Bears hit market following imposition of additional US tariffs on Indian goods, dragging the benchmark indices 1.8 percent down to near August lows for the week ended August 29. Severe FII sell-off despite huge DIIs inflow also weighed on sentiment as the pressure was across caps, though there was support from proposed GST rationalisation, favourable monsoon, and possible fed funds rate cut in September.

On Monday, first, the market may react to better-than-expected Q1FY26 GDP numbers, and developments during PM Narendra Modi's four-day visit (August 29-September 1) to Japan and China. Overall, the coming week (starting from September 1) is expected to be rangebound with focus on GST Council meet, auto sales, US jobs data, and manufacturing & services PMI numbers, as well as any updates with respect to India-US trade negotiations for further insights, according to experts.

Last week, the BSE Sensex plunged 1,497 points (1.84 percent) to 79,810, and the Nifty 50 plummeted 443 points (1.78 percent) to 24,427, while the Nifty Midcap and Smallcap 100 indices hit hard, falling 3.3 percent, and 3.9 percent, respectively. All sectors, barring FMCG, saw selling pressure.

"We expect the market to trade in a rangebound manner, tracking developments in the India-US trade negotiations and India’s strategic meetings with global leaders (Japan and China)," Siddhartha Khemka - Head of Research, Wealth Management at Motilal Oswal Financial Services said.

In the interim, according to Vinod Nair, Head of Research at Geojit Investments, the markets are likely to display a mixed bias, with consumption-driven and domestic growth-oriented sectors—such as FMCG, durables, discretionary, cement, and infrastructure—well-positioned to benefit from GST cuts, firm demand, and higher government spending. However, "limited progress in trade talks continues to add uncertainty and weigh on investor confidence," he said.

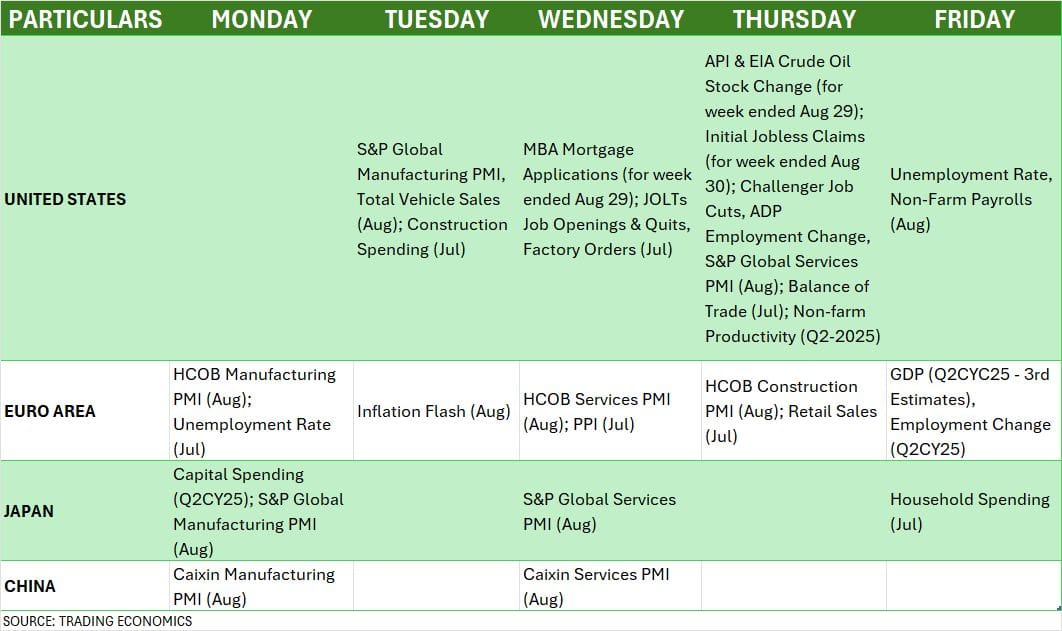

Here are 10 key factors to watch next week:

GST Council Meet

On the domestic front, all eyes will be on the GST Council meeting scheduled for September 3-4 for final decision, especially after the additional 25 percent US tariff on Indian goods effected from August 27 which impacted several sectors like textile, shrimp, footwear, chemicals, and jewellery.

Most experts believe that the GST reform will get finalised as well as implemented in September, i.e. well ahead of Diwali festival, which (along with already announced monetary easing and tax cuts in budget) would provide a timely boost to sentiment and consumption.

