Madhuchanda Dey

Moneycontrol Research

MAS Financial Services, the Gujarat-based non-banking finance company (NBFC), reported a solid Q1 FY19 and showed no incremental deterioration in earnings quality under the new IndAs accounting standard from Generally Accepted Accounting Principles (GAAP) earlier.

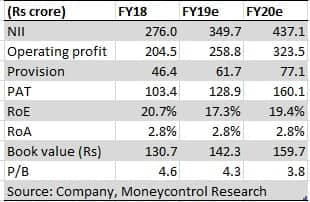

The management continues to grow the business with caution and healthy asset quality remains the key focus. The stock has stagnated in recent times and trades at 3.8 times FY20e book. While a multiple re-rating looks unlikely, investors should look at this stock for steady earnings trajectory in the mid-20s.

What makes MAS a niche player?

At present, the company operates across six states and Delhi, although majority of its branches are in economically vibrant states of Gujarat and Maharashtra. The business primarily focuses on loans to small businesses and individuals. There are four product categories: micro enterprise loans (MEL), small & medium enterprise (SME), two wheeler and commercial vehicle (CV). The company also has a housing finance subsidiary catering to affordable housing.

Source: Company

Knowledge of its end market and superior executionMAS has a unique sourcing model. In addition to its sales team, it has entered into commercial arrangements with a large number of sourcing intermediaries, including commission-based direct selling agents, and revenue sharing arrangements with various dealers and distributors, where part of the loan default are guaranteed by such sourcing partners.

The company has 108 small NBFC partners for sourcing business. The assets generated by these NBFCs are hypothecated to MAS. Over 58 percent of these assets have been contributed by these NBFCs.

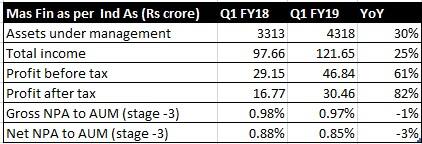

The NBFC has stringent qualitative and quantitative evaluation criteria that keeps a check on delinquency. This is reflected in the numbers, with gross and net non-performing assets at 1.19 percent and 0.95 percent, respectively. It is pertinent to note here that even as per IndAs the fundamental parameters have not worsened including NPAs (stage 3 assets), which is now identified on expected credit loss (ECL) criteria.

Source: Company

In the quarter gone by, riding on robust growth in assets under management, the reported numbers were encouraging. It is pertinent to note that in a rising rate environment, the management has succeeded in lowering its cost of borrowings from 8.98 percent in the year-ago quarter to 8.74 percent in the quarter under review, giving a kicker to margin.

MAS has been consistently reducing its cost of funds by diversifying its borrowing mix – non-convertible debentures, commercial paper, term loans and cash credit. Close to 37 percent of AUM is assigned to banks and financial institutions and the cost of funding from this source is quite competitive. Control over operating expenses also aided sharp improvement in profitability.

Source: Company

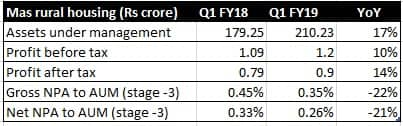

The housing finance subsidiary too reported steady performance, with revenue increasing 11 percent to Rs 7.3 crore and profit growing 14 percent to Rs 0.9 crore in Q1 FY19. The total AUM rose 17 percent to Rs 210 crore.

The company is very well capitalised (capital adequacy ratio at 29.5 percent) and should have a steady road ahead.

Despite the optically expensive valuation, we recommend stock for its consistency – a strategy that is likely to pay dividend in the long term. Investors looking at returns in the mid-20s should look to buy this company.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.