Dear Reader,

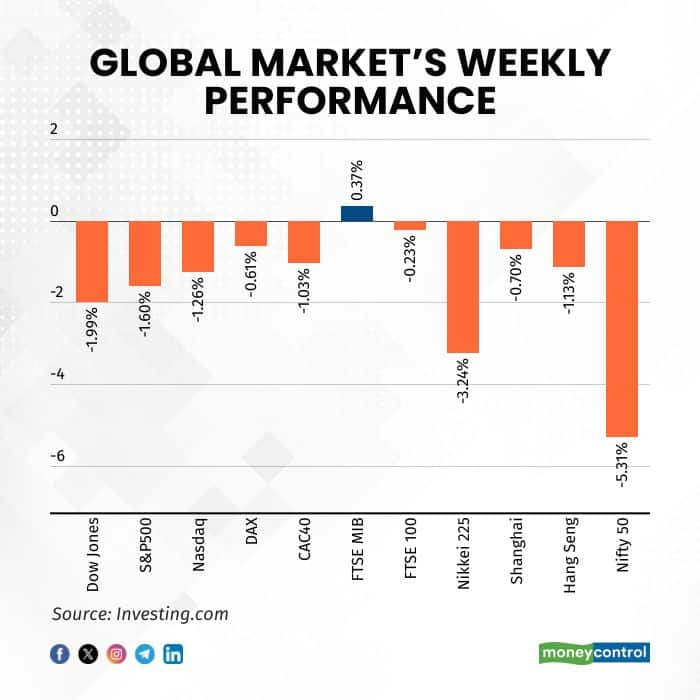

For the third consecutive week, crude oil prices held above the $100-per-barrel mark, casting a long shadow over global equity markets, with Asian markets bearing the brunt of the selloff. India proved the most vulnerable among its regional peers, as concerns over energy supply disruptions stemming from the Strait of Hormuz bottleneck weighed heavily on investor sentiment. The ripple effects were swift and broad — the Nifty50 fell 5.31 percent over the week, while the Midcap and Smallcap indices shed 4.5 percent and 3.6 percent respectively.

Every sectoral index closed in the red, with the auto sector leading the decline at a steep 10.6 percent. PSU Banks fell 7.2 percent, while Defence and Private Banks each dropped 7 percent, and Metals shed 6 percent — a sweeping retreat that underscored just how broadly the anxiety had spread across the market.

Foreign institutional investors showed no signs of returning. For the fourth week running, FIIs remained net sellers, offloading equities worth Rs 35,052 crore during the week alone, bringing the month's total outflow to Rs 56,883 crore — a figure that speaks to a sustained and deliberate withdrawal of foreign capital.

The mood was no better in Western markets. US indices declined for the third straight week, buffeted by the ongoing Middle East conflict and the volatility it has injected into oil markets. Adding to the unease were growing concerns about stress in private credit markets and uncertainty around trade policy. Compounding these worries, the second estimate of US GDP growth for the fourth quarter was revised sharply downward — from an initial reading of 1.4 percent to just 0.7 percent annually — as weaker exports, consumer spending, government outlays, and investment all dragged on the final figure.

Looking ahead, the trajectory of the war and its grip on oil and gas prices and supply will remain the dominant force shaping market direction. Despite equities edging into oversold territory, the selling pressure shows little sign of abating in the near term.

Downward pressure continues

On the weekly timeframe, the Nifty 50 closed at 23,151.10, registering a sharp decline of 5.31 percent. The RMI momentum indicator continues to hold below the zero line, a sign that selling pressure remains firmly in control. Price has broken through a major support level and is now carving out a lower-low structure — a classically bearish formation that suggests the market is not merely correcting but systematically weakening.

Adding to this concern, the index has slipped below its 40-period exponential moving average, a threshold many traders watch as a barometer of the medium-term trend's health. Taken together with the prevailing pattern of lower highs and lower lows, the overall market structure has unmistakably shifted to the downside. The Nifty 50 is, by any technical measure, in a confirmed downtrend — and unless the pattern breaks, the path of least resistance for now remains lower.

Source: web.strike.money

FIIs have rarely looked this bearish. Their net index futures position currently stands at a deeply negative 2,60,540. The indicator has broken below its previous major support zone, signalling that FIIs have not merely maintained their short positions but have actively extended them to levels beyond historical norms, pushing into territory rarely seen before. As long as these positions remain in place, the resulting downward pressure is likely to weigh heavily on the market in the near term.

Source: web.strike.money

The breadth indicator — measured by the percentage of Nifty 50 stocks trading above their 200-day simple moving average — currently sits at 28, having broken below a major prior support zone. The majority of Nifty 50 stocks have now fallen beneath their long-term averages, reflecting a market where bearish conditions are no longer confined to a few pockets but have spread broadly across the index.

