I had the chance to recently speak with a financial planner who was frustrated with his life’s work managing money for other people. “No matter what I did, I could never beat the S&P 500,” he conceded. This is normally when I share my smug efficient-markets-hypothesis-adherent wisdom, and how active management always comes up short. But as we chatted about his strategy, I realised he was also a believer. His problem, though, was not picking the wrong stocks; his problem was that he was doing everything I thought was right.

Let me explain. Financial theory suggests that investing in the benchmark S&P 500 Index is a good starting point for investors. But doing so leaves you under-diversified. I learned early on that the one of the biggest mistakes investors make is home bias, which is investing too much – or even entirely - in one’s own country. Many studies have shown that you’ll get a better return by investing in other countries as well and with less overall risk.

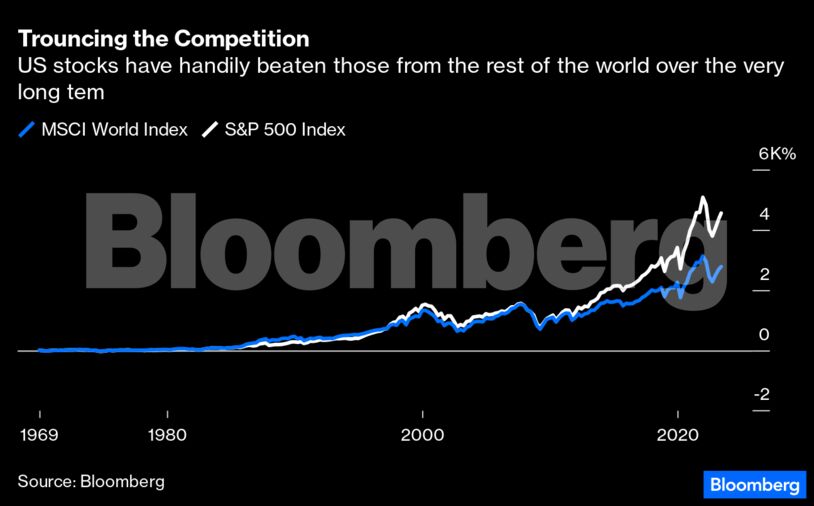

And yet, the raw numbers might suggest otherwise. The S&P 500 has returned an average of 8.7 percent annually since 1970, compared with 7.8 percent for the MSCI World Index that includes non-US stocks. Over time, that adds up to a big difference. Plus, the two benchmarks have almost the exact same volatility, suggesting no benefit from global diversification.

But the thing to know about returns is that they are extremely sensitive to the period you are analysing. Even 50 years of stock data may not tell you very much. And assuming the relatively recent past tells you everything you need to know about the future is a mistake. Sticking with just the S&P 500 requires believing the world changed in the last 15 years and that will be our new reality going forward. There are good reasons to be doubtful.

The outperformance of tech company shares may have been largely driven by historically low interest rates, and those days are probably over. Their shares have had a bit of a recovery in recent months despite higher rates, likely due to enthusiasm over the prospects for artificial intelligence, but at this early stage we can’t know the winners. AI may indeed change the world, but in ways that makes economic growth more democratic, producing tremendous opportunities for smaller companies and poorer countries, and perhaps leading international stocks to outperform.

Also, the US economy is no sure bet longer term. The major investment the government is making in industry and more reshoring may succeed and reduce corporate supply-chain risks, but it could also be distorting the distribution of capital and drag on the economy. The result is slow growth and higher debt. Investing abroad offers some diversification from any one government’s policy.

When structural changes happen in markets and economies, the old rules no longer apply. It may take decades to know when they started, but they do become clear over time. I tried to convince the financial planner that he should stick with his strategy because the future is as uncertain as ever, especially for long-term investors. The best you can do is stay grounded in theory based on decades of data. He was not sure his clients would have the patience to see if he was right.

Allison Schrager is a Bloomberg Opinion columnist covering economics. Views are personal and do not represent the stand of this publication.Credit: BloombergDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.