has the maximum number of integrated townships - 42 projects with approximately 1.33 lakh units")

Highlights:- Cement volumes declined by 13 percent YoY - Power business also had a weak quarter - Higher realisations aided Q1 margins - Demand has softened in recent months - Valuations expensive at 23.4 times TTM EV/EBITDA

-------------------------------------------------First quarter financial results of Shree Cements were disappointing as the company struggled to meet the market's expectations. While the headline numbers appear decent, the operational performance was weak on key parameters.

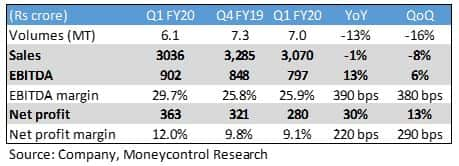

Key result highlightsTop line was marginally lower, but earnings before interest, tax, depreciation and amortisation (EBITDA) increased by 13 percent year-on-year (YoY) as margins expanded by close to 400 bps. Weakness in the overall demand environment had a significant impact on cement volumes, which contracted by 13 percent YoY to 6.1 million tonnes in Q1 FY20. However, this was offset by higher cement prices, which aided the margin performance.

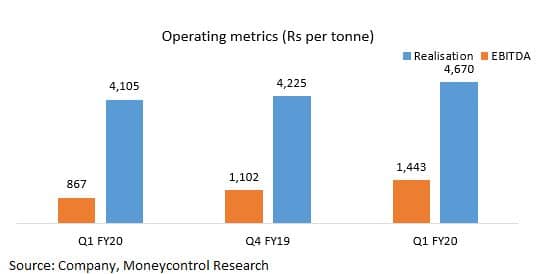

On a segmental basis, cement business revenues contracted by 1 percent YoY due to lower cement offtake. Realisations in this segment were much stronger in comparison to previous quarters and were up 11 percent quarter-on-quarter and 14 percent YoY. Overall cost base was stable as the decline in freight expenditure helped mitigate the higher staff expenses. A combination of higher realisation and steady costs had a positive impact on EBITDA per tonne, which came in at Rs 1,443 for the quarter.

Power business performance was also disappointing as volumes and sales contracted 14 percent and 6 percent, respectively. Weak demand and higher input costs had an adverse impact on the margin and EBITDA per unit fell sharply to 0.72, which represents a decline of 25 percent in comparison to the corresponding quarter last year.

Shree Cement has been diversifying its geographic footprint by expanding capacities in newer regions. Last fiscal year, the company set up a 3-million tonne clinker plant in Karnataka to expand into southern markets. In Q1, the company has commenced commercial production at its Jharkhand-based grinding unit (2.5 million tonnes). Besides, the company is in the process of setting up new plants in Maharashtra and Odisha.

On the international front, Union Cement, the UAE-based subsidiary which the company acquired in January 2018, is facing a challenging operating environment due to muted demand conditions in the region. Shree Cement has, therefore, increased focus on the exports to mitigate the near-term weakness in the local market.

The capex for FY20 is pegged at Rs 1,500-1,600 crore and will primarily be invested for funding the capacity expansion. The new plants are anticipated to go on stream in the next 18-24 months.

Outlook and recommendationLarge scale infrastructure projects have been driving the higher cement offtake across regions in the past 12-18 months. However, Q1 volume growth of cement companies suggests a stagnation in demand due to lower government spending. We anticipate the weakness to persist for the next 1-2 quarters as the country is witnessing a demand slowdown across multiple sectors.

Shree cement (CMP: Rs 19,710, Market Cap: Rs 68,667 crore) trades at a premium to its peers owing to its strong balance sheet and strict cost focus. The company has a strong positioning in north and western markets and is looking to scale up its market presence on a pan-India basis. Going forward, Shree Cement will have a greater focus on realisations in comparison to volumes. However, the execution will be challenging as competitive intensity remains high and the weak demand scenario is putting downward pressures on the prices across all regions.

In terms of valuations, the company trades at fairly expensive multiple of 23.4 times trailing 12 months Enterprise Value/EBITDA. We advise investors to tread carefully as the rich valuations might be difficult to sustain in a weak demand environment.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.