As per the expected government proposals, there could be 2-rate GST regime (i.e. 5 percent, and 18 percent) soon, likely covering various sectors including fertiliser, textile, footwear, medicines, surgical items, medical devices, education, paper, and many more, reports CNBC-TV18 quoting sources.

US Jobs Data

Globally, the markets across asset classes will focus majorly on the monthly jobs data including JOLTs jobs openings & quits for July, followed by unemployment rate and non-farm payrolls numbers for August, which could be crucial for the Federal Reserve's next move. Healthy GDP revision and expected PCE figures already signalled a possible rate cut in September policy meeting.

"With Fed Chair Powell recently highlighting downside risks to the labour market, any softness in the August jobs report could solidify the case for policy easing," Kaynat Chainwala of Kotak Securities said.

According to experts, the unemployment rate in August is expected to increase a bit compared to 4.2 percent in July. Apart from this, monthly factory orders, construction spending, and vehicle sales will also be watched.

Global Economic Data

Manufacturing and services PMI final numbers for August will also be released globally including key nations like United States, Eurozone, Japan and China next week. Also, the focus will be on the flash inflation for August, retail sales for July, and third estimates print for June quarter GDP numbers by Euro Zone.

Domestic Economic Data, and Auto Sales

Back home, too, (apart from GST meet details) the final Manufacturing and Services PMI numbers for August will be announced next week on September 1 and September 3. As per preliminary estimates, the HSBC Manufacturing and Services PMI climbed to 59.8 and 65.6 in August against final print of 59.1 and 60.5 in July, respectively.

The foreign exchange reserves for week ended August 29 will be released on September 5. In the previous week ended August 22, the reserves fell to $690.72 billion, from $695.11 billion on week-on-week basis.

Additionally, the focus would also be on the automobile sales numbers for August scheduled to be announced initially next week. Hence, auto stocks including Tata Motors, Mahindra and Mahindra, Ashok Leyland, Bajaj Auto, Hero MotoCorp, TVS Motor, Eicher Motors, and Escorts will be in action.

The market participants will also keep an eye on the FIIs mood as they turned aggressive sellers last week after the change in tariff policies and elevated valuation concerns. FIIs have net sold Rs 21,152 crore worth shares in the passing week, taking the total outflow in August to Rs 46,903 crore, against net selling of Rs 47,667 crore in previous month, as per the provisional data, but they actively maintained their buying in the primary market.

On the contrary, DIIs (Domestic Institutional Investors) provided strong support to the market, in fact, continued buying every dip. They net bought Rs 28,645 crore worth shares during the week, and Rs 94,829 crore for the month of August, the highest monthly net buying since October 2024.

Year-to-date, FIIs offloaded shares worth Rs 2.16 lakh crore, lower than Rs 3.04 lakh crore of selling in the same period last year, however, DIIs net buying was Rs 5.13 lakh crore, against Rs 5.27 lakh crore during the same period.

Rupee at Fresh Low

Meanwhile, the focus will also be on the rupee that depreciated sharply by 0.66 percent to end at all-time closing low of 88.12 against the US dollar after hitting an intraday record low of 88.31 on Friday. The currency formed long bullish candle on the daily charts and traded well above all key moving averages, signalling possibility of bearish trend ahead.

India-US trade war, hedging demand from importers, and FPI outflows from both debt and equity added pressure on the currency, though it acts as a cushion for exporters facing tariff challenges. "The rupee remains undervalued relative to its emerging market peers, but near-term direction will likely stay under pressure due to trade war concerns," Anindya Banerjee, Head Currency and Commodity Research at Kotak Securities said.

Despite weakness in benchmark and broader markets, the primary market will remain in action mode with the eight new public issues hitting Dalal Street next week including only one from the mainboard segment which is Amanta Healthcare's Rs 126-crore IPO scheduled for opening on September 1.

The major action will be seen in the SME segment with the launch of seven public issues - Rachit Prints, Goel Construction, Optivalue Tek Consulting, Austere Systems, Vigor Plast India, Sharvaya Metals, and Vashishtha Luxury Fashion - in the coming week.

Oval Projects Engineering, Sugs Lloyd, Snehaa Organics, and Abril Paper Tech will close their initial public offerings (IPOs) next week.

Further, Anlon Healthcare, and Vikran Engineering from the mainboard segment will debut on the bourses on September 3, while investors will see a total of 11 listings from the SME segment.

