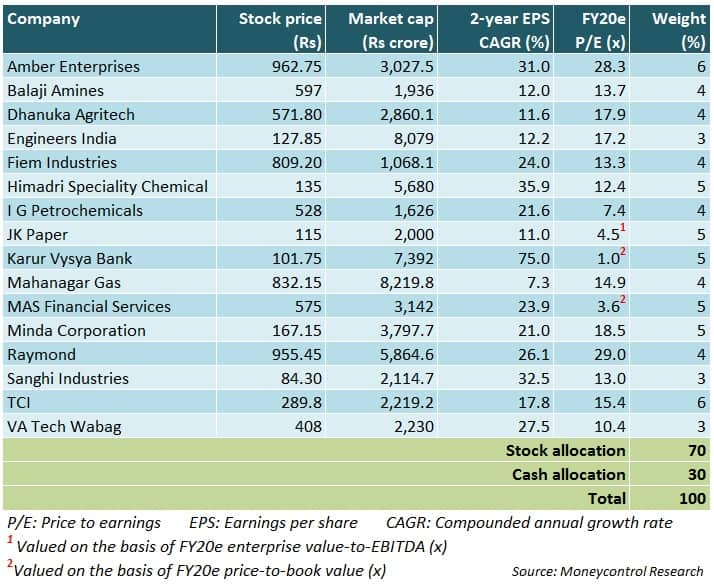

This year’s correction in the erstwhile market darling, mid-caps, has been severe. While the headline Nifty Index has risen by 2%, the mid-cap index has fallen by close to 11.5%. Within the mid-cap universe, the correction in several pockets have been significant. Earnings disappointments only partially explain the decline; sentiment, too, has been subdued. After a careful analysis of the financial numbers and the earnings outlook, we have constructed a 16-stock mid-cap portfolio (with 30% cash to take care of future volatility) to capitalise on the current weakness, which we feel presents a good opportunity for long-term investors.

Amber Enterprises is an OEM (original equipment manufacturer) and ODM (original design manufacturer) for room air conditioners (RACs) and components, an underpenetrated category in the consumer space. The capability to cater to marquee Indian RAC (room air conditioner) companies, with a market leadership position and 80 percent of revenues coming from margin-accretive ODM processes, should benefit the company.

Leading amine manufacturer, Balaji Amines, which continues to achieve double-digit volume growth, looks interesting. In the medium term, the company benefits from multiple capacity expansion initiatives and higher capacity utilisation for products wherein imports face anti-dumping duty. We like the management’s strategy of focusing on high-margin products where the domestic market is dependent on imports.

Dhanuka Agritech looks attractive after a 34-percent correction from its 52-week high, given that the company’s growth story remains intact. We see earnings tailwinds from a healthy product mix with more than 50 percent sales from specialty molecules, a strong lineup of new products, low penetration of herbicides and fungicides in India, favourable rural-focused policies and a good monsoon. However, in the short-term, pressure on the raw material front might continue.

Strong capex in the domestic hydrocarbon sector would benefit Engineers India, which is expected to deliver 12% annual earnings growth over next years backed by strong order book of close to Rs 7,800 crore or about four times its annual sales. After a 40% correction, its stock is attractively valued at 17 times earnings offering a 3% dividend yield.

FIEM Industries (FIEM) is a lighting solutions provider to automobiles, catering to two-wheeler (2W) segment. With its market leadership, strong clientele, focus on developing in-house technologically advanced products, and adoption of LED-based products, the company should witness decent earnings traction despite a drag from the LED Luminaries business. The business should remain unaffected by EV disruption, and trades at reasonable valuation.

Himadri Speciality Chemicals continues to benefit from elevated realisations for carbon black and coal tar pitch. The company has guided to strong volume growth across product lines in the next three years, particularly in high-margin specialty carbon black and the carbon material for the lithium-ion battery. Given the high visibility in earnings the current consolidation in stock price presents an opportunity.

IG Petrochemicals, a leader in the phthalic anhydride market has been generating strong return ratios. The company is expected to deliver 22% annual earnings growth over next two years. After a steep correction of close to 40%, the stock is attractively valued at 8 times FY20 estimated earnings.

JK Paper is well positioned in high-quality paper segments with cost leadership and integrated production capacities and is also looking to expand through the organic as well as inorganic route. Favorable industry factors such as improved supply -demand dynamics and raw material availability in proximity will continue to aid profitability.

Karur Vysya Bank’s results have been weighed down by higher slippages and consequently higher provisions. However, the directional roadmap appears to be encouraging in terms of its strategy of diversification and de-risking of the lending book, garnering more low cost deposits, stepping up fee income and a greater adoption of technology under the new CEO (an ex- Citi banker).

After the recent correction, Mahanagar Gas Ltd (MGL) looks attractive given the clean balance sheet and revenue growth visibility. The company has recently taken a price hike which should protect margins. Gas as a cleaner fuel should see volume traction as the city gas distribution network expands. Higher crude prices also make gas a good alternative.

Mas Financial, a Gujarat –based NBFC that got listed last year, has been a slow but steady player. The company has carved out a niche in lending to micro and small enterprises in its focused geographies, understands its end market well and has a unique sourcing strategy (partnering with several NBFCs) and conscious about maintaining its profitability parameters.

Minda Corp (Minda) is a well-diversified auto-component manufacturer catering to passenger vehicles, three-wheelers, two-wheelers and commercial vehicle segments. The reported numbers have been strong. With marquee clients in its kitty, no client concentration, focus on research and development to develop technologically advanced products, and a turnaround at Minda Furukawa, the company beckons attention.

Raymond is one of India’s largest textile manufacturers. Premium product launches in the branded fabric and branded apparel segments, cost rationalisation initiatives, store additions in smaller cities, benefits of the recently concluded capex programmes, and monetisation of the Thane-based land will be drivers of earnings and cash flow.

Sanghi Industries has witnessed a sharp correction as its Q4FY18 numbers were hit by a 15-day plant shutdown. Sanghi has one of the lowest cement production costs and is expected to post 18-20 percent volume growth in FY19 driven by its entry into the high-margin Mumbai market. The company is on track to double its cement capacity to 8 MT by FY20.

Transport Corporation of India (TCI) reported strong financials in FY18 and should benefit from recent government initiatives such as the Dedicated Freight Corridor, Sagarmala and BharatMala as well as growing industry demand. TCI currently trades at a valuation which is at a discount to its industry peers.

VA Tech Wabag, one of the world’s leading companies in the water treatment field, had a difficult FY18, marred by misses both in revenue and order intake. The decision to complete the APGENCO projects resulted in ballooning of receivables. The company expects the receivable issue to get sorted in FY19 along with an improved ordering environment.

For more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.