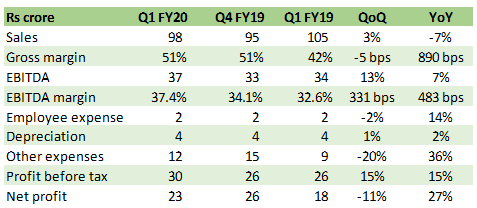

Specialty chemical player Seya Industries (market cap: Rs 980 crore) has reasons to be happy. It made good use of margin expansion to report 15 percent increase in profit before tax for the June quarter of FY20.

While the benzene-based player’s capacity utilisation is near optimum for the existing business, near to medium term volume growth will be decided mainly by its greenfield capacity expansion programme, which has seen 80 percent completion.

The vertically integrated operations and a strategy to focus on products with high import intensity have led to elevated operating margin. The company is likely to defend a sustainable operating margin of 25 percent plus over the long term even if China’s earlier closed capacities are revived. We remain positive on the stock, given its valuation discount to the peers in the benzene derivative space.

Table: Q1 financials

The firm saw a sales de-growth of 6.6 percent YoY (year on year) due to lower finished products volume (-3.6 percent) and realisations as the production in China stabilises. Sales volume was impacted compared to the year-ago quarter due to change in product mix requiring higher captive consumption.

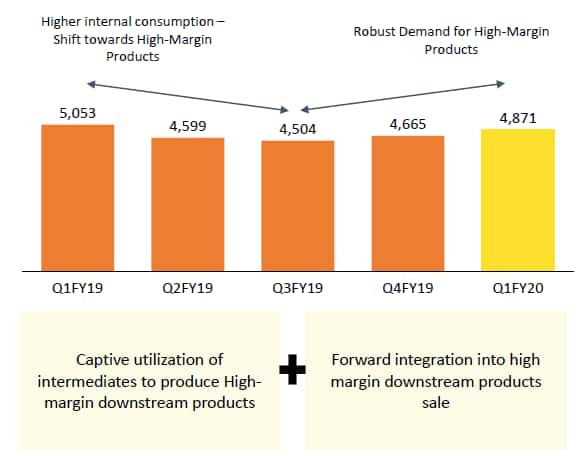

Sequentially, volume grew by 4.4 percent to 4,871 tonnes on increased demand for expanded capacity of the recently commissioned high value-added products. The company completed brownfield expansion of its key product, Para Nitro Aniline (PNA) in Q4 F19, which contributes about 20 percent to its FY19 revenue. This expansion doubles the capacity to 8,000 tonnes of PNA and hence, increases the exposure of hair dyes end market and veterinary pharma segments.

Chart: Volume trajectory

Gross margin improved YoY on the back of an improved product mix and lower input cost. This resulted in EBITDA (earnings before interest, tax, depreciation and amortisation) margin expansion of 483 bps YoY in spite of higher other expenses and employee cost. EBITDA per tonne increased by 13.8 percent YoY and 12.3 percent QoQ. Additionally, due to lower interest cost, profit before tax jumped 15 percent YoY.

Sequentially, however, there was a drop in other expenses. In Q4 FY19, higher other expenses were on account of the switchover to the expensive oil fired plant instead of the coal fired one. But this cost appears headed for normalisation as the company has switched back to the coal-based power facility.

Major observationsAmong the segments that are doing well in terms of demand-supply situation and pricing are printing inks and certain segments of pharma intermediates such as paracetamol. Chemical catering to hair dye segment and veterinary pharma (eg: PNA) have witnessed heightened volatility.

Capacity expansion projects on track: The Rs 735 crore mega capacity expansion programme is expected to be complete by H2 FY20. Already, 80 percent of the site completion has been achieved. The project will lead to more than six times jump in finished product capacity.

Top line contribution from the new capacity is likely to reach Rs 1,000-1200 crore by FY23 at an optimum utilisation of 80 percent. While the ambitious capex plan by itself presents an execution risk, the project’s progress so far and debt/equity profile (peak expectation of ~0.5x) provides comfort.

OutlookThe company’s foray into product range where there has been a high import intensity along with a steady domestic demand for varied downstream chemicals industries is a key driver for the medium term growth. According to the Department of Chemicals and Petrochemicals, nearly 70 percent of domestic demand for organic chemicals is met through import in India.

Taking into account the mega capex project and the lower end of the management’s guidance, we estimate revenue CAGR of 36 percent for the next 4 years.

Having said that, key profitability metric - EBITDA per tonne – may moderate due to product mix and normalisation in Chinese production disruptions, partially offset by vertical integration benefits. Already, at the sales level, we are witnessing moderation in realisation due to the China factor.

The management commentary suggests normalisation of supplies from China can possibly reduce the EBITDA per tonne performance to Rs 60,000 from 65,000 on a long-term basis. This guidance is limited to the existing product portfolio.

Considering the mega project, we believe that 25 percent would be a sustainable operating margin in the long run, which would be higher than prevailing sector margins.

Taking a conservative assumption, operating margin may drop to 30 percent in the near term. The stock is trading at 10.6x and 7.3x FY20 and FY21 earnings, respectively. We believe that the current valuations are at a substantial discount to peers in the benzene derivative space and offer investors an interesting opportunity for accumulation.

Follow @anubhavsaysFor more research articles, visit our Moneycontrol Research page.Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.