Krishna Karwa Moneycontrol Research

Bata is one of India’s most popular footwear and accessories brands.

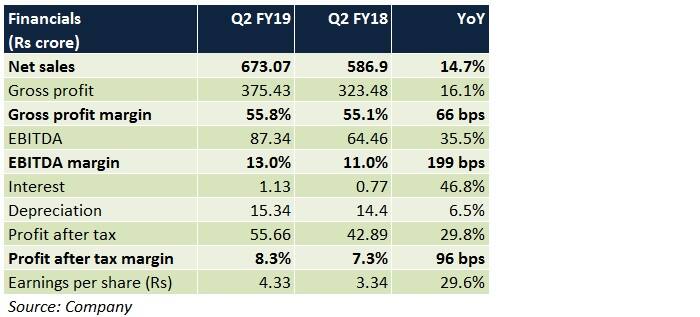

In the quarter gone by, sales growth was attributable to store additions, success of the ‘Be Surprised’ campaign and operationalisation of 50 new ‘Red Angela’ outlets (an international store concept that commenced operations in Q4 FY18). The latter two attracted high footfalls. A higher share of sales from premium products and cost efficiencies aided margin expansion.

What will drive revenue growth?

To attract more footfalls, store renovations are being undertaken. Furthermore, experience centres and kiosks are likely to be introduced in a phased manner at the outlets.

Spends on promotional activities are anticipated to increase from Rs 40 crore in FY18 to nearly Rs 80-90 crore by FY19-end. Besides coming up with new and innovative marketing programmes from time to time, celebrity-backed endorsements will be undertaken extensively to strike a chord with present and prospective buyers.

New offerings in select segments (for instance - ‘Red Label’ brand of women’s footwear, youth collections, sports footwear) are expected to gain traction on the back of visual merchandising initiatives and new exclusive brand outlets (EBOs).

In the value footwear space (ie. products priced upto Rs 1,000), reduction of GST rate from 18 percent to 5 percent will drive sale volumes.

To cash in on the rising popularity of online shopping, Bata is developing its website and mobile application to reach out to a wider audience. This will complement its brick-and-mortar sales.

Going forward, as the inclination to purchase branded and trendy footwear gains momentum, the management has outlined plans to leverage the digital platform optimally through social media posts, regular blogs and advertisements.

100-150 new retail stores will be opened each year in the coming fiscals to augment Bata's network of 1375 outlets (at the end of FY18), particularly in the smaller cities and towns of India. Most of these will be opened under the franchise route to keep capex limited.

How can margins improve?

Emphasis on improving stock management processes should reduce the strain on Bata’s working capital.

To facilitate cost rationalisation, rent agreements are under negotiation at a few locations and the possibility of opening smaller-sized stores in future is on the agenda.

The contribution of premium branded products, which fetch better realisations, is slated to gradually increase from the 25-30 percent mark in FY18.

Risks

An unfavourable sales mix in certain months, wherein the share of wholesale channel revenues are higher than that of the retail channel, could lead to a build-up of receivables, thus impacting cash flows.

Extended end-of-season-sale periods, which necessitate taking price cuts, may dent margins.

Stiff competition from foreign brands, other Indian players, unorganised entities and e-commerce portals will continue to persist.

Should you invest?

Bata as a brand is widely recognised in India, especially in the mass and mid-premium category. By refreshing its product portfolio, the company has managed to reposition itself strongly. Impetus towards enhancing the shopping experience of customers and efforts to boost the omnichannel should help the company gain market share in due course.

Given Bata’s robust fundamentals and its ability to derive healthy operating margins (in spite of high marketing spends), it is not surprising to see the company trading at lofty valuations of 42 times its 2-year forward earnings.

The stock, after witnessing a sharp dip until barely a fortnight ago, has managed to rebound pretty quickly from its 3-month low of Rs 858.6 (as on October 23, 2018). We advise investors to keep a watch on volatility-induced price corrections before placing the buy order.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.