Bhansali Engineering Polymer (BEPL) posted a weak set of Q2 FY19 earnings on lower margin. While currency and input cost vectors had led to expectation of a margin contraction, unhedged trade payables worsened the impact.

Going forward, we expect margin to improve as the company is able to pass on higher input prices to end customers. While volatility in input prices remains a key factor to watch out for, the company’s improving market share, on the back of operationalisation of new capacity, provides some assurance on earnings growth.

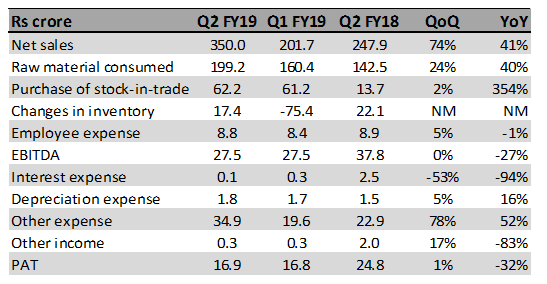

Gross margin severely impacted in Q2

Source: Company

Compared to Q1 FY19, which was impacted by disruption of production on account of a fire, sales have improved 74 percent quarter-on-quarter in Q2. Sales run rate is higher than one witnessed in Q4 FY18 (Rs 302 crore) on account of higher product pricing and operationalisation of additional capacity (20,000 tonne per annum).

However, the negative surprise was due to contraction in gross margin (-715 bps QoQ and -774 YoY). Consumption of raw material spiked 24 percent QoQ. While operating leverage was helpful, surge in forex losses (Rs 11 crore in Q2 FY19) led to weak earnings before interest, tax, depreciation and amortisation (EBITDA) margin (7.9 percent versus 15.2 percent in Q2 FY18).

Excluding forex loses, EBITDA margin is more respectable at 11 percent.

Unhedged forex exposure As per the company’s balance sheet, foreign currency exposure through short term borrowings is nil. The company had paid off its short term and long term borrowings from both external and domestic sources.

Foreign currency exposure is only through trade payables. Of its trade payable of Rs 125 crore, 88 percent was from external sources. Since this is unhedged exposure, it reported a forex loss in Q2 on account of a sharp currency depreciation.

Raw material prices soften in the current quarter Coming to raw material prices, the company imports 85 percent of its raw materials (styrene and acrylonitrile), which leaves it vulnerable to global oil derivative price levels and currency movements. Unlike its key competitor - INEOS Styrolution, the management maintains a low inventory of imported raw material so as to keep its forex exposure limited. Since INEOS Styrolution holds inventory for a longer period (about six months), it might post a relatively better earnings (Q2 FY19) as recent raw material fluctuation and currency movement would have had a lesser impact.

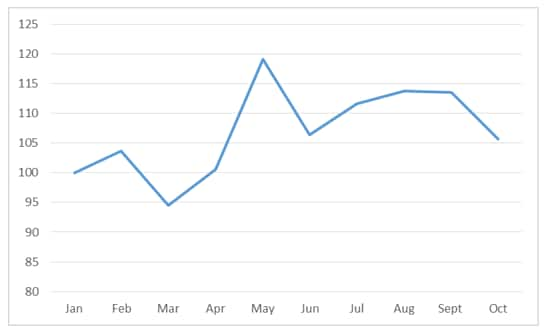

Styrene monthly price trend (indexed) in China

Source: sunsirs.com, Moneycontrol Research

Styrene prices have been volatile this year with an upward bias. Global styrene prices have been aided by unplanned shutdowns, anti-dumping duties and trade tariffs. ICIS, the world's largest petrochemical market information provider, mentions that trade tariffs from China on US products could be up to 80 percent. New supply from China is on anvil and represent 25 percent of current demand. In the medium term, there may be a moderate upside in prices at best. In the short term, however, trade war and retaliatory tariffs can keep pricing volatile.

Styrene projects under construction in China

Source: ICIS

While we expected margin pressure on account of both rupee depreciation and raw material prices, quantum of impact has been a surprise. We expect normalised EBITDA margin of 11 percent to improve from here as company would be able to pass on raw material price hike partially with a lag. The company’s deliberate policy of maintaining low raw material inventory would be positive in the medium term as it lowers its exposure to volatile input prices and currency.

After the result, we have upgraded our near term estimates for topline on the back of higher utilisation of new capacity addition. In case of operating margin, we expect a moderation compared to FY18 but see it rebounding from Q2 lows to a reasonable 13 percent. The stock is currently trading at 13 times FY20 earnings estimates. While this is ahead of its trading multiple for commodity chemicals, it is justified given the company’s dominant position in the duopoly market of acrylonitrile butadiene styrene (ABS), client stickiness and growing expertise in specialty grades.

While the company is already witnessing improved market share, its planned mega capacity expansion (200,000 tpa in FY21) is expected to bridge the domestic demand and supply gap. Given this context, investors with a long term horizon can start looking at the stock for accumulation.

For more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.