Source: web.strike.money

A second breadth indicator reinforces this gloomy picture. The number of Nifty 50 stocks making new one-month highs, smoothed by a 9-day average, has fallen to just 2 — its lowest recorded level. Barely any stocks are registering fresh highs, confirming that upside participation across the index is virtually non-existent. In short, the Nifty 50's internals remain deeply weak.

Source: web.strike.money

The net new one-month highs indicator for the Nifty 50 deepens the bearish case further, currently sitting at -14.44. More stocks are making fresh one-month lows than highs, adding yet another layer of weakness to an already fragile breadth picture. The direction of travel across the broader index is unmistakably downward, with declining stocks far outnumbering those managing any meaningful advance.

Source: web.strike.money

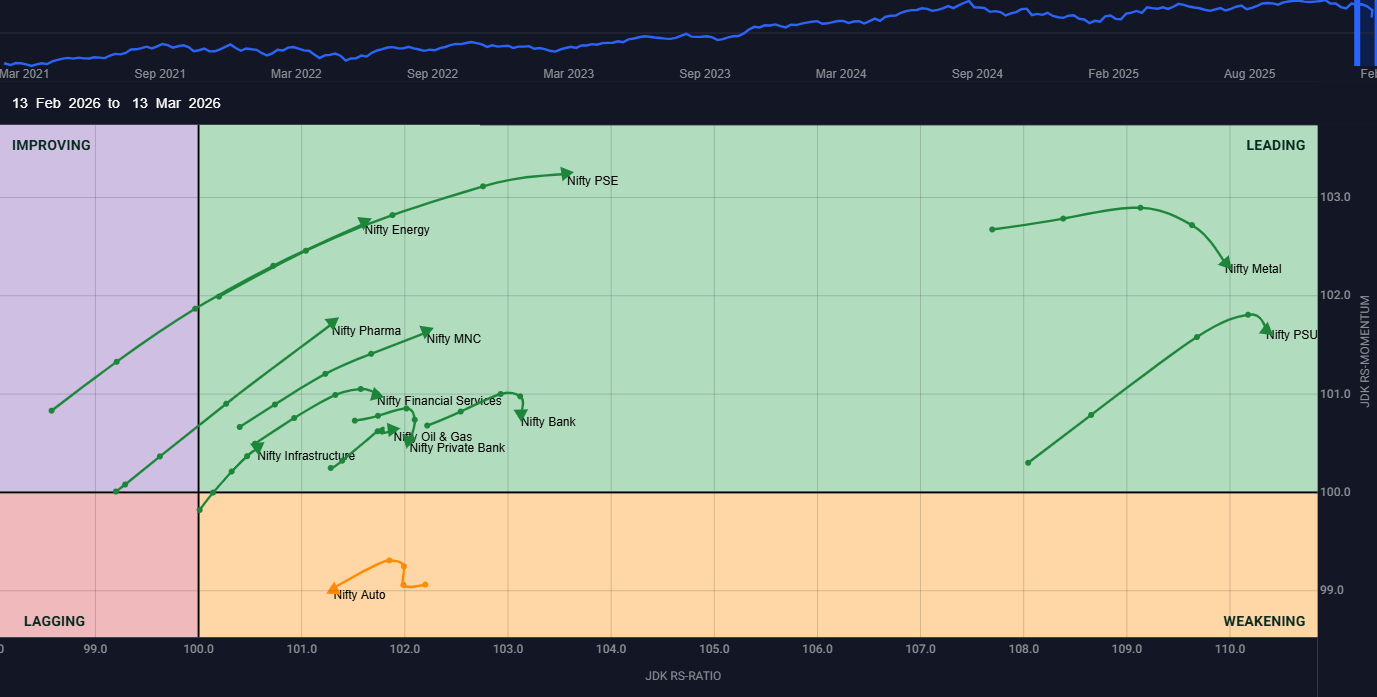

Sector Rotation

Nifty 50 – The Benchmark Index ended lower, by -5.51% this week and closed at 23,151.10.

Leading Quadrant: In the leading quadrant, Nifty PSE, Nifty Energy, Nifty Pharma, Nifty MNC, and Nifty Infrastructure are all showing increased momentum, maintaining their leadership. Meanwhile, Nifty Financial Services, Nifty Bank, Nifty Oil & Gas, Nifty Private Bank, Nifty Metals, and Nifty PSU Bank also remain in the leading quadrant, but these sectors are showing some reduction in momentum. In summary, while several sectors continue to advance, others are beginning to show signs of slowing momentum within their leadership positions.

Weakening Quadrant: In the weakening quadrant, Nifty Auto remains present and is showing a notable reduction in momentum. This sector could be worth watching, as Nifty Auto may shift from weakening to the lagging quadrant if momentum continues to decline.

