Gaurav Dua

After hiking interest rates twice in the latter part of 2018, accompanied by a hawkish monetary stance, the Reserve Bank of India (RBI) completely changed its tune in the last bi-monthly monetary policy review meet in February 2019. The central bank cut the policy rate by 25 basis points and changed its monetary stance from “calibrated tightening” to “neutral”. And rightly so, because monthly retail inflation has been undershooting RBI’s forecast and the tight liquidity conditions, post the IL&FS fiasco, have been hurting economic growth.

Macro indicators support further rate cuts

The trend in inflation remains soft. Consumer inflation could end up lower than RBI’s revised forecast of 2.8 percent for Q4 (Jan-March quarter). The outlook for retail inflation in fiscal 2019-2020 is also pretty benign on the back of distinct signs of weakness in consumption demand in both rural and urban regions.

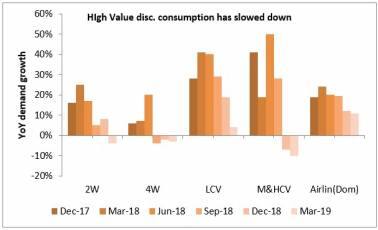

Among high frequency data-points, the monthly industrial production growth figures plummeted to 1.7 percent in January 2019 (from an already weak reading of 2.6 percent in December 2018). Auto sales are the weakest in the last five years and the growth in domestic air traffic has been trending downwards for the past five months. The recent appreciation of the rupee is also inflation negative and would mitigate the impact of a rise in crude oil prices or uptick in other global commodity prices.

Globally also, a dovish stance by the US Federal Reserve and early signs of a slowdown in global economic growth rates will encourage central banks to further cut policy rates.

It’s no longer if, but how deep, will be the cut this time around

The market is already factoring in a 25 basis points rate cut in the first bi-monthly monetary policy review meet on April 4. But the moot question is whether it would be accompanied by a change in monetary stance from “neutral” to “accommodative” and whether the undertone of the commentary will be dovish.

An extreme view from certain quarters of the market is that the central bank needs to nip the growing slowdown in the bud by announcing an aggressive 50 basis points rate cut. It would not be surprising if a couple of members of the monetary policy committee (MPC) do vote for a 50 basis points rate cut.

However, the 50 basis points rate cut looks unlikely to me. The RBI would prefer to wait for the new government in June and see its policy priorities before taking such a bold decision. Given the race to give cash doles to the weaker sections of society, any bold move could backfire and force RBI to do a volte face again post the elections. RBI can ill afford to take another U-turn after the recent complete change in its policy stance in the past few months.

Thus, what is likely is a 25 basis points rate cut with a dovish commentary and a promise to do much more if inflation remains benign and economic growth fears increase.

In such an environment it would be prudent to take home some gains in banking stocks before the monetary policy on April 4. Bank Nifty has surged by close to 12 percent in the past one month or so ahead of the monetary policy. Thus, it would be wise to book some trading profits and wait for better entry points.

Gaurav Dua is head of research, Sharekhan. Views are personal.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.