Fintech lending startups were one of the biggest beneficiaries of the COVID-19 pandemic as business boomed when people facing business distress or coping with a job loss scrambled for loans. Now, as the year draws to a close, these lenders are the ones in distress, scrambling to offer those same customers restructured options as defaults rise.

The lending startups have also come under scrutiny due to alleged harassment of borrowers, which has resulted in deaths. On December 23, the Reserve Bank of India (RBI) took note of the unbridled growth of these platforms.

Platforms that cater to organised and salaried customers are still better off, but lenders processing business loans are facing trouble collecting repayments from enterprises that bore the brunt of the pandemic.

Though overall industry numbers are not out yet, people who track the segment said repayments for business loans are likely lagging at 50-60 percent. Repayments for consumer loans are back at 90 percent and sometimes more, they said, requesting anonymity.

Restructuring loans

Industry insiders Moneycontrol spoke to pointed out that startups are trying to connect with borrowers who are not able to repay, looking to restructure their loans in line with RBI guidelines. This will allow them to show these loans as "standard" assets on their books, they said.

The fintech lenders are hoping for a quicker recovery in the March quarter, thereby making up for lost business during the pandemic. A healthy balance sheet is essential for VC-backed tech-enabled lenders to get decent valuations and attract quality equity investors in their follow-up rounds, said a top lending executive, speaking on condition of anonymity.

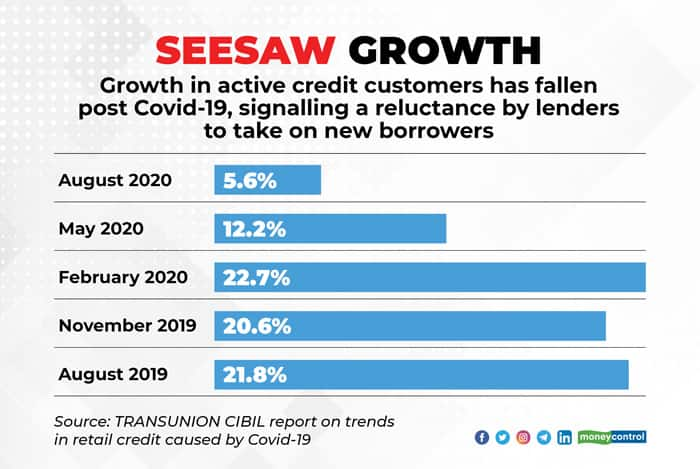

Both enquiries and approvals have fallen

Not only have inquiries dropped, approval rates have fallen, too. As per data shared by Cibil, approval rates fell by 3.5 percent for NBFCs and 7.5 percent for fintechs in August 2020 compared to the corresponding period last year. This shows that the overall sector is not only getting fewer loan applications, but also approving fewer loans, fearing stress on credit quality.

“The trend that we are observing is that consumers in the third and fourth bucket of defaults are going non-contactable. This means they are not in a position to repay and lenders will need to classify them as NPAs,” said Abhishek Agarwal, Chief Executive Officer, CreditVidya.

Mumbai-based CreditVidya works with lenders, helping them decide on the credit worthiness of their customers.

Third and fourth bucket consumers are those who have not repaid their loans even 60 days after the due date.

In terms of delinquency, as of August, fintechs saw their bad asset base shoot up to as much as 6 percent in August from 2.5 percent in 2019, data from Cibil shows.

Where is the stress?

Industry experts pointed out that fintechs that were lending to consumers with salaries are somewhat on safer ground and many have also seen business getting back to near normal. For instance, Early Salary, which solely caters to salaried customers, had told Moneycontrol that it had seen more than 80 percent of borrowers repay their loans even during the pandemic.

“Consumer durables as a segment saw business getting back to near-normal during the festive season. Lenders processing such loans might be doing around 50-80 percent of their pre-Covid disbursals as an industry average, depending on their size and risk appetite,” said the founder of a top fintech lending platform on the condition of anonymity.

He added that the biggest stress is in the SME lending space, where businesses have seen their cash flows getting disrupted for quite a few months during the lockdowns. Many of the small merchants have not been able to recover from that blow yet, he said.

In the case of job losses, many consumers who had taken personal loans had opted for the moratorium and are looking to restructure their loans now, so that they can repay over a longer tenure.

“Around 5-8 percent of our overall loan book has gone into restructuring. We have connected with borrowers who were not able to repay loans, looked at their bank statements and offered them longer tenures,” said Kunal Varma, cofounder, Moneytap, an app-based lending platform that offers credit lines and personal loans to consumers.

Personal loans still in the green, SMEs not so much

Varma believes that those in the salaried segment, which he caters to, understand the importance of a bureau score and are keen to repay their loans. But the problem is more acute for lenders who lend to the blue-collar segment and among daily-wage earners, who might have lost their jobs in urban areas and had to migrate to their home towns and villages. Connecting with them and collecting from them could be a challenge, he felt.

“We look at fraud checks seriously, matching the address of the applicant. Their permanent address is recorded as well. If they cannot be found in any of the places, then those can be cases of fraud,” he said.

In the case of business loans, the tenures tend to be longer and the value given out tends to be higher as well. In India, merchants take goods on credit, sell them to their consumers, get cash, repay their loans and book the rest as profits. Now, when consumption has gone down, businesses have seen their cash flows getting disrupted.

For large-value MSME loans, recovery and collections could both be a challenge.

Abundant caution

Industry experts pointed out that from here on, the lending startups will exercise abundant caution. There are a couple of points playing out in the industry; first, there is availability of liquidity in the system; secondly, there is demand since consumers need credit to restart their lives. The repayment stress will continue well into 2021.

Also, larger, well-capitalised players might show a higher risk appetite and grab market share next year, leading to some loss in business for fintechs, who might want to conserve capital and recover existing loans.

In a report titled ‘NBFC Sector in India: A brief update post Covid’, consultancy firm Alvarez and Marsal pointed out that that 10-15 percent of the customers who opted for a moratorium could see defaults, thereby pushing up overall NPA numbers by 300-400 basis points. Around 50 percent of those who took the moratorium could opt for restructuring of their loans and lenders could see a spike in their credit costs, too, the report added.

Gold loans and credit cards see uptick

There is already a spurt in demand for gold loans, which is a secured form of personal loan. Bankers in the know pointed out that they are more comfortable giving out secured loans in the aftermath of the pandemic, given that consumers across the board could be in tough financial situations.

Another fallout could be the rise in credit cards in the market. As per the Cibil report, origination volumes in August were back to 51 percent compared to last year. This number had fallen to less than 10 percent during the pandemic, when credit card origination had almost come to a halt.

“We are doing 100 percent more transactions these days from pre-COVID levels, as consumers are looking for buy now pay later options and credit cards as their preferred choice of digital payment instrument, working in favour of a post-pandemic world,” said Rajan Bajaj, founder of Slice which is alternative to traditional credit cards for young Indians.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.