Thirty-five thousand views in five hours. That’s how many views Nisha Madhulika’s YouTube channel gets every time a new video is posted. She put together a recipe for thekua, a niche Bihari sweet eaten only during Chhath Puja, and the viewers in the comments thanked her for her work. Madhulika has no formal training. In 2007, when she started her recipe blog, people loved her food. So she decided to make it for the world. Now, 12 million people follow her to watch her cook.

Madhulika is a creator. Tomorrow, if, say, a spices brand wanted to reach their audience, instead of carpet bombing advertisements during an Indian Premier League-like event, it may decide to ask Madhulika to mention the brand and extol its virtues. The brand will pay her handsomely for it. This is the power of a creator.

In the last decade, creators have been able to build businesses around their creations, and monetise their skills. To paint a clearer picture, in India, over 45 percent of the people use smartphones and, according to a Bain & Co report, India’s online video user base is over 350 million. According to Elevation Capital research, globally, professional creators make an average earning of $3,500. India has just started to scratch the surface, and is expected to see rapid growth soon.

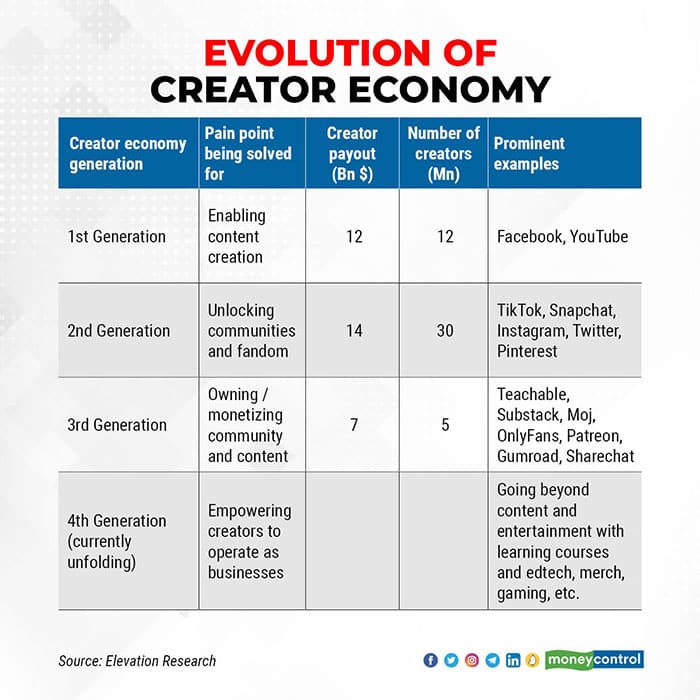

The First GenerationThis is the age of the solopreneur. The evolution of the creator economy will now rely on building businesses around these creators. Be it a fintech product to help them organise their earnings and pay tax, or a way of finding new platforms on which they can sell their services.

Almost a decade before terms such as influencers started gaining popularity, there were YouTube and Facebook. Let's call them first generation platforms. The digital platforms that first allowed users to upload their content. While creators could generate revenue on YouTube, it was primarily done through a share from advertisements, and Facebook was still years away from launching its monetisation at scale.

The two platforms were game-changers in a way that they introduced viewers to a new form of content that was personal in nature and got them hooked, thereby sowing the seeds of the creator generation.

What had started with Facebook took shape on spaces such as Instagram and Pinterest. Let’s call them second-generation platforms. The difference was the focus of these platforms. They were multimedia-rich. These platforms encouraged people to create a more polished version of the content. While Facebook was for friendships, Instagram was about discovering newer ways of seeing the world.

So, images and videos here were more consciously curated, more attention was paid to presentation. For example, a makeup artist could upload a video showcasing their skills, and there was an audience waiting to learn. The exhibitive nature of these platforms led to the creation of communities catering to specific needs — beauty, healthcare, fitness, education, etc. Creators with a great number of followers became influencers, and formed their own fandom.

But for a long time, the only way of revenue generation for Instagram creators was by monetising their skills off-platform through brand collaborations. Today, an Instagram creator with a following of 100,000 can earn about $200 per post.

This economic shift happened as content creators started becoming as important as their content.

The Third GenerationWith the rise of platforms such as Patreon and OnlyFans, focusing their attention on creators, smart and creative modes of monetisation came up. Let’s call these third-generation platforms. Here, users would be made to feel a part of the creator economy ecosystem in a way that they weren’t paying the creator but contributing towards their work. For example, a user could gift an e-coffee to the creator worth Rs 500 instead of depositing money directly into their account. Patreon, Teachable, OnlyFans, and Gumroad enabled monetisation through subscriptions, courses, commerce, shoutouts, tipping, and virtual gifting.

This has propelled creator earnings, which have increased to 1.5-3x on the third generation platforms when compared to the first and second generation platforms. For instance, the biggest subscriber-only platform Patreon made $1 billion worth of creator payouts in 2020, which is $5,500 per creator. Online course creation platform Teachable paid $500 million while content platform OnlyFans paid $1.6 billion. In India too, platforms like Graphy and Spayee are helping individuals become full-time creators.

These influencers are entrepreneurs in their own right; they are their own brand. Users today aren’t following platforms; that ownership has moved to the creators. Even after TikTok was banned, the fans of these creators moved with them to Instagram, Moj, and YouTube. To keep their content cycle running, there will be a need to not just create video editing tools, but also to help them manage their fans, communities, and the branded content deals these creators make. A customer relationship management tool, which can help boost not just influencer reach but also earning potential, is waiting to be created.

The Next GenerationProductivity tools that help the creator make more of their time too are still missing. A fintech tool that makes remittances easy for creators of any age or educational qualification is part of the white space.

Talking about education, currently, the focus is on creating entertainment content. But the next generation will create instructional content. The likes of Maven in the United States are attempting to do some of this. There will be a need to upskill as well. Creators will need to learn to do more. Platforms, which cater to creators will be needed.

Apart from this, software that helps creators make new kinds of content will be in demand. Creators’ ability to turn their work into non-fungible tokens, which can be sold across platforms, will give them greater reach. Software products that help them do that will be a necessity.

We are also excited about the opportunities that Web3 unlocks in creator monetisation. Digital art collectives like Hashmasks — a project with 70+ global artists collaborating — have seen $100M in traded volume. Royal.io allows musicians to fractionalise ownership of their music and fans to purchase it and share upside through royalties. All of this is made possible by a fundamentally new paradigm of verifiable ownership, fractionalisation, and global accessibility that has been heralded by NFTs.

Opportunity For MoreThis is the true creator economy. An entire ecosystem of businesses that are being built around the creator. Any and all types of content creation. Each part plays a role in the growth of this system.

As content creation gets decentralised and personalised, so will the creator economy. Essentially, this will mean that there is an opportunity to make distinct products for verticals beyond entertainment in fields such as finance, and health & wellness. With the size of the creator economy reaching ~$100 billion, the scales now are tipped in the favour of influencers who have the potential to earn salaries higher than bankers.

One can argue that the creator economy has just started to take shape. There are many more layers that will be built on this.

Disclaimer: Elevation Capital is an investor in Sharechat, Moj, and Unacademy (which owns Graphy, Spayee), mentioned in this article.

Mayank Khanduja is Partner, and Amit Aggarwal is Principal, at Elevation Capital. Views are personal, and do not represent the stand of this publication.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.