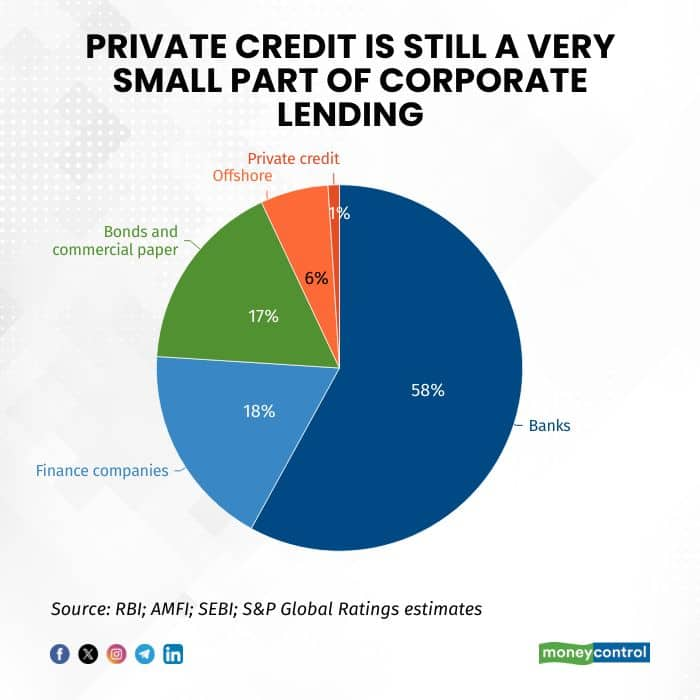

Globally, the private credit space has already surged past the $2 trillion AUM mark, but India is still in its early innings, with barely $25 billion in assets under management. The underpenetration, coupled with rising confidence in the Indian growth story, is setting the stage for a sharp upsurge in the domestic private credit market, pushing it closer to the mainstream.

For the first half of 2025, the total deployment in private credit touched $9 billion across 79 deals, which marked a 53 percent YoY jump, and roughly 3x compared to H2 2024 levels. According to an expert, the total AUM of domestic private credit can grow between 30-40 percent for the next few years.

Earlier, private credit was seen as a high-yield opportunity for HNIs, family offices, and institutional investors. However, as more borrowers are looking for flexible, tailored credit options, the private credit space is developing into a solutions-driven financing ecosystem, with funds stepping into roles traditionally dominated by banks.

Further, as private capex spurs into action once again, companies hunt for faster, more flexible capital, according to fund managers, private credit will shift from a return-seeking product to an integral part of the corporate financing stack.

At the same time, the investor profile is set to broaden meaningfully. Family offices, high networth individuals, and what most experts called the "sophisticated investor," are increasing their allocation towards private credit. Global funds are also looking to increase their allocation towards India, as clearer signs of opportunity emerge.

Private credit is usually painted in broad strokes: high-risk, high-yield capital given to distressed companies in the aim of higher returns. However, as the category has evolved, experts argue that returns vary based on the borrower profile, structure, collateral, and tenor.

Across fund managers, there is broad consensus that private credit returns in India today reflect both the risk premium for bespoke structures and the market’s early-stage nature. Based on the fund, returns can vary from 11-12 percent IRR for performing credit funds to 30 percent IRR for venture debt, explained an expert, who wished not to be named.

If a borrower goes to a bank, they will be offered a cookie-cutter loan, with standard repayment schedules. For a borrower that needs more flexibility, or a tailor-made repayment programme, private capital steps in, explained Ankur Jain, MD - Private Credit Strategies, InCred Alternative Investments. "Because of this flexibility, a borrower will give me a higher rate of interest. Further, the inherently illiquid nature of private credit funds adds to the premium return."

