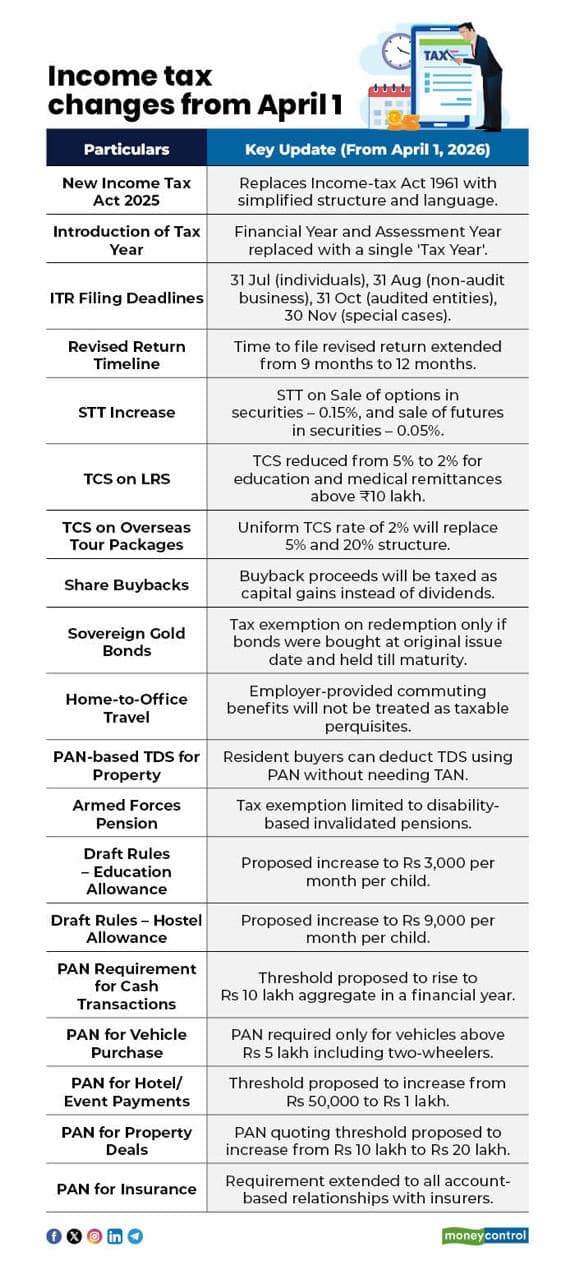

From April 1, the income-tax act, 2025 will replace the six-decade-old I-T act, 1961, several key changes in India’s direct tax framework will come into effect. The changes include lower tax collected at source (TCS) rates, an increase in securities transaction tax (STT) and an extended deadline for filing revised income tax returns.

“With effect from 1 April 2026, the Income-tax Act, 2025 will come into force, replacing the income-tax act, 1961. The new legislation introduces structural, conceptual and procedural changes across the direct tax framework,” said chartered accountant Suresh Surana.

Here is a list of the major changes that will come into effect from April 1:

The New Income Tax Act, 2025

Announced in the previous Budget, the Income Tax Act, 2025, will come into effect from April 1, the new financial year, and will apply from FY27 on. The new legislation will introduce simpler language and removes outdated provisions. The objective is to make the tax system easier to understand, improve compliance and reduce the scope for legal disputes.

Introduction of tax year

The terms "financial year" and "assessment year" will be replaced with a "tax year" to bring greater uniformity and make the tax framework easier to understand.

The existing slab rate framework for individuals under the old and new tax regimes continues without any changes.

Revision of due dates for filing the return of Income

The new law revises return filing deadlines to provide additional time to different categories of taxpayers.

• July 31: Individuals filing simple returns such as ITR-1 and ITR-2

• August 31: Taxpayers with business or professional income not requiring audit, and partners of such firms

• October 31: Companies, assessees whose accounts are required to be audited and partners of audited firms (including applicable spouses).

• November 30: Assessees to whom special provisions (eg section 172 cases) apply ie assessee, including partner of a firm or the spouse of such partner (where section 10 applies to such spouse).

