Corporate, or wholesale, banking is a relationship game, a risky one at that. India’s banks were found on the wrong side of this relationship a few years ago and that has left lenders bruised enough to tread carefully. This in part explains their reluctance to go all out in seeking big corporate borrowers at a time when policymakers are pushing for companies to raise capital and invest.

Lender's cautionThis caution is reflected in lending to mid-sized and smaller companies as well. Bankers say their reluctance stems from the potential mispricing of corporate loans and not from a lack of demand from the industry. In a way, the modest 5.7-percent growth in loans to industry in FY23 reflects the caution from lenders rather than the lack of borrowers. The 20.6 percent retail loan growth shows where banks are more than willing to deploy their funds.

Wholesale loan mispricing was first flagged by Kotak Mahindra Bank Ltd a few weeks ago. In the press interaction following the release of fourth-quarter earnings performance, the private sector lender’s head of wholesale lending KVS Manian said, “There is a significant amount of irrational pricing in the market. We have seen BBB (rated) entities getting (funds) at the same rate as AA (rated) entities are.”

Manian added that Kotak Mahindra Bank is not seeing demand for loans from companies that meet its underwriting parameters. The private sector lender’s corporate loan book was muted in Q4FY23 although the bank has turned quite liberal of late from a conservative lender. Despite its more accommodating approach to lending, the bank has steered clear of growing its wholesale loan book as fast as others.

Large private sector lenders such as ICICI Bank and HDFC Bank have reported higher growth in their corporate loan books. That said, such growth has accompanied commentary indicating utmost caution while lending wholesale. Executives from both the large private sector lenders have indicated in the past to investors that they remain watchful on cash flows and prospects while lending to large companies and even to smaller ones.

Public sector banks seem to be more comfortable giving out wholesale loans. That said, they too believe that loan rates do not fully reflect the risks involved. “We are renegotiating with the corporates for better returns. When interest rates were low because of policy rate cuts during the pandemic, instead of keeping liquidity, it was better to lend to corporates. But now the interest rate regime is on the higher side and so lending has to generate equal returns. We don’t want to grow at the cost of the bottom line,” said K Satyanarayana Raju, managing director and chief executive officer of Canara Bank.

Raju explained that though he hasn’t come across mispricing instances, the bank is seeking a higher yield from its corporate loan book. In other words, the interest rates on such loans have the scope to further rise in order to fully cover the risks involved.

This brings us to the question as to why corporate loans are potentially mispriced now when liquidity is more expensive than before due to consecutive policy rate hikes.

The swiftness with which policy rates were cut in response to the pandemic and then hiked back after two years has made loan pricing difficult for banks. Assessing credit risk has also become challenging since a bunch of borrowers were able to perform reasonably well simply because of forbearance in the wake of the pandemic. Their real financial prowess was masked by loan covenant relaxations.

Beyond the pandemic-affected years, corporate balance sheets have healed but the outlook on demand and the overall economy isn’t convincing big companies to borrow for capex. Analysts at Kotak Institutional Equities believe that earnings growth would moderate in FY24 and FY25, even though overall economic growth could be reasonably enthusiastic at 6.5 percent.

Some of the firms that need credit and are knocking on banks’ doors are doing so to keep up with the increase in their working capital needs due to raw material inflation. Small businesses have been hit hard by elevated commodity inflation in FY23 as also an increase in transport costs due to higher fuel prices.

Top-rated large companies have resorted to raising funds from the bond market where yields have eased substantially, which in turn is making it difficult for banks to increase their loan rates. This has affected transmission and even as policy rates have increased 250 basis points within the past one year, the weighted average lending rate (WALR) on outstanding loans of banks has climbed just 100 basis points. One basis point is one-hundredth of a percentage point. The increase in WALR of fresh loans is higher, an indication that repricing of old loans is taking time. “We have to balance between pricing and losing the best quality credit. If you want the best-rated corporate to borrow from you, you will have to keep loan rates competitive, even versus the bond market which is why pass through on MCLR has been low,” said an executive at a public sector bank requesting anonymity.

Going slow on transmission

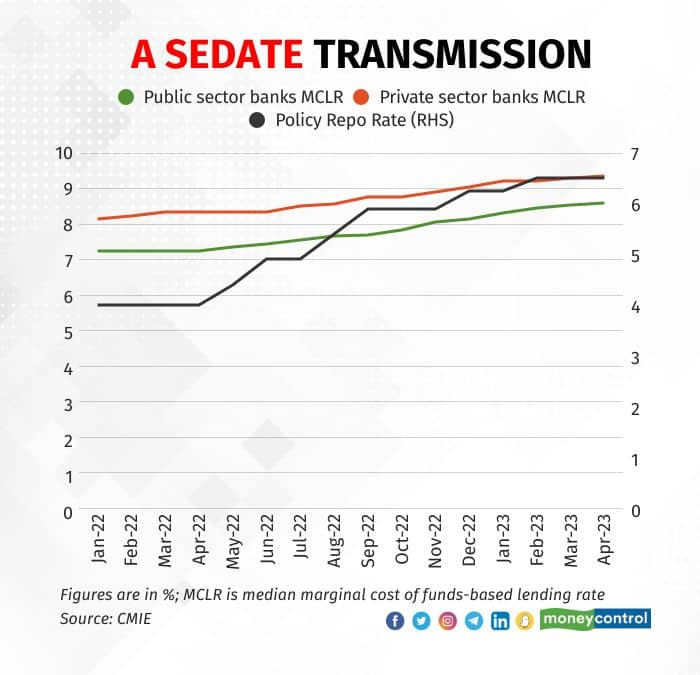

Going slow on transmissionCorporate loans are priced off marginal cost of funds-based rate (MCLR), which is a function of the bank’s deposit rates. The RBI has mandated retail and MSME loans to be priced using an external benchmark-based lending rate (EBLR), which is the repo rate. The transmission of rate hikes through EBLR has been swift while that through MCLR is wanting, especially for public sector banks.

As the above chart shows, the median one-year MCLR has risen by 125 basis points for public sector banks and 100 basis points for private sector lenders during the period that saw policy rates being hiked by 250 basis points.

Canara Bank’s renegotiations with large borrowers on loan rates speak of these challenges too. Historically, private sector banks have been able to squeeze enough from borrowers to justify the risk they underwrite, while public sector peers have chased volume and size at the cost of quality. The exuberance from public sector banks towards corporate lending in the previous cycle is missing this time. That said, lenders are chasing companies of good credit even as they sacrifice in some pockets to remain competitive. Bad loans are an unavoidable outcome of lending, but the idea is to avoid a punishing cycle like last time.

Leave it to an industrialist to sum up this corporate-banking relationship game. In the words of American oil magnate Paul Getty, “if you owe the bank $100 that is your problem. But if you owe it $100 million, that is the bank’s problem.” India’s banks are hoping to avoid this problem.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.