Madhuchanda Dey Moneycontrol Research

Asset financing companies are at a crossroad. While vehicle finance, its principal business, is experiencing opportunities from robust volume growth, especially from the commercial vehicle side, the rapid escalation in fuel prices raises questions about the sustenance of cash flow of customers, namely fleet operators. The rural economy is on the mend with a normal monsoon, pre-election largesse and expected rise in the minimum support price. However, sharp hardening of bond yields and expectations of a rising trend on account of firming up of crude oil and falling dollar-rupee signals further pressure on borrowing costs.

Stock prices have fallen in the past three months in light of the myriad concerns. Are these companies ripe for accumulation or are we staring at a period of prolonged pain?

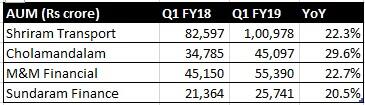

A decent Q1 FY19 Asset financing companies reported a decent performance in Q1 FY19. Average growth in assets under management (AUM) stood in mid-20s. For Shriram Transport Finance Company (STFC), the growth was aided by new vehicle loans, business loans and working capital. For Cholamandalam Investment & Finance Company (Cholamandalam), growth was driven by vehicle finance, even as the management continued its cautious growth strategy with respect to the home equity business. M&M Financial Services (MMFSL) saw strong traction in tractor, commercial vehicles and small business loans. For Sundaram Finance, the growth drivers were construction equipment and tractors.

Source: Company

The hardening of wholesale funding rates impacted net interest margin for all the players on expected lines.

Source: Company

Despite moderation in interest margin, robust growth in assets under management (AUM) led to significant improvement in net interest income: the difference between interest income and interest expense.

Network expansion continued, although it is heartening to witness growth in operating expenses, lagging growth in loan assets.

Source: Company

Another significant kicker for earnings growth in the quarter under review has been decline in provisions. STFC, for instance, has maintained its high provision cover (amount of provision held for non-performing loans), despite decline in provisioning, thereby indicating an improvement in underlying asset quality. Cholamandalam too saw an improvement in provision coverage despite a year-on-year decline in absolute provision. Sundaram saw a decline in provision, with a reduction in coverage ratio. MMFSL saw an increase in provision, thus improving its lower coverage ratio.

Going forward, with improved dynamics of the end-market, we expect credit cost to stay subdued and should provide a major earnings kicker.

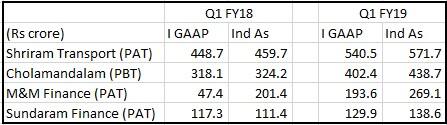

One of the highlights for the quarter gone by was presentation of accounts as per the new accounting standard: IndAs. Implementation of expected credit loss (ECL) criteria led to lower provisions compared to the earlier accounting standard (I GAAP) for MMFSL, Cholamandalam, Sundaram as well as STFC. Consequently, profitability improved under IndAS.

Source: Company

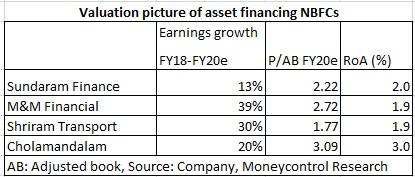

What are the stocks to look at?

While rural demand looks supportive on the back of pre-election spending, normal monsoon and hike in MSP, the dream run in the automobile segment faces speed breakers in the form of higher fuel prices. The ambiguity surrounding enhanced axle load norm might impact CV demand. Hence, sustainability of asset growth can’t be taken for granted. The steep hike in funding cost would impact interest margin as the entire hike may not be passed on to end-customers.

Of the companies under review, MMFSL has a diversified portfolio and is well entrenched in the rural geography. We see little risk to double-digit growth. With improvement in the end-market, after the migration to 90-day non-performing assets (NPA) recognition norm, credit cost normalisation should support earnings despite a decline in interest margin on account of rising wholesale rates.

Cholamandalam too has a diversified vehicle and home equity portfolio and has maintained pristine asset quality, while registering profitable growth. It is likely to continue on this path. However, valuation captures the positives. So, investors should await a better entry opportunity.

We are circumspect about traction in the second hand vehicle market of STFC as the non-second hand vehicle businesses have grown faster in recent times. This could impact profitability going forward as its margin is much lower. However, the steep 17 percent correction in the stock in the past three months has captured part of the concerns. For the long-term investor, we feel the stock is beginning to offer value.

Sundaram, with diversified business segments, will be a key beneficiary of the multiple growth drivers across various financial services. We expect the company to grow its lending book, albeit at a gradual and steady pace. Additionally, the other financial services business like AMC and general insurance are expected to grow in sync with India’s economic growth.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!