturing was driven by the debottlenecking exercise due to which production efficiency has improved to about 300 tonne per month from 225 tonne earlier.

Due to change in sales mix and sales of new high margin products, gross margin jumped to 36.4 percent (up 615 bps) offsetting higher cost of materials sold (36 percent YoY). Lower other expenses helped improve earnings before interest, tax, depreciation and amortisation (EBITDA) margin to 20.3 percent in Q1.

Finance cost has declined sequentially, aiding growth in profit before tax growth of 88 percent YoY and 46 percent quarter-on-quarter.

Increased share of manufactured sales

Source: Company

Capacity expansion and product mix to aid earnings growthJoint Managing Director Mihir Manek reiterated its sales turnover guidance of Rs 500 crore in 2020. While its capacity expansion plan remains on track, improving product mix, lower trading business and backward integration are expected to improve earnings. As a result, operating margin is expected to inch above 20 percent.

In FY19, the management is eyeing around Rs 250 crore in turnover, with about 25 percent contribution from the trading business. It expects to retire its debt this year before new working capital-related needs arise for the expanded facility.

We expect 48 percent compounded annual growth rate in EBITDA for the next three-years based on topline growth and margin expansion. In light of improved emphasis of high margin and low trading product mix, we expect 660 bps margin expansion by FY21 on an FY18 base. The stock is currently trading at a price-to-earnings multiple of 9 times FY20e earnings, which seems attractive given the regulatory nature of the business.

Follow @anubhavsaysFor more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!