ICICI Bank is expected to report a modest performance for the July–September quarter (Q2FY26), though analysts believe it will fare better than most of its private-sector peers as margin compression is expected to remain contained within low single digits. The private lender will announce its Q2 results on October 18, 2025.

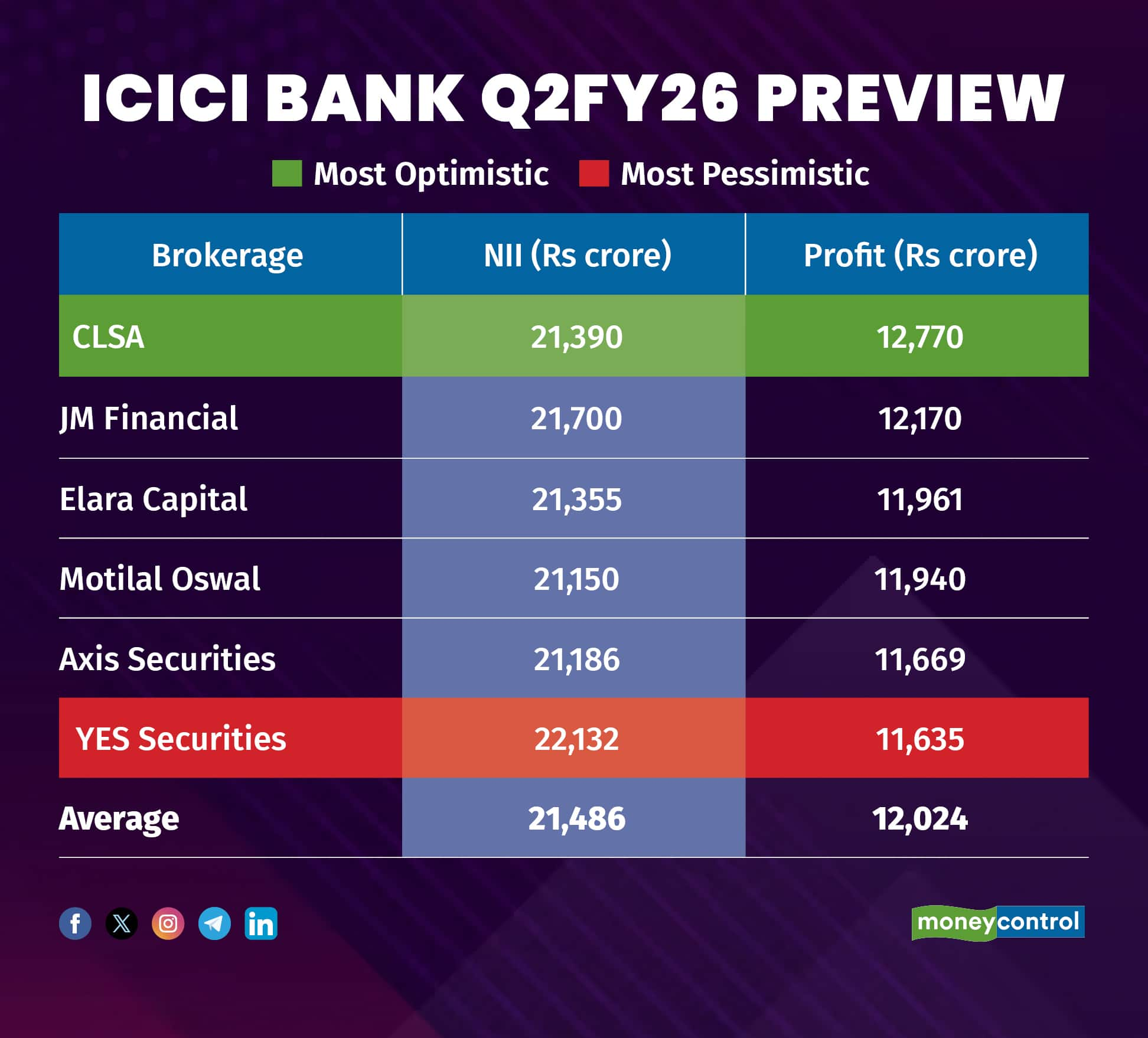

According to Moneycontrol’s poll, ICICI Bank’s net interest income (NII) is projected to rise by 7 percent year-on-year (YoY) to Rs 21,486 crore in Q2FY26, compared to Rs 20,048 crore in the year-ago period. The lender’s profit is expected to grow modestly by 2.3 percent YoY to Rs 12,024 crore in Q2FY26, from Rs 11,746 crore a year earlier.

Estimates of analysts polled by Moneycontrol are shown to be in a narrow range, meaning any positive or negative surprises may elicit a sharp reaction in the stock price. Among the brokerages polled, CLSA rolled out the most bullish projections while YES Securities forecasted the slowest growth for ICICI Bank.

What factors are driving the earnings?

Strong loan and deposit growth: Analysts at Motilal Oswal expect ICICI Bank’s loan book and deposits to grow by around 10 percent YoY each in Q2FY26, reflecting continued business momentum and healthy balance sheet expansion.

Margin compression: According to CLSA, ICICI Bank’s net interest margin (NIM) may see a mild contraction of 10 basis points (bps) YoY to 4 percent in Q2FY26, largely due to the impact of June's repo rate cut.

Stable asset quality: Motilal Oswal analysts expect the bank’s asset quality to remain robust, with gross non-performing assets (NPA) declining to 1.8 percent in Q2FY26 from 2 percent in the same period last year. Net NPA is likely to stay steady at 0.4 percent YoY.

What should investors keep an eye on this quarter?

Investors are likely to focus on loan growth, deposit accretion, and net interest margins, which will provide key cues on the bank’s earnings resilience and growth trajectory in the coming quarters.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.