The recent hardening of bond yields is bad news for wholesale borrowers like housing finance companies, particularly those which lend predominantly to the salaried. That is because of the spreads--difference between the rate at which the money is borrowed and then loaned—on such loans are thin.

The introduction of RERA (Real Estate Regulation and Development Act) was supposed to boost the housing sector—developers as well as mortgage lenders. Industry experts agree on the long-term benefits of the law. But in the short term, it has affected new real estate launches/loan growth of housing finance companies as many small builders struggle to meet RERA compliance norms.

Amid these headwinds, most of the companies in the sector have underperformed in the past six months. In a pre-election year, housing, especially for the “bottom of the pyramid”, will remain in focus. Against this backdrop, it is worth checking for housing finance companies which merit attention.

The push from the government coupled with the interest subvention under Pradhan Mantri Awas Yojana (PMAY) and sops for affordable housing like infrastructure status, tax deduction in profits should keep interest alive in low-ticket housing.

The "Credit-Linked Subsidy Scheme” (CLSS) under PMAY envisages the vision of housing for all by the year 2022. Under this scheme, interest subsidy on purchase/ construction/ extension/ improvement of house is provided to customers belonging to Economical Weaker Section (EWS)/Lower Income Group (LIG)/Middle Income Group (MIG).

| EWS/LIG | MIG1 | MIG II | |

| Eligible family income (Rs lakh per annum) | EWS -upto Rs 3 lakhs, LIG - over Rs 3 lakhs upto Rs 6 lakhs | over Rs 6 lakhs upto Rs 12 lakhs | Over Rs 12 lakhs upto Rs 18 lakhs |

| Max carpet area (sq m) | 30/60* | 120 | 150 |

| Subsidy calculated on max loan of | Rs 6 lakhs | Rs 9 lakhs | Rs 12 lakhs |

| Interest subsidy (%) | 6.50% | 4% | 3% |

| Max subsidy (Rs lakh) | 2.67 | 2.35 | 2.3 |

| Validity of scheme | Mar-22 | Mar-19 | Mar-19 |

| Woman ownership | Mandatory | Not mandatory | Not mandatory |

| * this norm is currently relaxed |

Repco Home (CMP: Rs 678 M cap: Rs 4241 crore) whose forte lies in lending to the unbanked derives nearly 60% of the home loan portfolio from the non-salaried class and has a major presence in Tamil Nadu. Over 80% of the loan book comprises of individual housing loan and the rest is LAP (loans against property).

FY17 was a bad year for the company marred by unfavorable regulations (Madras High Court order which banned registration of unapproved plots), demonetization, sand mining ban in the state and slippage of high-ticket LAP loans into NPL (non-performing loan). Consequently, disbursements declined 7% YoY in FY17. As a result, loan growth declined from 29% in FY15 to 16% in FY17 (and 10% in 1HFY18).

However, with some regulatory relief in Tamil Nadu and ebbing of demonetization woes, disbursement and loan growth should pick up. The loan book growth has started picking up in the states of Telangana, Kerala, Maharashtra and Gujarat.

Asset quality also worsened with gross non performing loans also increasing from 1.3% in FY16 to 2.6% in FY17 and then to 3.4% in 1HFY18. The company expects this to decline meaningfully and the asset quality has started improving in the LAP portfolio.

Repco has curtailed/stopped disbursements in high-ticket LAP, added employees at some high-delinquency branches to focus on recovery and reduced the share of LAP against commercial property from 36% in FY13 to 28% in FY17.

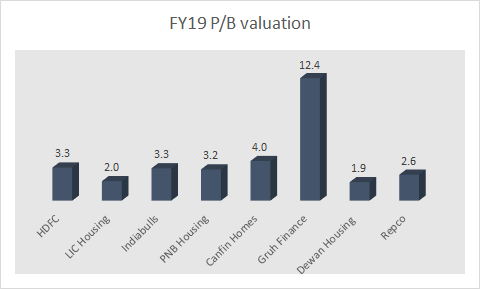

Repco’s rural penetration, average loan size of Rs 14 lakhs, competitive cost/income ratio, and ability to lend to non-salaried gives it an edge. The company has an intrinsically profitable business model with a net interest margin upwards of 4.5%, strong and consistent RoA (return on assets) of 2.2- 2.4% and RoE (return on equity) of ~17%. It is extremely well-capitalised with CAR (capital adequacy ratio) in excess of 22%. Therefore, it is a good business to look at when the going has been tough thereby rendering the valuation attractive at 2.6X FY19 book.

HDFC (CMP: Rs 1709, M cap: Rs 272953 crore) in contrast is a financial conglomerate and a large sized urban focused entity. But the consistency in performance and its ability to maintain margin across interest rate cycles makes us positive on this company.

HDFC intends raising Rs 13,000 crore capital. HDFC’s last capital raising was in FY07 with a dilution of 12%. This time around, including the capital raising and post conversion of warrants, it will be 7% over FY18-19.

HDFC intends to participate in growth via subsidiaries without compromising its own capital position and the additional capital raising is with the intent to maintain its stake in HDFC Bank (that is raising capital as well in view of its promising growth outlook), inorganic growth in general insurance via HDFC ERGO, acquiring distressed real estate assets via a separate fund and setup another fund to invest in equity and mezzanine debt of affordable housing projects. Close to 40% of the value of the company is now derived from subsidiaries.

On its core business front too, the institution has seen traction in both individual and corporate loans. Corporate loans is now close to 28% of the portfolio and helps in protecting margin when spreads on individual home loans are coming under pressure.

Gross NPL has largely stayed stable at 1.4% and NPL on the corporate book stands at 2.2%. Over the last sixteen quarters, Gross NPL for the non-individual segment have ranged from 1.0 to 1.2% but jumped sharply to 2.18% after slippage of Rs 910 crore in 1QFY18. With a provision coverage in excess of 100% on this book, an incremental spread of 1.15% (2QFY18) over the housing segment, and developer loans constituting financing against developer inventory, we believe this is a well-thought-out strategy and do not perceive the same as too risky.

The company has consistently maintained superior return ratios (ROA of 2.5% and ROE of 21%) and one of the lowest cost to income ratio. We see comfort in the current subsidiary adjusted valuation of 3.3X FY19 book.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!