Building material solutions provider Hyderabad Industries Limited (HIL), reported a strong performance for the second quarter of the current fiscal year.

The company's topline growth was driven by a combination of realisation and volume growth across multiple product lines. Operational performance improved significantly on the back of internal cost savings as well as efficient working capital management.

Hyderabad Industries has benefitted from the introduction of Goods and Services Tax (GST) and the management expects the growth momentum to continue as the company enjoys a strong relationship with its dealers and is consistently expanding its product portfolio to cater to the growing demand of the building materials industry.

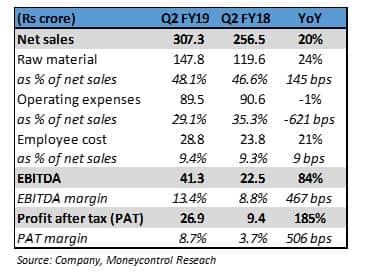

Quarterly result snapshotThe company's revenue for the quarter increased 20 percent year on year (YoY) to Rs 307 crore. Its operating profit increased from Rs 23 crores in Q2 FY18 to Rs 41 crore in Q2 FY19, representing a growth of 84 percent.

Its operating margin expanded to 13.4 percent as the company benefitted from price hikes, lower inventory as well as a reduction in operating and manufacturing expenses.

Profit after tax (PAT) nearly tripled to Rs 27 crore on account of higher other income (Rs 16 crores in Q2 FY19 vs Rs 9 crore in Q2 FY18). Interest expenses for the quarter came in at Rs 4 crore as the company had taken on additional debt to fund its recent acquisition.

Building solutions segment leading growthHyderabad Industries' sales in the quarter gone by were weaker than in Q1 because of the monsoon season. In the roofing solutions segment, sales growth of 4 percent on year was aided by 6 percent rise in volumes in asbestos cement sheets.

The building solutions segment recorded a jump in sales of 30 percent on year to Rs 159 crore. A significant rise in dry mix volumes (up 76 percent on year) drove the topline. Board and panel volumes also increased by over 11 percent and 22 percent, respectively, during the quarter.

New products gaining tractionSales of roofing sheets, the biggest source of revenue and profit for Hyderabad Industries, have stagnated in recent years. To cater to the growing demand in infrastructure and construction, the company is gradually expanding capacities across product lines and diversifying its revenue stream by launching new products.

The company recently launched Charminar Fortune (asbestos-free roofing product) to cater to the requirements of institutional customers. The feedback received from the initial trial runs has been good and it expects the product to gain traction over the next 6-12 months.

Parador Holdings acquisition completeHyderabad Industries' acquisition of Germany-based Parador Holdings is now complete and the business integration is underway. Parador designs, manufactures and distributes flooring solutions for customers across 65 countries. The company has 2 manufacturing facilities located in Germany and Austria.

In terms of financials, Parador reported sales of around 142.2 million euros in 2017 and generated an operating profit of 10.7 million euros. The management expects the acquisition to be EPS accretive but margin dilutive as Parador's margin is lower than Hyderabad Industries' standalone margin.

The company has funded the acquisition through a combination of rupee and euro-denominated debt. As a result, the debt-equity on a standalone level rose to 0.5 times at the end of H1 FY19 ( vs 0.1 times at the end of FY18). This is expected to move up to 1.0 times on a consolidated level at the end of FY19.

Outlook and RecommendationOn the demand front, we expect Hyderabad Industries to benefit from a reduction in GST rates (from 28 percent to 18 percent) and improving rural demand. For the company, the scale up in revenue will largely come from new product lines (plumbing, pipes, putty).

The recent acquisition of Parador will further expand its product and geographic footprint and position it as an integrated building solutions provider. On the cost front, the operating margin will continue to gain from operational efficiencies as well as economies of scale.

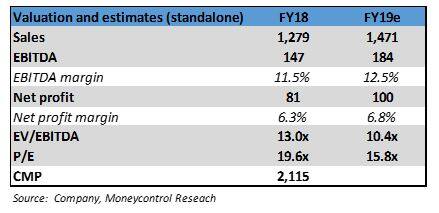

From a valuation standpoint, the stock trades at nearly 16 times the company's FY19 price-earnings on a standalone basis. Consolidation of Parador’s financials into the parent entity would further aid the bottomline.

Hyderabad Industries is a market leader in the building materials industry and the current stock valuations appear fairly reasonable for accumulation from a long-term perspective.

Follow @Sach_PalFor more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.