Highlights- Volume growth tops 10 percent across segments - Gross margin under pressure on higher input costs - Advertising spend higher 38 percent YoY - Deterioration in working capital a concern - Valuations reasonable from a long-term perspective

-------------------------------------------------Liquor manufacturer Radico Khaitan is in high spirits. And it lived up to its tag of being an outperformer during the December quarter of 2019-20, too.

A wider distribution network and new product launches did the trick. The volume play was quite impressive against the backdrop of muted industry sentiment. Gross margin lost fizz, but the underlying operational performance spoke for itself despite an inflationary cost environment.

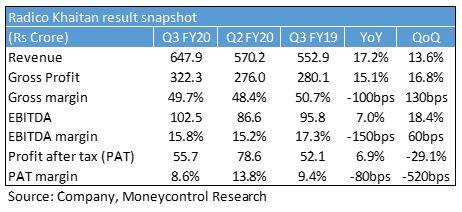

Earnings highlightsA strong offtake across both premium (Prestige and above) and non-premium (regular and others) segments drove up Radico’s revenue by 17 percent year-on-year (YoY). The IMFL (Indian-made foreign liquor) volumes for the said quarter came in at 6.5 million cases, up 14 percent. Premium segment volumes went up 21 percent and that of the popular segment 11 percent.

Gross margin felt the pinch because of pricey raw material (extra neutral alcohol up 22 percent YoY). Introduction of cow cess in Uttar Pradesh and credit loss provisions kept expenses at elevated levels.

Earnings before interest, tax, depreciation and amortization (EBITDA) covered some ground, rising 7 percent to Rs 103 crore. During October-December, the company made a payment of Rs 7.5-8 crore towards settlement of excise duty disputes under the Sabka Vishwas 2019 scheme.

New product launches played their part. That is visible from Radico’s operational performance, which got a fillip from 8PM Premium Black whisky and 1965 and Spirit of Victory rum. During 2019-20, the company launched these brands in three new states, taking the total tally to 14 states. Its strategy of premiumisation seems to be working well as the contribution of Prestige and above has inched up to 29.4 percent, from the earlier 27.7 percent.

According to the management, margins are expected to consolidate at the current levels as input prices seem to have peaked. India’s sugarcane output for 2019-20 has also declined sharply, but the country is likely to see a record food grain production this year owing to heavy rains during the previous monsoon season. Molasses prices could take some correction after the harvest of Rabi crop in April-May 2020.

Amid all this, slips are showing. Radico’s interest expenses are up again sequentially due to a slight deterioration in working capital. Cash flow from operations has been weak throughout first nine months of FY20 as liquidity challenges in the trade channel are leading to a longer receivable cycle.

The impact is there to see. Net debt widened to Rs 360 crore in December 2019, from Rs 315 crore in March. Delay in payments from state corporations, mainly Andhra Pradesh and Telangana, and the Canteen Stores Department has squeezed the cash flow. The overdue amount from these is fully secured and the total quantum of the same is pegged at around Rs 150 crore. Of this, the management expects to recover Rs 100 crore by the end of FY20. Given the current market environment, the company now expects to be debt-free by FY22-end as against FY21 earlier.

Outlook and RecommendationAll said, demand prospects for the liquor industry look very promising. This is borne out by the fact that alcohol consumption has been on the rise every year, regardless of the business cycle. However, near-term challenges such as slowdown in consumption and increase in taxes (introduction of the cow cess) loom.

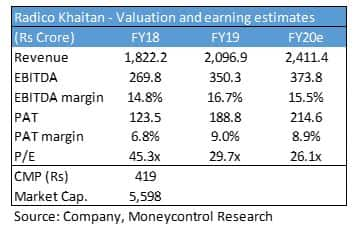

Radico Khaitan has been outperforming the industry in recent years. Its volume numbers suggest that the company has been capturing incremental market share against its larger competitors (United Spirits and Pernod Ricard). For FY20, the company is on track to deliver volume growth of 9-10 percent with margins of 15-16 percent.

The stock has seen a sharp upmove post its quarterly earnings and trades at 26 times FY20 estimated earnings. The long-term prospects look good and investors should gradually build positions in the scrip. The point to note is deleveraging and portfolio premiumisation remain key triggers for Radico Khaitan’s growth and its stock re-rating.

Follow @Sach_PalFor more research articles, visit our Moneycontrol Research pageDisclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!