India's credit card market has more than doubled over the past five years, crossing 111 million cards by mid-2025, with spending rising at around 25-30 percent annually, a recent report by Zeta, a banking technology company, has said.

Within this boom, co-branded credit cards such as the Flipkart Axis Bank and Flipkart SBI cards have carved a niche. According to the report, co-branded credit cards make up around 17 percent of all cards but contribute nearly 18 percent to overall spends, which is projected to grow to a quarter of the market by FY28. For frequent online shoppers, these cards are no longer a perk, they are a tool that can meaningfully impact savings.

But once you move beyond headline numbers, small differences in cashback caps, exclusions, and usage conditions begin to matter.

Joining fees and welcome benefits

At a base level, both cards come with a joining fee of Rs 500 and an annual fee of Rs 500, which is waived if annual spending crosses Rs 3.5 lakh.

However, there is a small but important distinction with the Flipkart Axis Bank Credit Card. Axis Bank periodically offers the card as first-year free, meaning the joining fee is waived upfront. In such cases, cardholders do not receive the Rs 250 Flipkart voucher that otherwise comes with paid cards. The Flipkart SBI Credit Card, on the other hand, issues the Rs 250 Flipkart gift card after the joining fee is realised.

Both cards also offer limited-time platform-specific welcome offers, but these tend to change frequently and shouldn’t be the deciding factor.

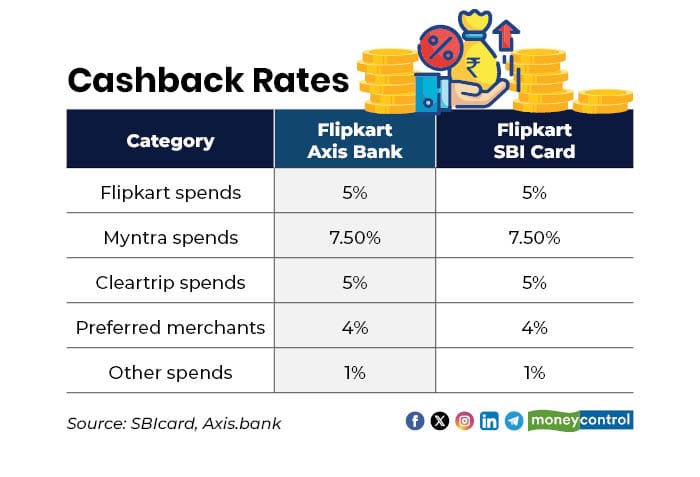

Core cashback structure

The main reason people sign up for either card is cashback, and this is where the overlap is the strongest.

Both cards offer identical overall cashback rates, 5 percent on Flipkart, 7.5 percent on Myntra, 5 percent on Cleartrip, 4 percent on select partner merchants, and 1 percent on all other eligible spends. In both cases, cashback is credited directly to the card account, not issued as points.

While the headline cashback rates look identical, the actual savings depend heavily on quarterly caps, eligible categories and how each bank applies exclusions such as EMIs and specific transaction types.

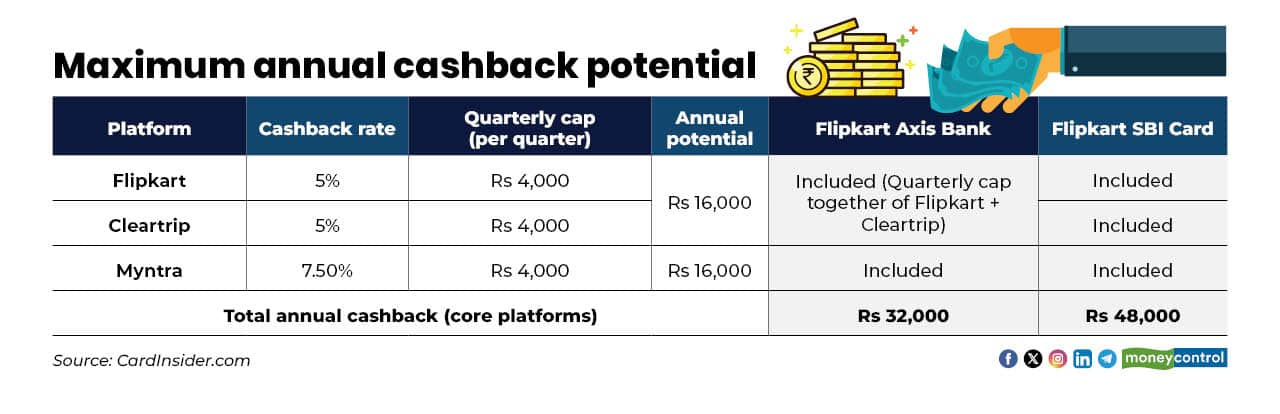

Cashback caps

For cardholders, this means the real value isn’t just about percentages, but about how quickly you hit these limits. Once the cap is reached in a quarter, every additional rupee spent earns no extra cashback in that category.

For the Flipkart Axis Bank Credit Card, cashback caps are structured as:

The preferred merchants for the Flipkart Axis Bank Credit Card include Cult.fit, PVR, Swiggy, and Uber, where cardholders earn 4 percent cashback on eligible transactions, with no upper limit on earnings.

For the Flipkart SBI Credit Card:

For the Flipkart SBI Credit Card, the preferred merchants are Netmeds, PVR, Zomato, and Uber. Cardholders earn 4 percent cashback on transactions at these merchants, again with no cap on the cashback earned.

These numbers represent the maximum possible cashback a user can earn in a year. To reach them, you must consistently hit the quarterly cashback cap on each platform, quarter after quarter, while avoiding EMI transactions on Flipkart, Myntra, or Cleartrip, which do not qualify for cashback.

As Ankur Mittal, co-founder of Card Insider, said, “The upside looks large on paper, but only disciplined users who consistently hit category caps will realise these numbers.”

Other charges and conditions worth knowing

Both cards offer a 1 percent fuel surcharge waiver, capped at Rs 400 per billing cycle, and neither earns cashback on fuel spends.

Axis Bank’s card has introduced several category-based fees in recent years, including on wallet loads, utilities, education payments and rent, once spending crosses defined thresholds. SBI Card excludes many of these categories from cashback altogether but does not apply as many transaction-level fees.

Neither card offers complimentary airport lounge access, reinforcing their positioning as pure e-commerce cashback cards, not lifestyle or travel cards.

Bottom line

Both Flipkart Axis Bank Credit Card and Flipkart SBI Credit Card deliver strong value for loyal Flipkart ecosystem users. The Axis card works well for shoppers focused on retail and lifestyle spends. The SBI card offers a higher upside for users who also spend heavily on travel via Cleartrip and avoid EMIs.

Approval standards are similar for first-time or lightly-leveraged users. However, Mittal said, “SBI Cards tend to be stricter when applicants already hold multiple credit cards, while Axis Bank is generally more accommodating in such cases.”

A better card isn’t decided by percentages alone, it’s decided by how closely your spending habits match the fine print.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.