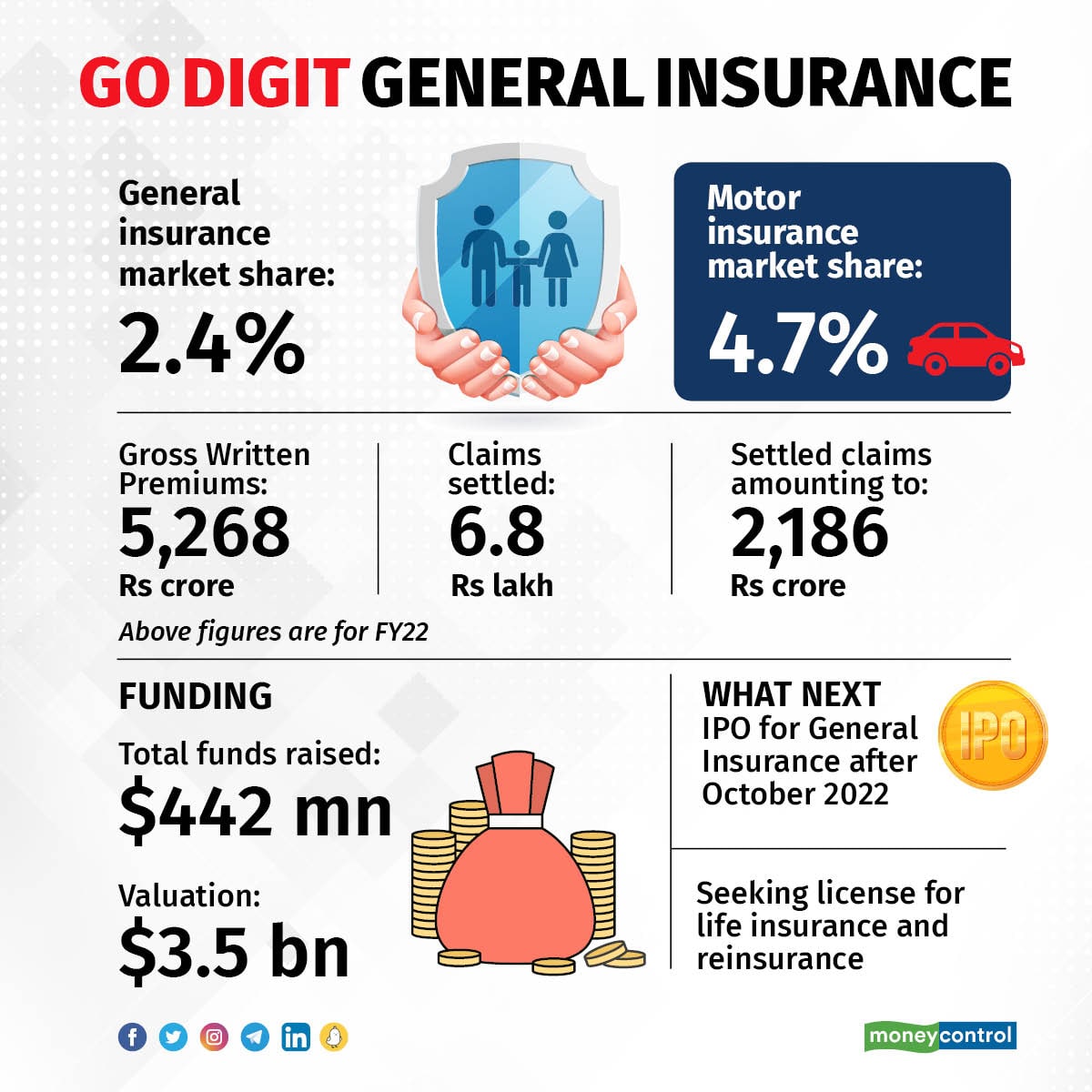

In FY22, Kamesh Goyal’s startup Go Digit General Insurance became the fastest general insurer to cross Rs 5,000 crore in annual gross written premiums. The next pit stop for the company, backed by Canadian billionaire investor Prem Watsa’s Fairfax Holdings, is to go public soon after the company completes five years in business this October. Per Insurance Regulatory and Development Authority of India (IRDAI) norms, promoters cannot sell a stake before five years.

However, the insurance industry veteran has larger plans to build an insurance conglomerate. Digit has applied to the IRDAI seeking licences to set up a life insurance and a reinsurance entity.

Valued at $3.5 billion, the company raised a total of $284 million in 2021. Besides Fairfax Holdings, the company counts Sequoia Capital India, A91 Partners, Faering Capital, TVS Capital and cricketer Virat Kohli as its investors.

In an interview with Moneycontrol, Goyal said that the company will assess the timing of its IPO at the end of the five-year tenure, based on market conditions. Meanwhile, he believes that the tough macro environment owing to rising interest rates and inflation will slow down the pace of growth for the general insurance industry.

Goyal worked in both life and general insurance before founding Digit in 2017 and has 32 years of experience in the space. Digit is an insurance manufacturer and provides motor, health, travel, fire and other small-ticket insurance. The company has an overall market share of 2.4 percent and a share of 4.7 percent in the motor insurance space.

If the life insurance licence is granted, Goyal is hoping to co-create products in collaboration with customers and distribution partners, after securing the regulator’s nod. Edited excerpts from the interview.

Can you share any internal targets that you have in place for the company to achieve before the IPO?A lot of work internally goes in whenever one is planning an IPO. So, the work has been on but there is no target as such because, in a regulatory mechanism, you cannot have any targets. Markets also have their own sense. We are trying to complete whatever formalities are required (for the IPO). The hope is to do that first, and then take the next steps. No point trying to prepare too much beforehand.

