Stroke cases among younger adults are rising sharply, with those aged 20-45 making up a growing share of the overall burden.

Multi-city data from Apollo Home Healthcare shows cases in this age group have increased 2.3 times between 2021 and 2025, with their share rising from 12 percent to 17.8 percent. In absolute terms, cases grew from 290 to 690, indicating faster growth than overall stroke incidence.

The increase is most visible in the 30-39 age group, while those aged 40-45 continue to account for the largest share. Even the 20-29 segment, though smaller, has more than tripled over the period.

Doctors say the trend is being driven by a mix of lifestyle and metabolic risk factors.

Dr Rajesh Reddy, Consultant Neurologist at Apollo Hospitals notes, “Younger patients are increasingly being diagnosed with conditions such as hypertension, diabetes, obesity and lipid disorders, along with lifestyle risks like sedentary habits, stress, irregular sleep and smoking.”

He further adds, “Delayed detection is a key concern, as many individuals ignore early warning signs and seek treatment only when symptoms become severe.”

Financial exposure remains high

The financial impact of stroke remains significant, particularly for younger patients.

The data shows that 74-79 percent of patients were financially under-protected at diagnosis. Nearly half had no insurance, while another 24-28 percent had coverage below Rs 5 lakh, which is often not enough to cover treatment costs.

This is important given that total treatment and rehabilitation costs range between Rs 5 lakh and Rs 12 lakh, with even insured patients facing a shortfall of Rs 2.5 lakh to Rs 5 lakh.

“What shocks families is not only the stroke, but the length of recovery and the continuing cost after discharge,” says Dr Darwin Ittiachan, Regional Lead Physician at Apollo Home Healthcare, adding that existing insurance often falls short of covering the full care journey.

Experts say the financial strain is higher because many patients are primary earners. The data shows 64 percent of young stroke patients are the main earning members, meaning recovery can directly impact household income.

Rehabilitation also plays a key role in both recovery time and costs. Hospital-based rehab is linked to 85-125 workdays lost, while structured home-based care can reduce this by 28-35 percent, helping patients return to work sooner.

Costs also differ significantly. Over a typical recovery period, home-based rehabilitation can reduce overall expenses by 40-55 percent compared to hospital-based care.

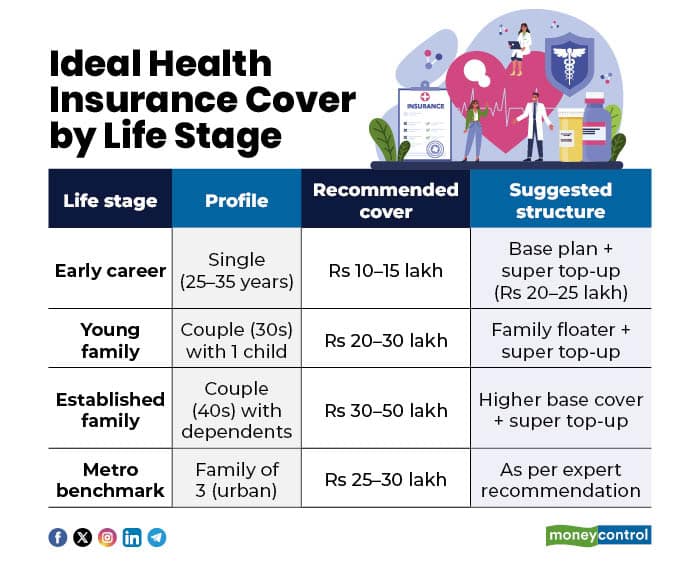

How much health insurance cover is enough?

The report highlights the gap in how younger individuals approach health insurance, especially for conditions that involve high costs and long recovery periods.

Experts say coverage should be based on age, location and family responsibilities, particularly as medical costs continue to rise.

Vivek Chaturvedi, CMO and Head of Direct Sales at Digit Insurance explains, “Medical inflation in India remains in the 12-14 percent range, driven by the growing use of advanced treatments and diagnostics. Given the rising cost of treatment, especially for critical illnesses, having an adequate sum insured is essential to ensure financial protection during medical emergencies.”

He further adds, “A sum insured of Rs 25-30 lakh for a family of three in metro cities is now recommended to provide a stronger financial safety net against major illnesses such as stroke.”

More broadly, here is how you should look at health insurance coverage:

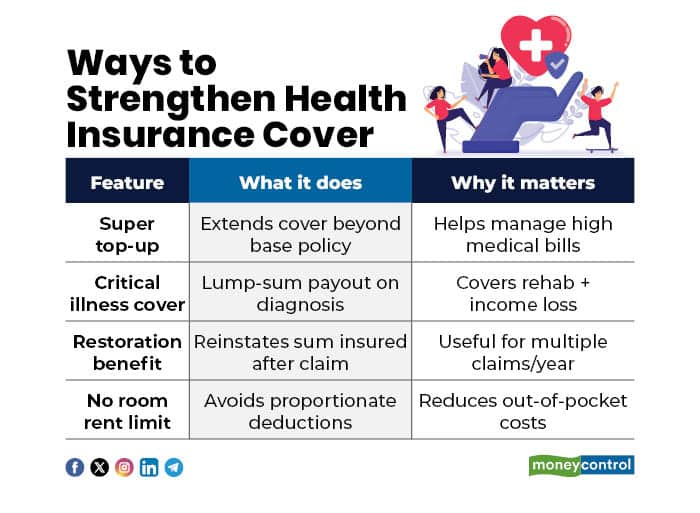

Having said that, experts point out that policy features matter as much as the sum insured. Plans without room-rent limits and with fewer restrictions on procedures can help reduce unexpected out-of-pocket costs.

Is higher cover needed in stroke cases?

Stroke-related expenses often go beyond hospitalisation, making higher coverage important.

In addition to hospital care, industry experts say patients may need long-term rehabilitation, physiotherapy and home healthcare, all of which can significantly increase total costs. This is why many insured patients still end up paying a large amount out of pocket.

Should you consider critical illness cover?

Now for high-cost conditions such as stroke, where costs can extend beyond hospitalisation, adding a critical illness cover may offer additional financial support.

“While a higher base cover should be the priority, individuals with lower existing coverage can consider adding critical illness protection to manage high-cost conditions like stroke,” explains Chaturvedi. These policies typically provide a lump-sum payout on diagnosis, which can help cover rehabilitation expenses or offset income loss during recovery.

Experts suggest that policyholders can also strengthen coverage through options such as super top-up plans, which extend coverage beyond the base limit, and restoration benefits, which reinstate the sum insured after a claim.

Chaturvedi adds, “Such features can be particularly useful in managing prolonged treatment or multiple claims within a policy year.”

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.