When cryptocurrencies first gained prominence, they were touted as being more secure than real money. However, for Indians who bought into the bitcoin dream, the process of filing tax on gains accrued from the cryptocurrency could prove to be a nightmare.

Under Indian law, the status of investments in virtual currencies remains unclear. The Reserve Bank of India (RBI) released a series of conflicting statements indicative of its uneasiness regarding the regulatory framework governing cryptocurrencies. But for investors who hold virtual currency, paying taxes is inescapable, despite the authorities’ ambiguous stance on the validity of such investments.

The income tax (I-T) department surveyed cryptocurrency exchanges across the country in December 2017. It served notices to 5,00,000 investors for tax evasion. Since then, bourses have also come under the scanner of the I-T department.

The RBI has outlawed cryptocurrencies and prohibited banks from dealing with investors or exchanges. But people who had invested in cryptocurrencies before the RBI’s diktat to banks are liable to pay taxes. There is no separate statute in the law book detailing tax norms for cryptocurrencies, but the law is clear on taxing income irrespective of the form in which it is received.

Here are a few scenarios where dealings in cryptocurrencies are likely to be taxed.

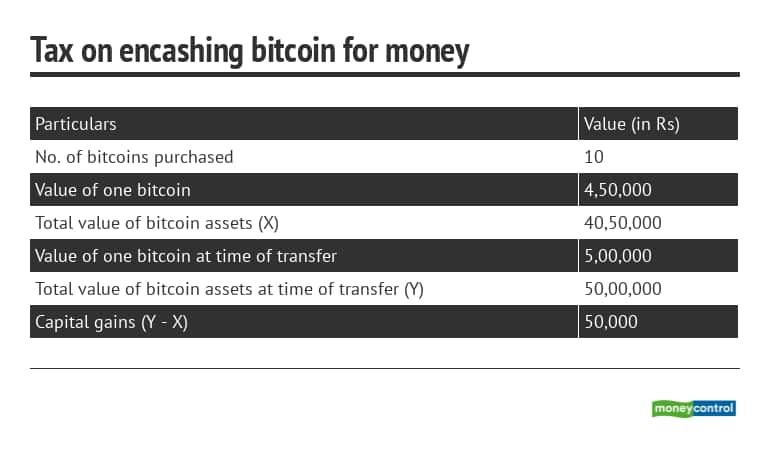

1. Investment in cryptocurrencies exchanged for real money

If money held in the form of cryptocurrencies is transferred in return for real money, the same rules applicable to income from capital assets, such as long term capital gains tax, will be applicable. Long term gains will be taxed at a flat rate of 20 percent, while those accrued over a shorter term will be taxed according to the slab it falls under.

For example, in the above case, the capital gained is Rs 50,000. If this was accumulated over the long-term, it will be taxed at 20 percent. The I-T department could make use of an ambiguity in the statute book to classify such transactions as “income from other sources” rather than as capital assets. This can be beneficial since income above Rs 10 lakh will be liable to be taxed at 30 percent, as opposed to the flat 20 percent for long-term capital assets.

2. Bitcoin mining

Mining for cryptocurrencies is a capital intensive activity as it requires large amounts of electricity and expensive hardware. But ultimately, income generated by mining is self-generated. This means that the cost of acquisition cannot be ascertained.

Moreover, cryptocurrencies are not included in Section 55 of the Income Tax Act, 1961, which lays down the template for computing the cost of acquisition for self-generated assets. The implication of this would be to exempt miners from the tax net, till such time as the government decides to amend the I-T Act to accommodate income from cryptocurrencies.

3. Cryptocurrencies held as stock-in-trade

Trading in cryptocurrencies gives rise to income from business, thereby directly qualifying profits arising out of such deals for taxation under the different slabs set by the law.

4. Payment for goods and services

Many Indian vendors have started accepting cryptocurrencies like bitcoin and ethereum as payment for goods and services. Even though such firms are in the minority, the volume and total value of such transactions is quite substantial, for tax to be foregone.

If a vendor is paid in cryptocurrency, it will be considered as income from business. This implies that tax will be levied under the head profits or gains from professional business, as is applicable to trade in the conventional sense. Depending on the quantum of such transactions, the total income will be taxed as per the rate of the slab it falls under.

However, as of now, the government does not recognize cryptocurrencies as legal tender and is working with the RBI to formulate a draft legislation to regulate their use in the country. There is a disclosure requirement regarding cryptocurrencies in I-T return forms, but the absence of well-defined guidelines regarding their taxation is lending to confusion among Indians holding on to their crypto assets.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

| 1W returns21.01% |

| 1W returns17.52% |

| 1W returns12.29% |

| 1W returns8.22% |

| 1W returns7.37% |

| 1W returns5.99% |

| 1W returns5.98% |

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.