Many of the tech stocks that listed when the markets were good last year are not currently doing well. Digit, on the other hand, is profitable, per International Financial Reporting Standards (IFRS) accounting rules, but the markets do not look favourable currently. Will you still launch the IPO as soon as the company completes five years?I would say that let the five years be over first and then we will take the next steps. I would not want to unnecessarily anticipate how the market will be etc. We will see at that time what the market is, and talk to the bankers.

The way we see it, IRDAI is focused on increasing insurance penetration. They are asking the industry to take whatever steps are required from their side. Instead of getting worried about the number, we are seeing it in the spirit of the regulator seeking more penetration and how we can help the regulator achieve that vision.

We welcome this and will try and do our best to help. The vision of every insurance company is and should be that every Indian should have some sort of an insurance policy.

You had earlier said that you foresee an opportunity to grow your share in the general insurance market from 2.4 percent currently to 5 percent in the next 10 years. The regulator’s targets suggest a much higher growth in the next five years. Does that change your projection?The 5 percent number came from the view of doubling our market share. There was no science built into that. But, business and life is not like a straight line on a graph. To have some number in mind and assume you will achieve that… I don't think in reality it works like that. We would have to go year by year, quarter by quarter.

Inflation has increased and the current economic situation globally is a bit uncertain. All these factors also play a role in the growth of any industry and also our industry. Over the longer term, India's economic growth story as well as the general insurance growth rate still look good to us. Short-term, we could always have some hiccups, but that always happens. You don’t change your long-term thinking based on short-term good or difficult things.

What impact do you see from the changed macro environment on the general insurance space as well as on Digit?Inflation obviously has had an impact on the claims. When inflation goes up, the cost of claims goes up. Second is if the growth rate dips; in India, people are still optimistic that our growth rate might come down a bit but not substantially. In other markets people are talking about recession. So, that obviously also will have some impact.

Obviously for any industry, when your expenses go up, your growth rate can come down. However, in India, as of now, nobody's talking about a slightly lower growth rate, and nobody's really talking about a very low growth rate. Our inflation is a bit high, but compared to a lot of other countries it is not that high. We will have to see how long this lasts, what the impact is.

Do you have any projections on the impact the industry will see in the next few quarters?The industry saw good growth in the first quarter of FY23 due to a lower base last year. Growth will moderate a bit in the July to September quarter. I would expect this growth rate to be around 13-14 percent as compared to the 23 -24 percent growth we saw in Q1.

We will have to see how Q3 pans out with the festival season, based on the economic situation, interest rates etc at that point in time.

How is the electric vehicle insurance vertical growing? On health insurance, are you seeing a further change in consumer behaviour as Covid-19 fears have receded?We are continuously expanding our partnerships on EV insurance and we are also seeing the sale of vehicles going up. Customers are adapting to electric vehicles much faster than anticipated. The overall environment is good for the growth of electric vehicles and we continue to work with almost all the EV players.

On the health insurance front, retail growth slowed in Q1. Again, that may be the base effect, plus a lesser sense of urgency to buy because Covid-19 is not really as bad as it was last year. Group health insurance is seeing good growth. That could also be because policies have had a high claim ratio — the impact of the Delta wave was seen for policies maturing in Q1. We'll have to wait and see how the growth rate in group health will be, based on renewals in the second quarter.

But overall, in healthcare, we are definitely seeing inflation. Last year, the cost of the average claim size even for non-Covid insurance had gone up by 15-20 percent. We are not expecting inflation to go down in the case of health insurance. Overall, demand will ease a bit because people may not feel the same need to buy or renew health insurance.

Health insurance is a long-term product. Consumers should definitely do a bit of research, and compare products before they buy rather than just buy what is being pushed at them. Changing a health insurance product is very tricky. If you look at the US, Europe etc., people normally spend 45 minutes at least online researching health insurance before they buy. We need to really start taking this a lot more seriously.

You have applied to the IRDAI for life insurance and reinsurance licences. What is the plan for those verticals?Right now the focus is to get through the licensing process. Life insurance and reinsurance will function as separate companies. Once we are successful in securing the licences, we will have talks on further plans.

Both the new companies will have to raise funds separately, they will have their own management teams.

How are you preparing for life insurance considering there are large players already in the space?We are very conscious of the challenges any new company entering the space will face. But on the other hand, when you start a new company, you also have some advantages in terms of flexibility of how to build your operating model, your tech platform etc. We will take it as it comes. Prem (Watsa) keeps saying that we look at things more from a long-term perspective. In the long term, this will be good. We obviously know it will be very tough to build this so we are not undermining it. Obviously, it’s a very challenging market. There has been no new life insurance company in the last 10 years.

On the tech front, what opportunities do you see to change the way life insurance is made available to customers?In my personal experience, you have 10 initiatives, and some may fail on day one. Some may click. We will try and take the same philosophy and begin with 5-6 initiatives. Once we secure the licence and are closer to launch, we will start meeting distributors to understand opportunities and challenges and then develop a value proposition.

We believe that we have to talk to customers and distribution partners, and have to co-create products and processes. We definitely have our own ideas and we are building on them. But we will have to validate the ideas with our own team as well as from the market. It’s too early for us to form very firm ideas.

You recently launched the ‘pay-as-you-drive’ add-on feature for motor insurance. How has the response been?The initial feedback seems to be encouraging. We are seeing good traction from customers on this product. As things stabilise we'll see if we can come up with more versions to pay as you go. Our team had been working on it, so the launch had been a bit faster than what we expected.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.