These revised deadlines will be applicable from Tax Year 2026–27.

More time to file revised returns

The time limit for filing a revised return will be extended from nine months to 12 from the end of the tax year. A fee will be charged if the revised return is filed after nine months:

• Rs 1,000 if the taxpayer’s income is up to Rs 5 lakh

• Rs 5,000 if the income exceeds Rs 5 lakh

The extension aims to give taxpayers additional time to identify and correct errors in their income tax returns.

Increase in rates of STT

From April 1, STT rates on certain derivatives transactions will be increased to address the sharp rise in derivatives trading and growing concerns over speculative activity in the futures and options (F&O) segment.

The STT on the sale of options in securities will increase from 0.10 percent to 0.15 percent, while the tax on options that are exercised will rise from 0.125 percent to 0.15 percent. The STT on the sale of futures in securities will be raised from 0.02 percent to 0.05 percent.

Rationalisation of TCS rates

For remittances made under the Liberalised Remittance Scheme (LRS) exceeding Rs 10 lakh for education or medical treatment, the TCS rate will be reduced from 5 percent to 2 percent. However, remittances made for other purposes will continue to attract a TCS of 20 percent.

For overseas tour packages, the existing structure of 5 percent TCS on amounts up to Rs 10 lakh and 20 percent on amounts above this limit will be replaced with a uniform TCS rate of 2 percent.

Share buybacks to be taxed as capital gains

Previously, proceeds from buybacks were treated as deemed dividends and taxed at slab rates. From April 1, buyback proceeds will be taxed as capital gains.

In case of individual promoters buying back shares, the effective tax rate will be 30 percent and 22 percent when the promoters are companies.

Sovereign gold bonds

The tax exemption on the redemption of sovereign gold bonds (SGBs) will only apply to bonds purchased at the original issue price. Redemption of bonds bought in the secondary market will attract capital gains tax.

Motor accident compensation interest to be tax-free

From April 1, the interest component on compensation awarded by the Motor Accident Claims Tribunal (MACT) will be completely exempt from income tax. Claimants or their legal heirs receiving such interest will not be required to pay tax on it, and no tax will be deducted at source (TDS) on these payments.

Relief for home-to-office travel

The new Act provides relief for home-to-office commuting. Transport facilities provided by employers, or reimbursements for travel between an employee’s residence and workplace, will no longer be treated as taxable perquisites. The provision now extends to both company-provided vehicles and employer-paid commuting expenses, thereby broadening the scope of the earlier exemption.

PAN-based TDS deduction allowed from April 1

From April 1, the process for deducting TDS on property purchases from non-residents has been simplified. Resident buyers will be able to deduct and deposit TDS using a challan linked to their PAN, removing the requirement to obtain a Tax Deduction Account Number (TAN).

Tax exemption for armed forces pension limited to disability cases

From April 1, income tax exemption on pensions will apply only to armed forces personnel who are declared ‘invalidated’ from service due to a bodily disability. Pensions received on retirement due to superannuation will no longer qualify for this exemption.

Draft income tax rules

The Draft Income Tax Rules, 2026, if approved, will also come into effect from April 1. These proposed rules increase certain deduction limits under the old tax regime and introduce new forms in line with the Income Tax Act, 2025. Key proposals under the draft rules include:

• The education allowance deduction is proposed to be increased to Rs 3,000 per month per child.

• The hostel allowance deduction may be raised to Rs 9,000 per month per child.

• The threshold for mandatory PAN quoting in below financial transactions is also proposed to be increased:

Cash deposits/withdrawals: PAN requirement will increase from Rs 50,000 cash deposit in a day to Rs 10 lakh aggregate cash deposits or withdrawals in a financial year.

Motor vehicle purchase: PAN requirement will be limited to vehicles priced above Rs 5 lakh and will also include two-wheelers.

Hotel, restaurant or event payments: PAN quoting threshold will increase from Rs 50,000 to Rs 1 lakh.

Property transactions: PAN requirement threshold will increase from Rs 10 lakh to Rs 20 lakh.

Insurance policies: PAN requirement will expand from insurance premiums above Rs 50,000 to all account-based relationships with insurers.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.