Madhuchanda Dey

Moneycontrol Research

Highlights:

- Strong growth in loan book

- Diversified asset book and liabilities

- Asset quality on the mend

- Auto slowdown and poor monsoon key risks

- Valuations reasonable

-------------------------------------------------

Mahindra & Mahindra Financial Services (M&M Fin) has seen its operating environment improve in the current fiscal. However, the automobile end-market, which forms a large chunk of its lending book, is on a slow lane. Against this backdrop, how should investors be positioned in this stock?

M&M Fin (CMP: Rs 419, market capitalisation: Rs 25,900 crore) is a subsidiary (51.9 percent) of Mahindra & Mahindra (M&M) and engaged in the business of financing purchase of new and pre-owned auto and utility vehicles, tractors, cars, commercial vehicles, construction equipment and SME financing. The company has 1,313 offices covering 27 states and five Union territories in India with over 5.91 million vehicle finance customer contracts.

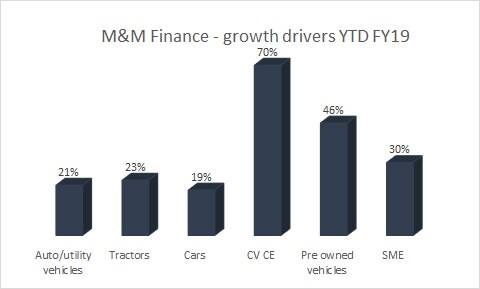

Strong growth in assets

Business momentum remains strong, with assets under management growing by over 30 percent as at December 31, 2018, driven principally by commercial vehicles, pre-owned vehicles as well as lending to small & medium enterprises (SME). Growth in disbursement was in excess of 24 percent. Albeit the slowdown seen in the vehicle side of the business, the company remains confident of maintaining over 20 percent growth in assets. The management isn’t too worried about its growth outlook and feels 20 percent asset growth is achievable as most of the products financed are not aspirational but are driven by necessities.

Source: Company

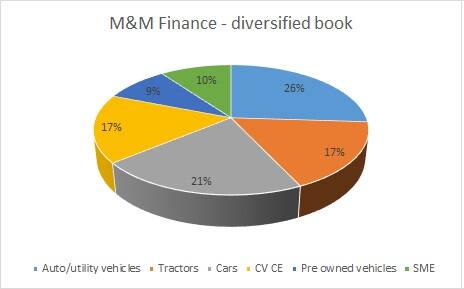

Asset book – diversification leads to de-risking

The lending book remains diversified, thereby de-risking the business. The company remains deeply penetrated in the geographies they operate.

Source: Company

That essentially means that the slow growth in one product category can be compensated by other products to a large extent. For instance, while the first-hand automobile market is on a slow lane, the company is witnessing traction in the second-hand vehicle financing as well as construction equipment segments. The management feels that the competitive intensity is not very severe and the company is experiencing improvement in market share in almost every product segment.

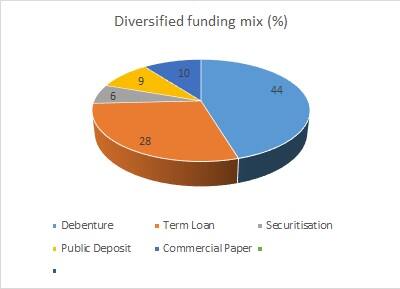

Emerging stronger from the recent liquidity crisis

M&M Fin was unscathed in the recent liquidity crisis, although it experienced a short-term increase in its cost of funds. For instance, Q3 FY19 saw the lingering impact of the Infrastructure Leasing & Financial Services (IL&FS) crisis and tightness in liquidity.

However, the management mentioned that there was no funding constraint for M&M Fin, although they carried some excess liquidity as a precaution. End-market still looks good with no pressure on lending yields. Despite the challenges, the company was able to maintain its interest margin. The company has a diversified funding mix with over 40 percent of funding accruing from a stable source like bank funding.

Source: Company

Asset quality – decisively on the mend

Improvement in asset quality continues with the quarter witnessing a 10 percent sequential decline in gross non-performing assets (NPAs). Gross and net NPAs at the end of the quarter stood at 7.7 percent and 5.8 percent, respectively. The management mentioned that although the headline gross NPA number may still look a tad elevated the underlying trend is strong.

On a 180-day past due basis, the underlying asset quality is at one of the best levels. The number of contracts under NPA is also on a decline. While the underlying asset quality has improved, provision cover (provision held against non-performing assets) has actually declined to 26.9 percent in Q3 FY19 from 34.9 percent YoY. The management, however, maintained that overall loss is close to its current coverage levels.

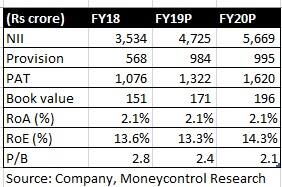

Eyeing three percent RoA

On the back of improvement in net interest margin (NIM) as well as productivity and decline in provisions, the company is hopeful of reaching three percent return on assets (RoA) in the next couple of years from the current 2.2 percent level.

Subsidiary performance improving

Some of the company's important subsidiaries are showing an improvement. Mahindra Rural Housing (88.75 percent stake) reported a 32 percent growth in after-tax-profit for the first nine months of FY19 with a gradual improvement in asset quality. Mahindra Insurance Brokers (80 percent stake) reported a 46 percent growth in after-tax-profit for 9M FY19.

Investment risks

After a blistering pace of growth in the past, auto industry volumes appear to be on the slow lane, which could impact demand from its end customers. However, management still sees no signs of stress, with cash flow of its rural customers improving on the back of increase in infrastructure activities. For transporters, the change in axle load norms has resulted in better cash flow.

Erratic monsoon or any other event that negatively impacts income/cash flow in rural areas could impact asset growth as well as delinquency levels.

Outlook

With its deep rural penetration, M&M Fin has carved a niche for itself. The diversification in asset as well as funding book makes the business relatively de-risked and the marquee parentage insulates it from the funding issues that has engulfed the NBFC space in recent times. We see the company as a vantage player to wean away market share from weaker competition. The decline in credit cost could be a earnings trigger going forward.

The stock has corrected by close to 11 percent in the past three months. With most issues largely addressed, the weakness may be a perfect time to accumulate the stock for the long term.

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!