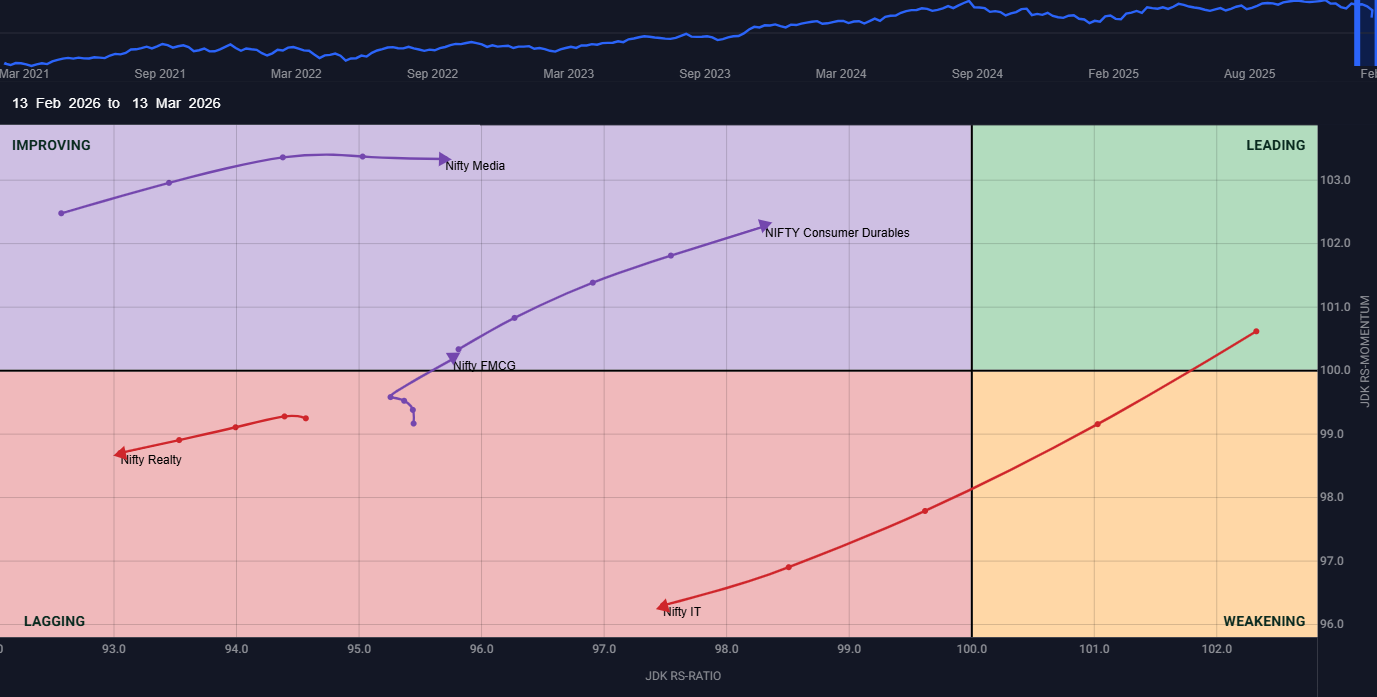

Improving Quadrant: In the lagging quadrant, Nifty IT is showing a significant decline in momentum, making it among the weakest performers across all sectors. Similarly, Nifty Realty is also in the lagging quadrant, with a substantial drop in momentum. These two sectors stand out as among the weakest and may continue to face downside potential in the near term.

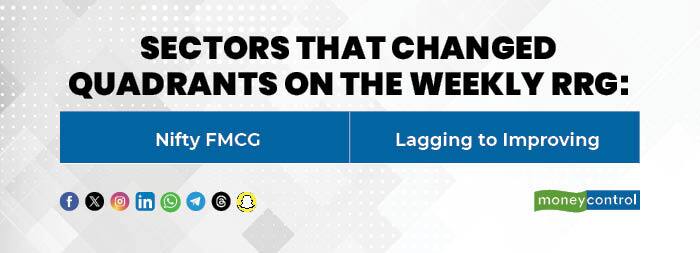

Lagging Quadrant: In the improving quadrant, Nifty FMCG has moved from lagging to improving, showing a stable increase in momentum. Additionally, Nifty Consumer Durables continues to see momentum improvement within the improving quadrant. Meanwhile, Nifty Media also remains in the improving quadrant, but its momentum has slightly declined. Thus, while some sectors are gaining strength, others are stabilising or slowing in momentum.

Stocks to watch

Among the stocks expected to perform better during the week are JB Chemicals, Torrent Pharma, Lupin, GE Shipping, and CCL.

Cheers,

Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.