For many long-term investors, years of disciplined Systematic Investment Planning (SIP) investing in equites have finally done their job. The house is bought, the children’s education is funded, or the retirement corpus has reached a comfortable milestone. On paper, the hardest part is over.

In reality, a more delicate phase is just beginning.

The shift from accumulation to withdrawal is where financial outcomes are quietly decided. This is the stage where portfolios stop being engines of growth and start becoming sources of income. A wrong move here, exiting too fast, ignoring taxes, or misjudging market risk, can erode years of compounding far quicker than most investors expect.

This transition is especially critical in the years leading up to retirement. Between the ages of 55 and 60 investors are no longer chasing returns alone. They are protecting future cash flows, managing volatility, and ensuring that money lasts as long as life does. The decisions made in this narrow window often determine whether retirement feels financially secure or unexpectedly fragile.

Smart retirement planning, therefore, is not about pulling out money at the finish line. It is about withdrawing with intent, sequencing risk carefully, and turning a hard-earned corpus into a reliable, tax-efficient income stream that can withstand both markets and time.

Don’t rush the exit

The first instinct for many investors is to redeem the entire corpus once a goal is met. That’s usually a mistake. “If an investor has been investing through SIPs over the last few years and the financial goal is now achieved or nearing completion, the withdrawal should be planned as carefully as the investment itself,” says Saurabh Agarwal, Chief Business Officer-New Business, Angel One.

The starting point should be to pause ongoing SIPs, not withdraw everything. Before doing anything else, investors should set aside a 6-12 months emergency fund in savings accounts or liquid funds to ensure liquidity and peace of mind.

Instead of lump-sum withdrawals, a Systematic Withdrawal Plan (SWP) works better. SWPs allow investors to withdraw a fixed amount at regular intervals, reducing market timing risk and spreading out capital gains tax.

For funds not needed immediately, a gradual shift from high-risk equity to more stable options such as short-term debt funds, government securities, or fixed deposits helps protect accumulated gains. Exit loads and capital gains tax must also be factored in before planning withdrawals.

The 55-to-60 transition: Shift from growth to protection

For investors aged around 55 who have accumulated a Rs 1 crore-Rs 5 crore corpus and plan to retire at 60, the strategy needs a clear shift in mindset. The goal here is no longer aggressive growth but capital preservation, predictable returns, and tax efficiency.

“The focus should gradually move from growth to capital preservation with steady returns,” Agarwal explains. A good rule of thumb is to park the next five years’ expenses in low-risk, highly liquid options such as short-term debt funds, fixed deposits, or government-backed schemes. This ensures that near-term needs are insulated from market volatility.

The remaining corpus can still be invested for growth, but in a more balanced manner. Typically, 30–40 percent exposure to equities is sufficient for inflation protection, with 40–50 percent in debt instruments, and the rest in liquid assets. This glide-path approach systematically reducing equity exposure as retirement approaches helps manage downside risk without sacrificing long-term purchasing power.

