Madhuchanda Dey

Moneycontrol Research

Tata Consultancy Services (TCS) started the new fiscal on a strong note, indicating a promising year ahead. With a recovery in the banking financial services & insurance (BFSI) segment in the North American markets, and TCS gaining market share with its early investments in digital, we see little risk to its premium valuation. The healthy payout (with buyback and dividends) coupled with a weak rupee are added tailwinds that should set a floor for the stock price. The stock has clocked 29 percent return in the past three months against a 4.6 percent rise in the Nifty. While there could be near-term consolidation in the stock performance, we expect mid-teens returns that should closely track the earnings trajectory.

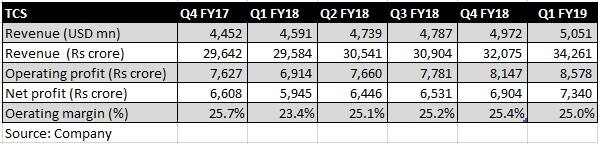

Result at a glance

For the quarter ended June 2018, TCS reported revenues of $5,051 million, up 1.6 percent quarter-on-quarter, with cross-currency impact trimming some of the gains. In constant currency term, revenue grew by 4.1 percent. Year-on-year, the revenue growth in constant currency terms was 9.3 percent.

Geographically, the bright spots for TCS were continental Europe, UK and Asia Pacific. It was heartening to see the biggest market North America with a share of over 50 percent showing a strong growth of 7 percent.

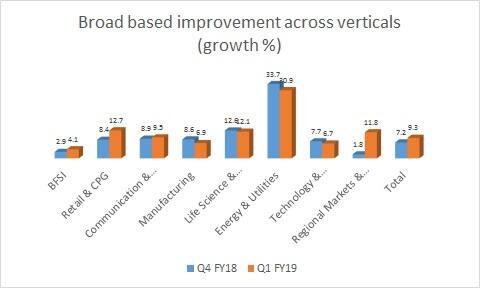

Vertical-wise, the biggest takeaway was the reversal of the underperformance in BFSI, riding on the revival of the North American markets. TCS has reclassified some of its verticals (like clubbed travel & hospitality with retail) and the now the two big verticals – BFSI and retail together contributing close to 47 percent of the revenue look out of the woods.

Life sciences, energy and regional markets maintained their strong growth trajectory.

Source: Company

Strong performance on margin

Despite a wage hike that is a recurring feature every first quarter, the sequential drop in operating margin was restricted to 40 basis points. While the wage hike took away 180 basis points from the margin in the quarter, this was partly compensated by efficiency gains contributing to 70 basis points and rupee depreciation adding 70 basis points as well. The company did not give any explicit guidance, but sounded confident of returning to the operating margin band of 26- 28 percent.

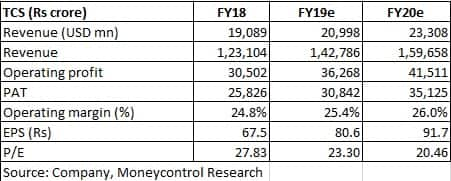

FY19 & beyond – look promising

The deal pipeline remains healthy. For the first time, the management has started announcing the quantum of deal wins. In Q1 FY19, TCS won deals worth $4.9 billion of which 55 percent came from North America. Amongst the leading verticals, BFSI contributed 33 percent and retail 16 percent. The book to bill ratio is little under one, in line with the past performance.

The management sounded extremely optimistic about FY19 and beyond. North American banking customers have started engaging strongly and there are nascent signs of tapering off of the captive units of these big banks. Companies from the BFSI space are engaging with TCS for their transformation programs. TCS sees a strong pipeline of transformational non-RFP (request for proposal) driven deals.

The management mentioned that while enterprise spending on technology is picking up, the company too has made a difference with its early investment in digital, thereby hinting at market share gains.

If the deal win and guidance is any indication, continuation/acceleration of this momentum does point to a promising FY19 after a strong FY18, despite a high base. The company is gearing up for the same, with step up in net employee addition despite attrition level remaining low.

Digital – the differentiator

The strong growth in digital revenue continues. In Q1 FY19, the digital business grew by 44.8 percent year on year and formed 25 percent of the total revenue. This growth in digital is much higher than the overall growth of the company at 9.3 percent.

In our interaction with competitors, we get a sense that deal sizes in digital are getting larger and that should boost margins. With rupee depreciation giving some headroom for margin expansion, TCS will continue to invest in new technology without compromising margin in the near term.

The healthy payout

TCS now adopts a well- defined capital return policy of 80-100 percent of free cash flow. In FY18, for instance, the company paid dividend of Rs 50 per share in addition to its Rs 16,000 crore buyback. Should it adopt a similar payout policy in FY19 as well (already announced a buyback worth Rs 16,000 crore), on a pre-tax basis this works out to a yield of 4 percent.

While the payout limits the downside, rupee depreciation in a volatile global environment could act as a tailwind. Investors should, therefore use dips to accumulate TCS as a core holding in the large cap IT space that could easily deliver mid-teens return in a choppy market.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!