Dear Reader,

Indian markets last week experienced one of their strongest performances in a long time. The overall market showed robust activity, with broader indices outperforming the main indices. This significant upward movement was supported by simultaneous buying from foreign and domestic investors, a rarity in recent times.

Typically, when foreign institutional investors (FIIs) are buying, domestic funds tend to sell, and vice versa. However, this week saw both groups actively participating in the cash market, with FIIs quickly closing their short positions.

Domestic funds are also keen to take advantage of this situation to enhance their net asset values (NAV) as the end of the current fiscal year approaches.

The week ended with the large-cap index closing 4.6 percent higher, the mid-cap index rising by seven percent, registering the biggest weekly gain since February 2021, and the small-cap index closing eight percent higher, recording the biggest gain since June 2020.

During the week, the Sensex gained 4.16 percent, and the Nifty50 added 4.25 percent. All the sectoral indices closed higher, with Realty and Media adding nearly eight percent each and Pharma, Auto, and PSU Bank adding around six percent each.

After 13 weeks, FIIs turned buyers with purchases worth Rs 5,819.12 crore during the week, while Domestic institutions bought equities worth Rs 4,337.83 crore.

Global markets also closed positive for the week, with the MSCI World index closing 0.66 percent higher.

US stocks closed the week in positive territory, with the mid-cap index rising for the first time in 2025. Tech stocks were under pressure, with the Nasdaq closing flat compared to a decent performance in other indices.

The US Fed left rates unchanged but expected 50 basis points of rate cuts this year. However, expectations for inflation in 2025 increased, and the GDP forecast was lowered.

In Europe, the STOXX Europe 600 Index closed 0.56 percent higher after two weeks of negative closing. Among the major indices, the DAX fell 0.41 percent, the CAC 40 and the UK's FTSE 100 closed flat, and Italy's FTSE MIB gained 0.98%.

All European central banks maintained their interest rates this week; however, many bankers expressed concerns about the uncertain environment created by Trump's policies. European Central Bank (ECB) President Christine Lagarde emphasized that the ECB would remain vigilant due to the uncertainties arising from escalating trade tensions.

Only the Swiss National Bank (SNB) reduced its policy interest rate by a quarter percentage point to 0.25%, citing low inflationary pressure and increased risks to the economy.

In Asia, Nikkei 225 closed 1.68 percent higher on news of Warren Buffett increasing his stake to 10% in Japanese trading companies. The Bank of Japan's cautious stance by holding rates steady aided the rise, though there was expectation of a rate hike in certain circles.

China went against the trend, with the Shanghai Composite losing 1.60% and the Hang Seng Index slipping 1.13%.

Data from China's real estate sector continues to be depressing, with property development investment sinking 9.8% in the first two months of 2025 on a Year-over-Year basis after falling 10.6% in December.

A short-covering rally

In its third week of recovery, the Nifty Index has experienced five consecutive days of gains. After previously setting a record for the most days of continuous decline, we are now achieving a record for the most days of advance. Looking at the monthly timeframe, we are on track to close positively after five months of declines.

The previous occurrence was in 1996 when the fall led to eight months of market recovery back to the highs. There is a good chance we may see a similar recovery.

The Nifty index gained 1000 points, prompting foreign institutional investors (FIIs) to reduce their short positions. Meanwhile, domestic institutions continued to purchase, making it costly for FIIs to cover their positions at higher prices. This behaviour is unusual, especially at this magnitude. The week concluded with an all-time high of 74942 net long contracts.

Source: web.strike.money

The volume of put options to call options reached 0.79 at its peak and is currently declining. This high ratio indicates excessive pessimism, which often signifies market bottoms, as it has in the past. Now that the ratio is falling and trending downward, it aligns with the bullish trend observed in the market. We should look for the indicator to reach around 0.66 or lower before we start considering a potential market top, and we are still quite far from that. This has been the typical range for the indicator over the past one to two years.

Source: web.strike.money

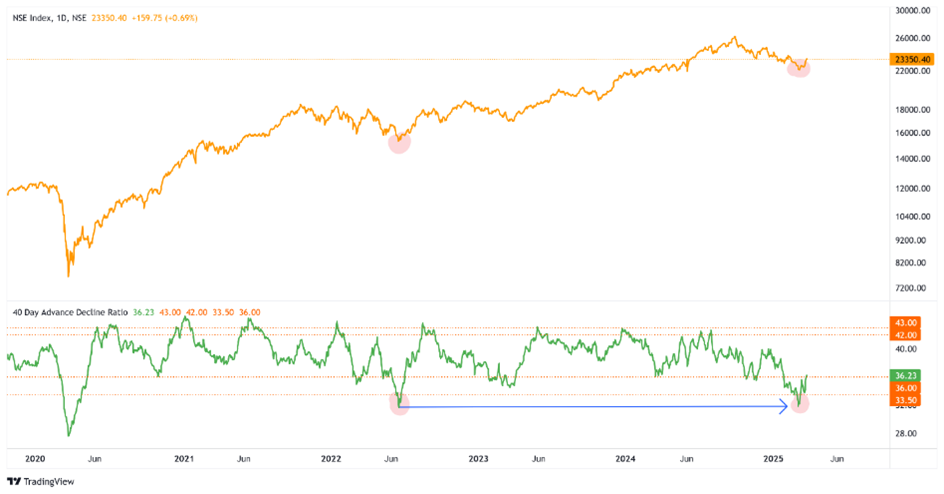

The 40-day advance/decline (A/D) ratio has decreased to levels comparable to those observed in 2023 but has recently begun to recover. The ratio is currently exhibiting higher highs and higher lows, which indicates a classic uptrend in market breadth. This trend aligns with the positive movement in the market and suggests a reversal of the broad-based sell-off we have experienced over the past few months.