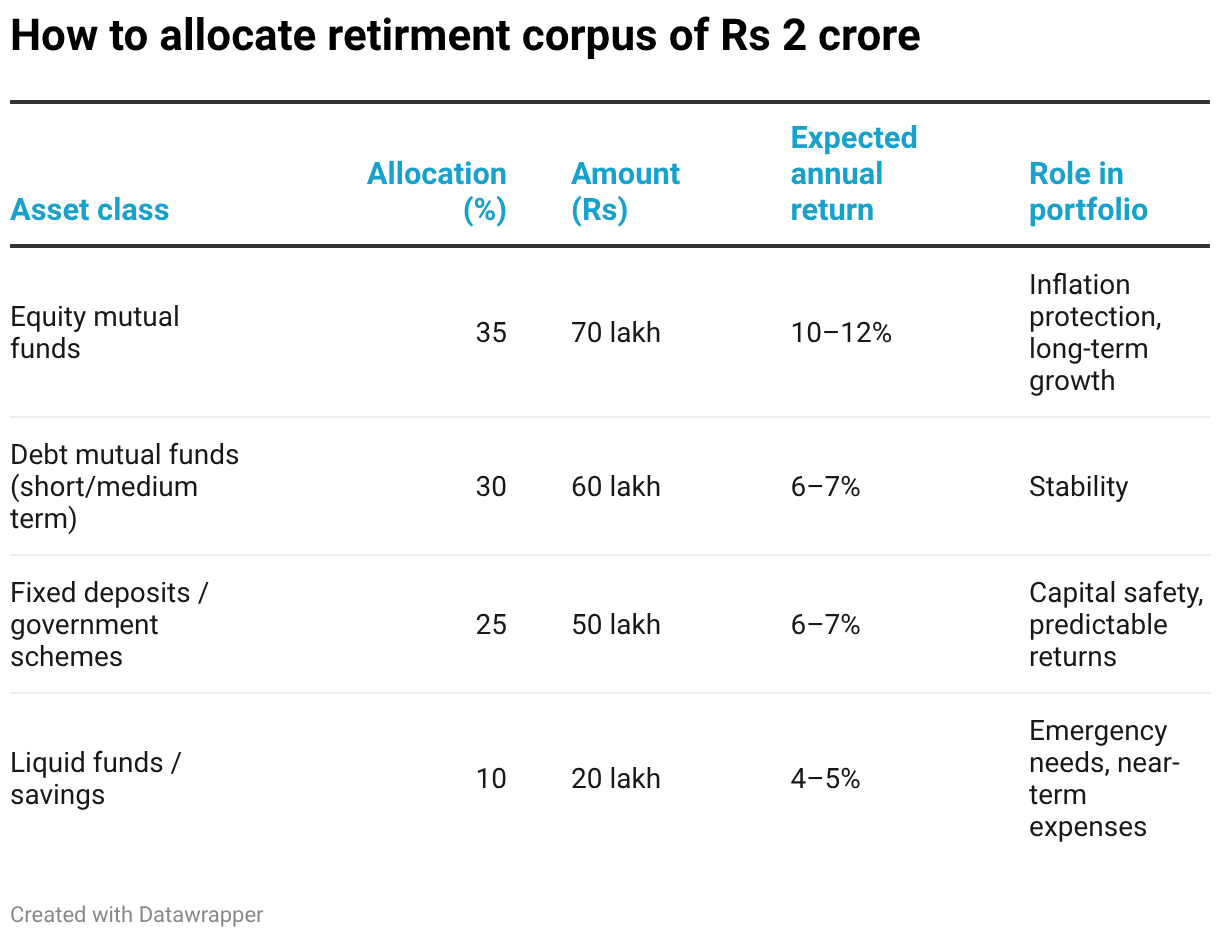

Where to deploy funds: A practical allocation framework

Below is an illustrative deployment strategy for an investor aged 55 with a Rs 2 crore corpus and retirement at 60. Actual allocation should vary based on risk appetite and cash flow needs.

This kind of structure allows the investor to meet short-term cash needs without touching equities during market downturns, while still letting a part of the portfolio grow.

A glide-path approach progressively moving from equities to safer instruments helps reduce market risk. Tax efficiency, predictable income through Systematic Withdrawal Plans (SWPs) in debt and equity funds, and regular portfolio reviews are key to ensuring a smooth transition into retirement, added Agarwal.

Tax efficiency matters more than returns

SWPs from equity funds held for more than a year attract long-term capital gains tax, which can be managed better when withdrawals are staggered. SWP from debt funds will be taxed at the slab rate.

Regular portfolio reviews at least once a year are essential to rebalance allocations, adjust for market movements, and align investments with evolving retirement needs.

Reaching a financial goal through SIPs is an achievement, but how you withdraw and redeploy money determines whether that success lasts. Whether you are exiting a goal or preparing for retirement at 60, a phased, tax-aware, and risk-adjusted strategy is critical.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.