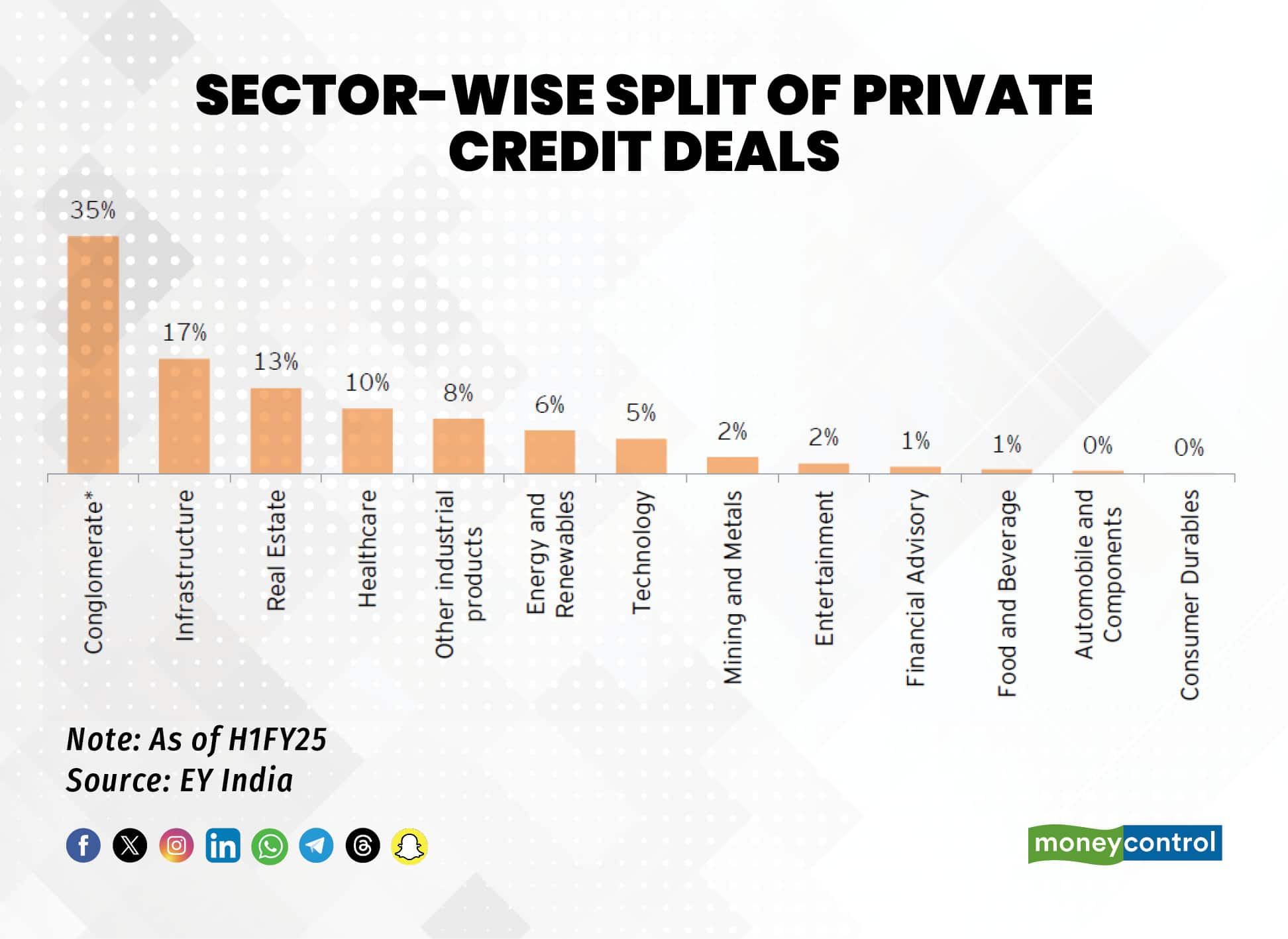

On the sectoral front, infrastructure led private credit activity, followed by real estate and healthcare. Further, nearly 17 percent of the capital raised by borrowers in the first half of this year was deployed towards forward-looking initiatives, including growth capital, capacity expansion, and strategic acquisitions of companies, according to EY India.

India’s broader capex cycle and the structural build-out across infrastructure and industries are driving a wave of high-growth opportunities. "With strong demographics and rising consumption which feeds directly into manufacturing, sectors such as chemicals, pharma, steel, engineering, and auto components will see strong expansion going ahead," noted Kanchan Jain, Head at Ascertis Credit Group.

Ankur Jain reaffirmed this, noting that as India enters a new domestic capex cycle, manufacturing remains one of the biggest demand pockets. He added that the new-age sectors are also "capital guzzlers."

“There is a clear shift towards companies in clean energy, module manufacturing, electric vehicles, and more. These firms need structured capital for expansion, working capital, and capex financing," he said.

Key risks

Most of the experts agreed that private credit in India has not seen a full credit cycle, growing mainly in a benign environment since 2020. "I think about it, this industry has not seen a full credit cycle. Asset managers are mushrooming every day, funds are coming every day," said Ankur Jain.

"Not all the fund managers and AMCs have seen a bad cycle. So in a credit downturn, how will their portfolio be stress tested? How will the recovery of bad credit happen? I think that still remains untested and that is I would say a single biggest risk in this industry as of right now."'

Another private credit expert concurred. There are very few funds which have gone through a 10-year tenor to see a full cycle, he noted. "This also becomes an important aspect in picking the right fund, because first-time fund managers who entered in a secular growth phase may not be able to navigate this."

On the flip side, Kanchan Jain said for established players, many cycles have come and gone. "The rate hike cycle, rate cut cycle with the pandemic, and so on. Therefore, it's not fair to say that private credit funds haven't gone through cycles. They've gone through a lot of cycles and the returns have proven to be resilient."

As with any credit companies, the risk of defaults or NPAs is always present. However, to mitigate this, some funds take significant cover. "We take a security cover of 2 to 3x in the form of either hard collaterals or liquid securities which can be liquidated, just in case things go south," said an expert in the field.

