Neha Dave

Moneycontrol Research

Highlights:

- AUM growth ahead of industry; favourable asset mix

- Operating expenses decline

- Impact of total expense ratio manageable

- Rich valuations to limit near-term upside in the stock price

- HDFC AMC remains the key beneficiary of enduring growth in the MF industry

-------------------------------------------------

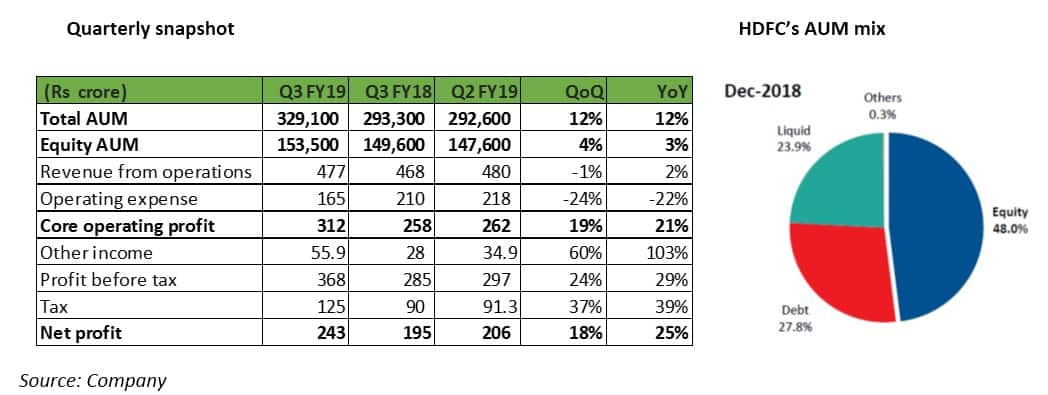

HDFC Asset Management (HDFC AMC) reported strong Q3 FY19 earnings, with net profit rising 25 percent year-on year, on the back of an increase in assets under management (AUM) and favourable asset class mix. It also regained its position as the largest asset management company (AMC) in India, with total AUM market share of 14.4 percent as on December 31, 2018.

Liquid AUM surged

HDFC AMC’s AUM increased to Rs 3,29,100 crore as of December-end, a growth of 12 percent YoY, better than industry growth of 8 percent during the same period.

Growth in AUM was mainly driven by liquid assets, which increased to Rs 78,655 crore during Q3, a sequential growth of 72 percent. Against this, industry growth in liquid funds was a mere 15 percent quarter-on-quarter. The AMC earns negligible fees on liquid funds. So, how should investors read this growth? As positive.

The MF industry faced large redemptions (withdrawals) in liquid schemes in September last year, triggered by the default of IL&FS group companies. HDFC AMC, however, saw a surge in liquid flows in the aftermath of the liquidity crisis. Market share gains during this tumultuous period is a testimony of HDFC AMC’s strong brand.

Asset mix still favourable and better-than-industry

Equity AUM growth of 4 percent was in line with the industry during the quarter under review. Share of high revenue earning equity assets declined 48 percent in Q3 from 52 percent of the AMC’s total assets QoQ. This decline in equity asset mix shouldn’t bother investors much as it was mainly due to disproportionate growth in liquid assets. In terms of asset mix, HDFC AMC still stands out far better than the industry, which has 44.8 percent of its total AUM in equity assets as at December-end.

Granularity of the asset book adds to the comfort

HDFC AMC continues to enjoy the highest share of individual customers. The AMC reported unique individual accounts of 8.86 million as at December-end, a growth of 17 percent YoY. As a result, 62 percent of the AMC’s total monthly average AUM is contributed by individuals compared to 54 percent for the industry. This is very encouraging as flows from individual customers are relatively sticky. Also, individual investors favour equity schemes, which generate higher investment management fees compared to debt schemes.

Current monthly flows through systematic investment plans (SIP) stood at Rs 1,169 crore. Around 64 percent of the SIP book has tenure of more than 10 years, adding to predictability and visibility in AUM growth.

Operating expenses declined

The AMC reported a 22 percent decline in operating expenses during Q3 due to decline in scheme-related expenses, which will be borne by MF schemes and not by the AMC as per market regulator SEBI's directive.

In its circular dated October 22, 2018, the Securities and Exchange Board of India (SEBI) banned payment of upfront commission and mandated a full trail model for distributor commission. It has further mandated that all scheme-related expenses, including distributor commission, will have to be paid by MF schemes and not by the AMC.

HDFC AMC took a Rs 9 crore hit during Q3 (Rs 21 crore in Q2) on its Rs 40 crore exposure towards IL&FS’ (holding company) preference shares. Adjusting for this one-off impairment expense, core operating profit increased 25 percent YoY, better than the reported growth of 21 percent.

Outlook - impact of TER reduction manageable

SEBI had earlier announced a major overhaul of the fee structure that AMCs charges to investors. Read: SEBI cap on MF fee income will have a widespread impact, and not just on AMCs

The proposed reduction in total expense ratio (TER) by SEBI will come into effect from April 1. While it will lead to an weighted average impact of 24 bps on HDFC’s equity-oriented AUM, the management reiterated that it will pass on 21-22 bps by cutting distributor commissions. This should limit the adverse impact of SEBI’s move on the AMC’s financials, which spooked investors, leading to a free-fall in the stock.

For new inflows, AMC will have to absorb some impact, but it will be more gradual from a Profit & Loss perspective. The extent of cost sharing with the distributor (whether it is 50:50 or 60:40) will be determined in due course, based on how the competition pans out.

Rich valuations but a long-term compounderHDFC AMC’s stock has corrected almost 25 percent from its 52-week high. Despite the sharp fall in its stock price, valuations are still rich as the AMC is trading at 9 percent of its trailing AUM (December 2018) and 33 times FY20 estimated earnings. On a relative basis also, HDFC AMC is being valued at a premium of more than 50 percent to its closest listed peer. This doesn’t come as a surprise.

Akin to most of HDFC group companies, the AMC also commands a relative premium valuation, purely stemming from its brand and consistency in performance. Given HDFC AMC’s best-in-class return ratios, with return on equity (RoE) above 40 percent and future growth levers, we believe rich valuation can sustain. However, premium valuations limits near term upside.

While SEBI’s mandate will induce some pain in the medium term, the lower charges (TER) will make mutual funds more attractive to investors and aid penetration in the long run, benefiting industry leader like HDFC AMC. Hence, long term investors should look to buy the stock in a staggered manner as SEBI’s move doesn’t alter the structural growth story of HDFC AMC.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.