Source: web.strike.money

Sector Rotation

Nifty 50 – the Benchmark Index, gave a spectacular rally to close up by more than four percent this week at 23350.40.

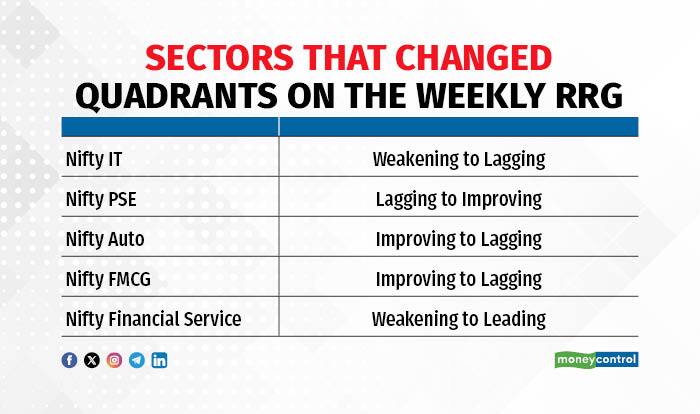

Indices positioning on Weekly Timeframe

Weakening Quadrant: Nifty Bank has stayed in its current quadrant but is gaining momentum and moving towards the Leading quadrant. It lags slightly behind Nifty Financial Service, which demonstrated greater strength and momentum to enter the Leading quadrant this week. This sector should be a focus for next week.

Lagging Quadrant: Nifty IT is a new entrant in the Weakening quadrant, which indicates weak strength and momentum. Nifty Consumer Durables and Nifty Pharma have remained sluggish in this quadrant. However, Nifty Media and Nifty Realty have shown an increase in momentum, while Nifty PSU Bank has gained enough momentum to move upward and transition into the Improving quadrant. Additionally, Nifty Auto and Nifty FMCG are also new entrants, but they are coming from the Improving quadrant, suggesting a lack of strength and momentum.

Improving Quadrant: Nifty Oil & Gas has been moving horizontally for the past five weeks and is approaching the Leading quadrant. This indicates that it is progressing steadily and attempting to outperform the benchmark, although it lacks momentum. Nifty Metal has extended its positive momentum; if this trend continues next week, it may enter the Leading quadrant, making it a sector to watch. Nifty Energy has also seen an extension of its positive momentum but remains far from the Leading quadrant, suggesting that it will need more effort to reach that level. Meanwhile, Nifty PSE has entered the Leading quadrant due to its increasing momentum. It will be important to see if it can maintain this momentum.

Leading Quadrant: Nifty Private Bank has once again shown significant momentum and is positioned in the Leading quadrant.

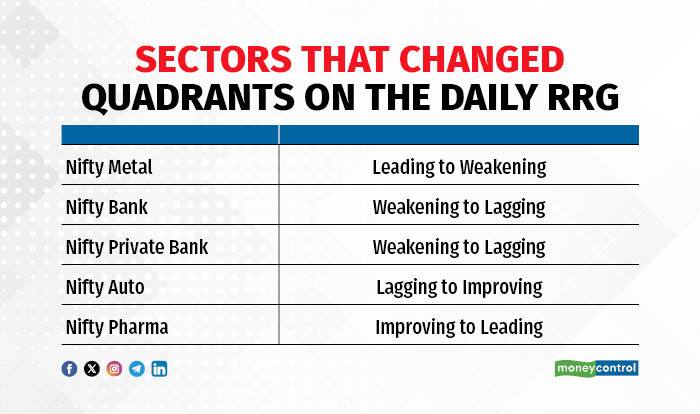

Indices position on the daily timeframe

Weakening Quadrant: Nifty Metal lost its momentum and entered this quadrant. Nifty Financial Services remained in this quadrant but showed some increase in momentum and seems to have taken a 'U' turn to head back towards the Leading quadrant.

Lagging Quadrant: Nifty Bank and Private Bank transitioned from the Weakening quadrant, gaining momentum on the last day to move towards the Improving quadrant. In contrast, Nifty IT continued to head westward, not gaining momentum and underperforming.

Improving Quadrant: Nifty Auto gained significant momentum and has moved into this quadrant from the Lagging category. Nifty Realty has also continued its positive momentum and is approaching the Leading quadrant. Additionally, Nifty Media performed well, and with a bit more momentum, it could enter the Leading quadrant in the next couple of days. There has been little change in Nifty Consumer Durables. Nifty FMCG and Nifty PSU Bank remain in their current quadrant but have lost some momentum and are trending downward. These two sectors are very close to the border, and if momentum picks up, they could potentially move into the Leading quadrant.

Leading Quadrant: The Nifty PSE, Nifty Energy, Nifty Oil & Gas, and Nifty Infrastructure sectors remained in the Leading quadrant, although they displayed signs of momentum saturation. Nifty Pharma has recently joined the Improving quadrant, making it a sector to watch in the upcoming days.

Stocks to watch

Among the stocks expected to perform better during the week are Bajaj Finance, Muthoot Finance, Chambal Fertiliser, UPL, Shree Cements, SBI Cards, ICICI Bank, JW Steel and Indigo.

Among the stocks that can witness further weakness are Astral, TCS, Tata Elxsi, Yes Bank, Hero MotoCo, Hindustan Unilever, Titan, Colgate Palmolive, IDFC First Bank and L&T.

Cheers, Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.