Five years from now

India used to be a miniscule portion of private credit in Asia five years ago, but that has changed, added Kanchan Jain. "Today, India is the second largest private credit market in India."

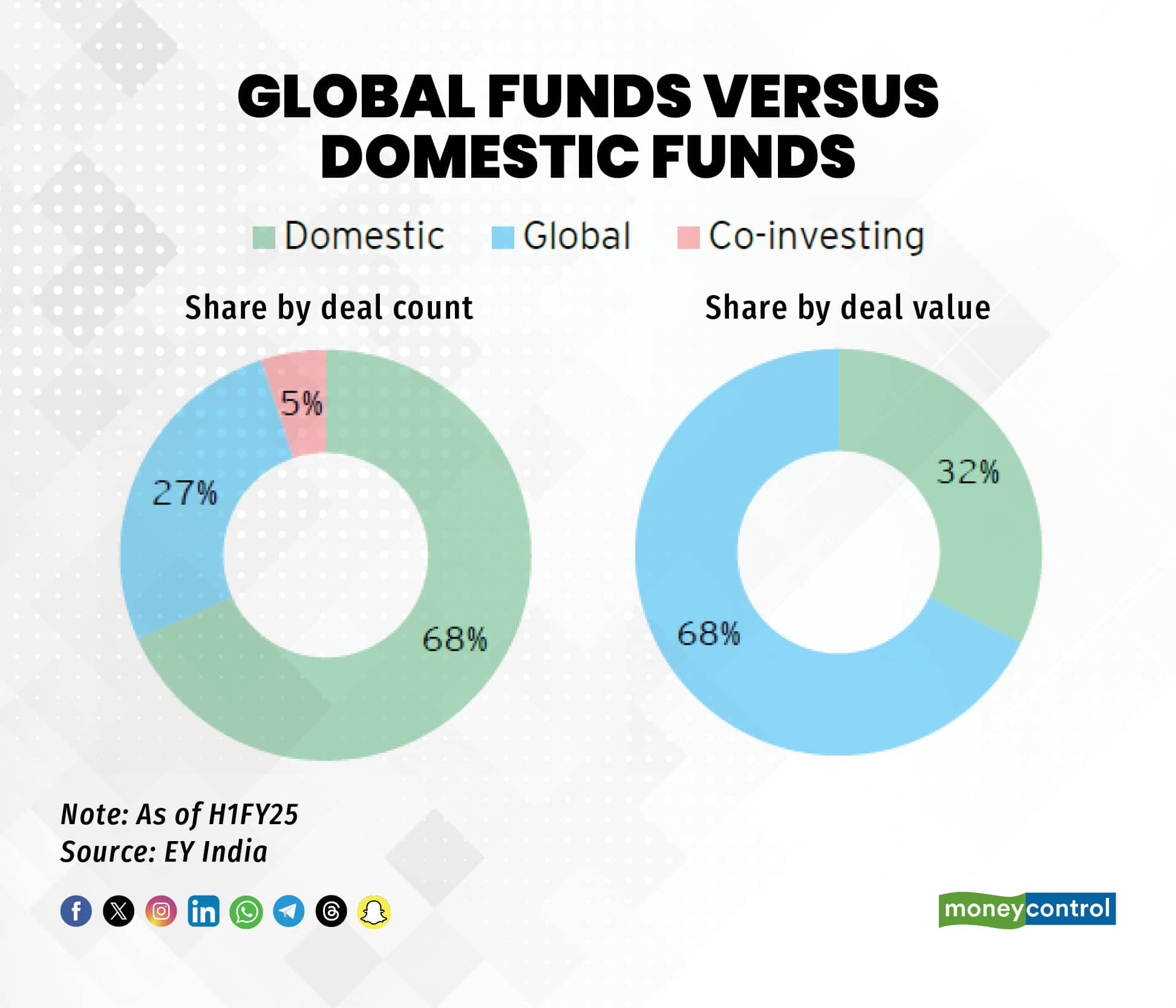

So far in 2025, global capital remained the primary driver of India’s private credit inflows, contributing the majority of capital despite lower deal participation. However, going forward, analysts expect increased participation from domestic investors, as private credit comes into the mainstream.

According to experts, India has an estimated five to seven year window where the demand for bespoke capital will remain high. Corporates prefer speed, certainty, and flexibility in capital structuring, and private lenders are stepping in where traditional lenders face constraints.

The next phase will see private credit becoming more specialised as the nature of deals have seen a change. According to Ascertis Credit, borrowers today have stronger balance sheets compared to a decade ago, making the segment more resilient.

At the same time, consumption-linked businesses, new economy platforms with predictable revenue models, and sectors with asset light operations continue to draw interest from investors.

EY India is guiding Indian family offices to achieve 8-12 percent direct private credit allocations, compared to the current modest allocation within the broader private markets bucket

The sector is likely to continue to mature, with some predicting 30 to 40 percent AUM CAGR over the next five years. While the story is still in its early chapters, the foundation is being built for a strong, booming market over the next decade.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.