Technical View

Technically, the Nifty 50 is looking weak though it has taken a support at upward sloping support trendline on the closing basis on Friday. The index traded well below short term moving averages which bended down on the weekly charts, along with formation of long red candle following shooting star kind of pattern (the bearish reversal pattern) in the previous week. The MACD maintained negative crossover with histogram trending below zero line, while the RSI at 49.7 sustained bearish crossover. Hence, if the index breaks trendline support (slightly above 24,400), the August low can't be ruled out next week as below it bears will get charged more, however, on the higher side, 24,700 is the crucial for a move toward 25,000, experts said.

F&O Cues

The fresh weekly options data suggested that the Nifty 50 is likely to face resistance at 24,500-24,600 (wherein the maximum Call open interest was observed) as sustaining above it can drive the index toward 25,000, however, the 24,400-24,300 is expected to be immediate support zone (wherein the maximum Put open interest was placed) followed by directly at 24,000 being the crucial support.

Meanwhile, the India VIX, also known as the fear index, has remained at lower levels with rangebound movement around short-term moving averages. Market participants need to stay alert in such periods of complacency, as the likelihood of a sharp move in either direction remains high. It was just up 0.21 percent during the week to Rs 11.75.

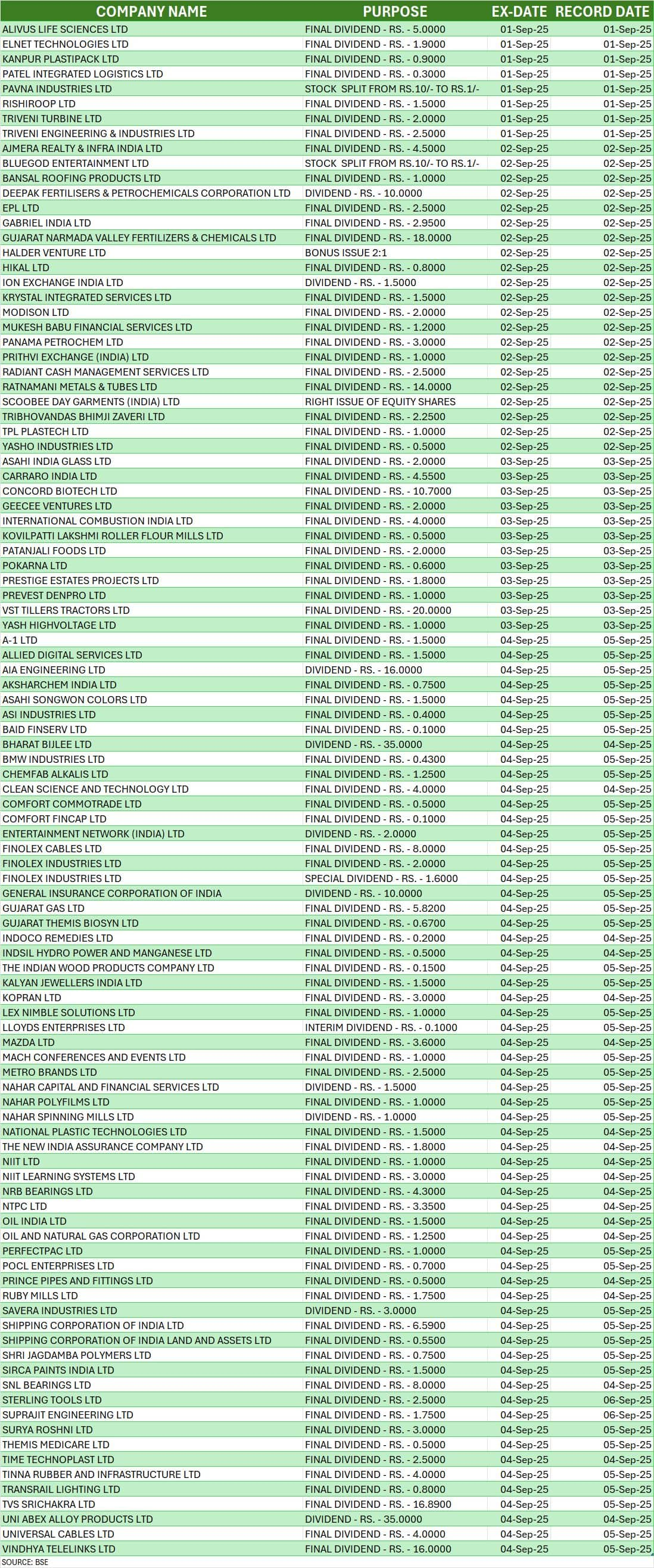

Corporate Action

Here are key corporate actions taking place in the coming week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.