Sachin Pal

Moneycontrol Research

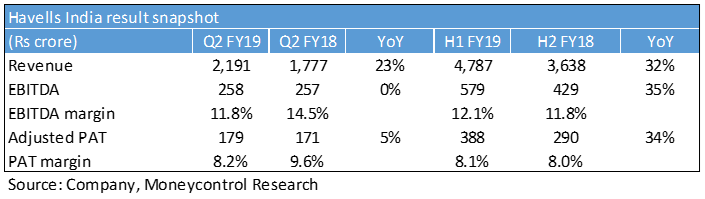

Havells India reported a stable set of Q2 FY19 earnings. The company delivered strong topline growth, but operating profit came in flat as inflationary cost pressures resulted in higher input costs. Also, advertising and promotion expenses were higher year-on-year as the company had limited marketing expenses in view of last year's Goods & Services Tax (GST) rollout.

Revenue increased 23 percent year-on-year (YoY) to Rs 2,191 crore. Earnings before interest, tax, depreciation and amortisation (EBITDA) stood at Rs 258 crore in comparison to Rs 257 crore YoY. Profit after tax came in 5 percent higher at Rs 179 crore in comparison to the same quarter last year.

Strong topline growth across business segments

Switchgear segment revenues grew 28 percent after a period of sluggish growth in the past few quarters. Performance in the segment was aided by a low base as well as higher industry demand as a result of the Centre's focus on electrification projects.

Revenue growth of 35 percent in the cables and wires segment was driven by a combination of volume and price hikes. The sharp increase in commodity prices, especially copper, had impacted margin over the past 12-18 months. Margin softened on a sequential basis as input prices remained unfavourable. For Q2, margin came in at 14 percent as compared to 20 percent in the year-ago period. Over the long run, the management expects margin to remain in the 15-17 percent range.

New product launches (water purifier and personal grooming) and deeper market penetration led to an increase in market share and drove growth in the consumer durables segment. The segment delivered revenue growth of over 40 percent as fans and other products continue to gain customer traction. Margin remained largely stable despite the changing product mix.

Adjusted growth of 18 percent in the lighting and fixtures segment (excluding Energy Efficiency Services - EESL) was aided by deeper distribution and higher B2B (business-to-business) and B2C (business-to-consumer) sales. Volume growth came in 30 percent higher, but the price erosion in the LED business dragged overall topline. Absence of EESL orders resulted in a sharp decline in the segmental revenue during the quarter gone by. The company does not expect any new orders from this business line.

Lloyd Electric had reported a very strong Q1 on all fronts. However, performance in Q2 was in sharp contrast to the previous quarter as unseasonal rains had an adverse impact on the business, which resulted in a topline reduction of 4 percent. Higher channel inventory as well as currency devaluation kept input costs at elevated levels.

Havells continues to expand Lloyd's portfolio as well as increase its distribution through tie-ups with modern retail stores. It also plans to reduce import dependency for the Lloyd's business by setting-up local manufacturing capacities.

Capital expenditure for FY19 is pegged around Rs 500 crore. Majority of these funds (Rs 280-300 crore) will be used to set-up a 6 lakh unit air conditioning manufacturing facility for Lloyd, which is expected to be operational by FY19-end. Going forward, the annual capital expenditure is expected to be in the range of Rs 200-250 crore.

Outlook and recommendation Over the past couple of years, Havells has gained a strong foothold in the sector with the launch of new products and gain in market share across segments. While topline is expected to grow at a steady rate, margin is expected to be under pressure in the near term on account of higher commodity prices as well as currency depreciation.

Over the long term, the company seems well positioned to benefit from an expanding distribution network and increased brand visibility. Repositioning of the Lloyd brand and expansion of its product portfolio seems to be going on track. Reduction in GST rates on white goods (TV, washing machine, refrigerator etc) should further spur consumer demand.

The stock currently trades at 38 times FY20 projected earnings and seems priced to perfection. Given its strong positioning, we recommend accumulating the stock during corrections.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.