We have been positive on Reliance Nippon Life Asset Management (RNAM) as we sniffed the winds of change following the mounting financial problems of the ADAG group. Just three weeks ago, we reiterated our stance by recommending the stock as weekly tactical pick. Read: Weekly Tactical Pick: Reliance Nippon Life Asset Management

As anticipated, Reliance Capital is selling of its entire stake (42.88 percent) in the asset management company (AMC), Reliance Nippon Life Asset Management (RNAM). According to Thursday’s stock exchange release, Nippon Life Insurance, a co-promoter, will increase its stake in the AMC to 75 percent, from the current 42.88 percent. Reliance Capital will exit the remaining part of the stake through offer for sale to other financial investors.

Stake sale triggers an open offer

On the execution of the announced deal, Nippon Life will be the largest shareholder and exercise sole control over RNAM. Reliance Capital will receive proceeds of about Rs 6,000 crore by selling its stake, which it will use to reduce its outstanding debt.

The stake purchase by Nippon Life will trigger an open offer to minority shareholders of RNAM holding around 14 percent stake in the AMC. SEBI’s (Substantial Acquisition of Shares and Takeovers) Regulations requires mandatory open offer in the event of any substantial change in shareholding or change in control of the company.

Furthermore, if a party already holds at least a quarter of the target's voting rights (in this case Nippon Life holds 42.88 percent in AMC), a mandatory open offer will be triggered if that party acquires more than 5 percent of the target's voting rights in any financial year.

Accordingly, Nippon Life will make an open offer at Rs 230 per share.

Exit of Reliance ADAG will help soothe investor worries

RNAM, the first AMC to list in the country, made its debut on bourses in November 2017 at around Rs 295, a premium of 17 percent over its issue price of Rs 252.

While its overall AUM growth moderated in FY19, finer details of its business are very encouraging. For instance, RNAM is the industry leader in retail assets. Retail assets form 39 percent of its average AUM, much better than the industry’s retail AUM of 26 percent. This is positive as retail flows typically consist of high-earning equity assets and are stickier than institutional flows. Read: Reliance Nippon: Soft FY19 numbers, but ADAG stake sale may move the needle

Despite reporting healthy trends in asset flows, the stock of RNAM has remained under pressure. The financial problems of the Reliance ADAG Group — which the company is part of — have given the scrip a hard time.

Even though Nippon Life is an equal partner with 42.88 percent stake in the AMC, Reliance Capital’s stake has been a key overhang for the stock. Hence, Reliance ADAG group’s decision to reduce its stake in the business will help assuage investors’ concerns.

Deal positive, considering RNAM’s exposures

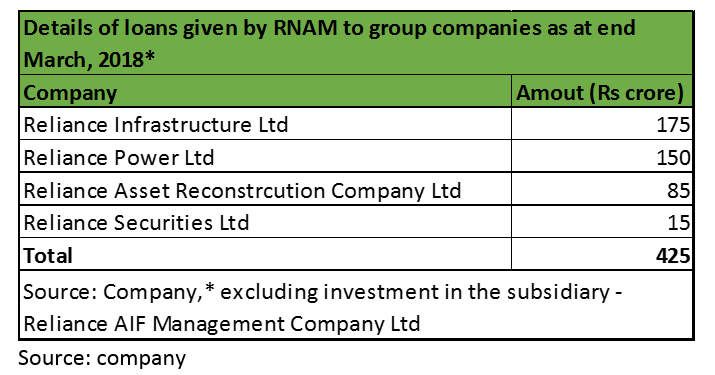

RNAM has extended inter-corporate deposits (ICDs) to companies belonging to the ADAG Group in the past. As of March 2018, RNAM had ICDs of Rs 425 crore, which have now reduced to around Rs 380 crore.

At the scheme level, debt funds of RNAM have exposure of around Rs 1,600-1,700 crore to group companies. Monetisation of RNAM stake, along with the other deals under way, will enhance ADAG Group’s debt servicing and/or repayment capability and to that extent is a positive news for MF investors of RNAM.

Investors in RNAM’s debt schemes have taken a hit on their investment as NAV was marked down following the rating downgrade of a couple of ADAG Group companies (Reliance Home Finance and Reliance Commercial Finance).

Shareholders of RNAM need to closely monitor the unwinding of exposure to ADAG at the company (ICDs) as well as the scheme level.

What should investors do?

The stock has rallied more than 20 percent over the past month. Despite the rally, RNAM’s valuations are reasonable, considering its strong retail brand, improving asset mix and well -diversified sourcing platform. Further, RNAM being the fifth-largest asset management company (AMC) in the country will continue to benefit from the structural growth in the MF industry.

At the current market capitalisation of Rs 13,900 crore, RNAM is trading at 6 percent of average MF AUM of Rs 2,33,600 crore as of March-end. In terms of P/E metric, RNAM stock is trading at 23 times FY21 estimated earnings. On a relative basis, the valuation is very compelling. The scrip is trading at a discount of more than 40 percent to HDFC AMC’s valuation.

The most common pushback while comparing with HDFC AMC’s valuation is that HDFC AMC is in a league of its own and commands a premium valuation for superior return ratio and strong parentage. While a rightful discount to HDFC AMC is justified, RNAM is trading at a significant discount, which we think should now narrow following the change in parentage and hence, long-term investors should hold the stock.Follow @nehadave01

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.