Atul Ltd (Market cap: Rs 9,906 crore), a leading integrated chemical manufacturer, deserves attention as it benefits from improved end markets, supply side reforms in China and growing reliance on India as a favoured destination for sourcing chemicals. While company's foray into new products and available capacity bandwidth will keep it ready for meeting demand, efforts on backward integration and lower finance cost are expected to further aid bottom-line growth.

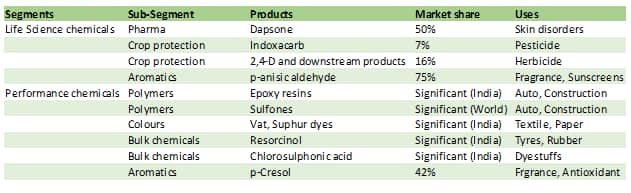

Key highlights for the company-Strong presence in the performance chemicalsIn the performance chemicals segment (~2/3rd FY18 revenue), company manufacturers chemical intermediates for the varied end markets. It is a market leader for aromatic compounds having applications in personal care and fragrance end markets.

Further, company is among the largest manufacturer of vat and sulphur black dyes in the colour sub-segment, having applications for textile and paper industries. Atul also has a JV with the German company Rudolf, through which it offers full range of textile dyes.

Additionally, the company is a pioneer in the production of epoxy resins and its brands Polygrip and Lapox are known in end markets like furniture, auto and construction.

Table: Significant market share in varied chemicals

Large part of the life science chemicals segment (~1/3rd of FY18 revenue) caters to crop protection end market wherein key products 2,4-Dichlorophenol (2,4-D) and Indoxacarb command significant market share globally.

In case of another life science chemicals sub segment - pharmaceuticals, Atul is involved in he production of various basic chemicals (Amino acids, phosgene derivatives) and APIs. The major API where company is a market leader is di-amino di-phenyl sulfone (Dapsone) which is used to treat skin disorders like Hansen's disease.

Backward integration to aid marginsAtul has a JV with Akzo Nobel (50:50) in order to produce monochloro acetic acid (MCA), which in turn is used for the production of 2,4 D. Capacity under this JV is expected to reach 32,000 tonnes by Q4 FY19.

The company repaid its debt last fiscal year which provides scope to fund capacity expansion program in future. Further, Atul's return ratios and free cash flow are expected to improve on the back of economies of scale, improved pricing, better end markets and lower finance costs.

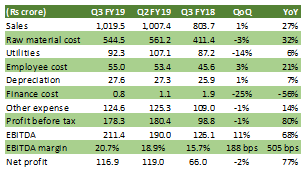

Q3 – benefits from better pricing trendsIn recent times, better operating performance was witnessed for both the segments. Standalone Q2 sales grew by 27 percent YoY aided by strong growth in life science (27 percent YoY) and performance chemicals (28 percent YoY). EBITDA improved by 68 percent YoY (Margin: 20.7 percent) on account of better pricing effect and operating leverage.

Table: Q3 FY19 financials

It's noteworthy that company benefits from the imposition of anti-dumping duty on Sulphur black imported from China. However, this anti-dumping duty is applicable till July’19. In the event of anti-dumping duty termination, there would be a marginal impact on margins as the supply demand dynamics have restored in due course of time.

OutlookWe continue to expect low double digit sales growth for next three years powered by growth outlook in diverse end markets (mainly automobile, crop protection, dyes, and fragrances) and improved pricing effect for some of the products.

Atul has incurred more than Rs 840 crore capex in last four years. Currently, additional revenue potential based on capacity bandwidth is 0.9 times FY18 sales.

Further, taking note of strong operating performance, we expect the company to sustain around 17 percent in the medium term. On account of favorable supply demand scenario in some of the segments, we remain buoyant.

Key risk to watch out is oil prices though we expect it to remain rangebound. As far as the stock is concerned, it has consolidated recently and is now trading at a reasonable level of about 22.4x FY20e earnings.

Follow @anubhavsaysFor more research articles, visit our Moneycontrol Research page(Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!