")

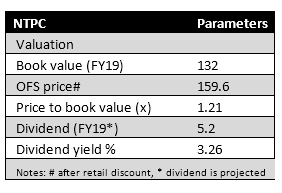

Participating in NTPC’s offer for sale (OFS) could be a sensible decision for retail investors who would be getting an additional 5 percent discount on the cut-off price. The government is offloading 10 percent stake in the company at a floor price of Rs 168 a share, which post discount works out to Rs 159.6 per share for the retail investors.

Is there value at Rs 159.6?What is worth noting is that at the discounted price the valuation works to about 1.2 times its estimated FY18 book value and offers a dividend yield of close to 3.3 percent, which is quite attractive.

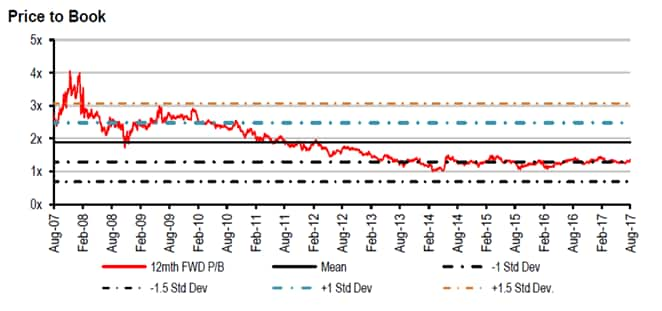

If one looks at history, there is very little chance of losing money at these valuations. Over the last 11 years, the stock of NTPC has traded in the band of 1 to 4 times its forward book value. Interestingly, in this period, it touched the levels of one-time book value only twice, in 2014.

While valuations are certainly in favour of investors, what drives the comfort further is the good earnings visibility. NTPC, which is the largest power generation company with annual generation capacity of 44000 MW, earns a regulated return. For every rupee of equity invested in the operational power plant, the company is allowed to earn 15.5 percent (regulated return) return by Central Electricity Regulatory Commission.

Unfortunately, the company’s reported RoE is much lower at 10.6 percent as large amount of money is invested in projects which are under execution or construction.

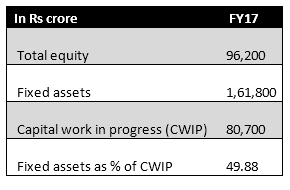

For instance, currently close to 20,000 MW of capacity is under construction and consequently funds to the tune of about Rs 81,000 crore are held in projects under construction or capital work in progress (CWIP). This money is not earning and forms close to 50 percent of the fixed assets employed in the business.

Thankfully this is going to change with the company now aiming to add 5000 MW of these under construction projects over 2018-20 and the rest by 2022. As projects become operational, the ratio of CWIP to fixed assets would improve to 19-20 percent by the end of 2022 as against 50 percent currently.

How would this help?The management mentioned that it would help in increasing its regulated equity (equity capital that generates 15.5 percent regulated returns) by 50 percent over the next three years and 100 percent by the end of five year.

As the regulated equity jumps, it would lead to higher profits and improve return ratios like RoE (return on equity). Therefore, the earnings visibility is higher for NTPC which could actually lead to a valuation rerating as the earnings momentum starts to kick in. Our internal estimates suggest that earnings over the next three years should grow as the regulated equity jumps, it would lead to higher profits and improve return ratios like RoE (return on equity).

Our internal estimates suggest that earnings over the next three years should grow by at least 15-16 percent annually. This is quite good considering that over the last four years the earnings have actually declined by 7 percent annually.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.