Neha Dave

Moneycontrol Research

The insurance sector in India is on a structural growth path. Listed private insurers have gained a significant edge over agency-led insurers and are now witnessing accelerated growth.

We are enthused by private insurers’ improving profitability metrics in general, and their changing business mix in particular. We see low insurance penetration, increasing persistency ratios and growth of the protection business as key drivers of profitable growth for insurance companies.

Given the promising outlook on the sector, which life insurance company’s stock is a worth investing in at this point? We have analysed the H1FY19 earnings of ICICI Prudential Life Insurance and HDFC Standard Life Insurance, two of India's leading private insures.

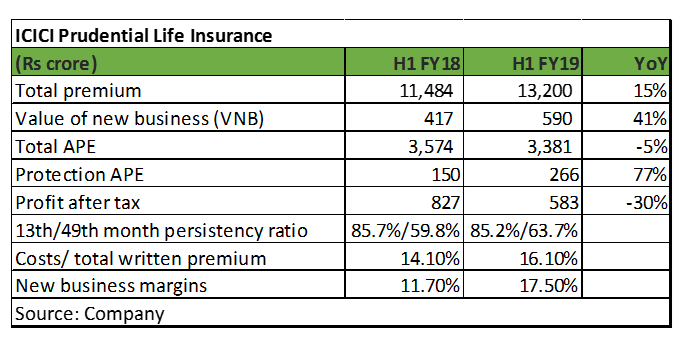

ICICI Prudential Life: Headline numbers muted but insurer on right track

ICICI Prudential's H1FY19 performance is an optical illusion. The insurer's accounting profits declined 30 percent on year, dragged down by increasing operating expenses and lower investment income. However, its operating performance was very healthy.

Insurance companies recognize costs incurred (marketing expenses including commissions) to acquire new business upfront. This is because accounting rules do not allow amortisation of cost over the life of the policy. ICICI Prudential increased its marketing spend to grow the protection business, which led to a drag on reported profit (referred to as new business strain).

There were two negative readings from the company's first half performance -- a decline in annualised premium equivalent (APE, measure of ascertaining business sales in the life insurance industry), and an increase in operating expenses. But neither of these negatives worry us much, as the finer details we have highlighted are quite encouraging.

However, the highlight of the company's H1FY19 performance was the strong growth of its protection APE, which grew 77 percent on year. This actually got masked by its headline growth number.

It is heartening to see the business mix improving in favor of the high margin protection business. The share of ULIPs in total new business APE stood at 82.2 percent, while that of the protection business improved further to 7.9 percent (4.5 percent in Q1FY18).

As a result, the company's cost-to-total-written-premium ratio deteriorated to 16.10 percent from 14.10 percent last year.

However, despite the rising cost, new business margin expanded significantly to 17.5 percent from 11.7 percent a year ago. Apart from an improvement in persistency ratio, it was the product mix with an increasing share of the protection business that drove margin expansion.

The insurer has increased spending on adverting and incentives to grow its protection business. It does seem like the right strategy as the benefits exceed the costs, as is evident in the significant improvement in margins.

Overall, ICICI Prudential's results reflects its 4P strategy for future growth. We are enthused by the good growth on 2Ps (protection and persistency) in H1FY19, which we believe will lead to an improvement in the other 2Ps (premium growth and productivity) in the long term.

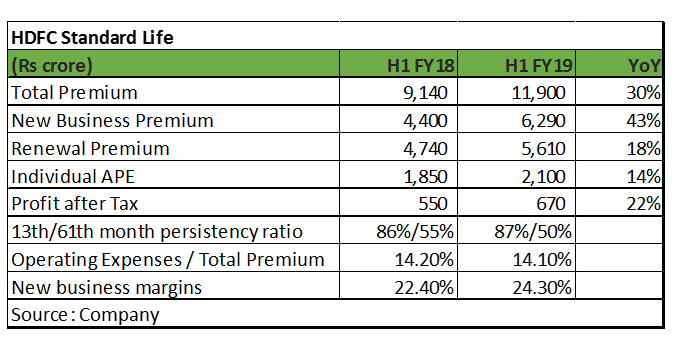

HDFC Standard Life H1: Steady performance

HDFC Standard Life continued to deliver a steady performance. Its profit rose 22 percent on year, driven by growth in premiums and an expansion of margins.

The company's total premium increased 30 percent year on year. Its continuous focus on the relatively-high-margin protection business was clearly visible as the share of protection in new business premium improved to 28.7 percent in H1 from 26.4 percent last year.

Operating performance continued to be superior, with operating-expenses-to-total-premium-and-persistency ratio at the shorter end (13th month) almost stable on a year-on-year basis.

Thanks to the product mix and superior operating performance, new business margin expanded to 24.3 percent, significantly higher than 22.4 percent reported a year ago.

Overall, HDFC Life's return ratios were strong and steady, with operating RoEV (return on embedded value) at 19.6 percent and RoE (return on equity) at 26.4 percent in H1FY19.

Both insurers witnessed strong growth in protection business

Buoyant capital markets have helped insurance companies improve their profitability as the sector witnessed growth for products like ULIPs and an improvement in persistency. Going forward, we see a large share of growth emanating from the protection business as there is a huge opportunity in this segment.

India continues to be a high protection-deficit country. As per Swiss Re estimates, for every $100 needed for protection, only $8 is spent by a typical Indian household, leaving a massive mortality protection gap.

Prefer ICICI over HDFC on valuation front

We like HDFC Life for its balanced product mix with leading position in the protection business, an expanding distribution network, high focus on technology, product innovation and an experienced management. Having said that, the premium valuation of the stock gives us cold feet.

Despite the recent correction, HDFC Life's stock is trading at 4.4 times its trailing P/EV (price to embedded value), which is a significant premium to its peers. Given its best-in-class return ratios and profitability levers, the premium valuation will be sustained. While the stock is a long-term compounder, the stretched valuations limits its near-term upside.

At the other extreme, ICICI Prudential's stock is currently trading at 2.4 times its trailing P/EV, which is at a significant discount to HDFC Life’s, despite RoEV improving from 16.5 percent in FY17 to 22.7 percent in FY18. We view the valuation discount of more than 40 percent to its closest peer as unwarranted and expect the gap to narrow in the near-to-medium term.

While the current volatility in markets might make investors jittery about ICICI Prudential because of its higher exposure to ULIPs, there are no signs of an adverse impact on its financials so far. Further, it is worth noting that while the protection business is very lucrative, a large part of it comes from the credit protection business, which is vulnerable to stringent regulatory actions. This makes ICICI Prudential a relatively safer bet as contribution from the high-margin protection business, though growing, is still in single digits.

Overall, we are positive on the insurance sector and suggest investors to participate in the insurance growth story through ICICI Prudential, which is available at a compelling price. While investing in HDFC Life can offer downside protection, investors will be better off with ICICI Life as it offers a reasonable upside potential as well.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.