The market closed the week on a negative note amid rangebound and volatile trading on February 21, continuing downtrend for second consecutive week. Trump administration's announcement of reciprocal tariffs and FOMC minutes signalling pause in further rate cuts citing inflation risk ahead along with persistent FII selling weighed on the market sentiment. However, the consistent correction in oil prices and significant DIIs buying supported the market.

The market participants are expected to maintain cautious stance in the truncated week ahead starting from February 24, with focus on quarterly economic growth numbers by India and US, monthly auto sales data, developments over tariffs by Trump administration, and updates related to peace talks between Ukraine & Russia, according to experts. The volatility may increase considering the expiry of monthly Futures & Options contracts due next week.

The Nifty 50 fell 0.6 percent to 22,796, and the BSE Sensex declined 0.8 percent to 48,981, however, there was strong buying interest in broader markets after recent steep fall, with the Nifty Midcap 100 and Smallcap 100 indices rising 1.7 percent and 1.5 percent, respectively. Auto stocks were under pressure on fear of increasing competition due to likely entry of Tesla, and reciprocal tariffs fear dampened sentiment in pharma counters. FMCG, and IT stocks were also in red, but metal stocks were shining.

"The market's mood remains cautious, with pessimistic sentiments likely to linger until there is a marked improvement in corporate earnings and a conducive environment with easy global liquidity and stabilised currency," Vinod Nair, Head of Research at Geojit Financial Services said.

According to him, India is currently lagging behind its Asian peers, as FII outflows remain high, with the "sell India, buy China" strategy continuing to yield returns for the time being.

The market will remain shut on February 26 for Mahashivratri.

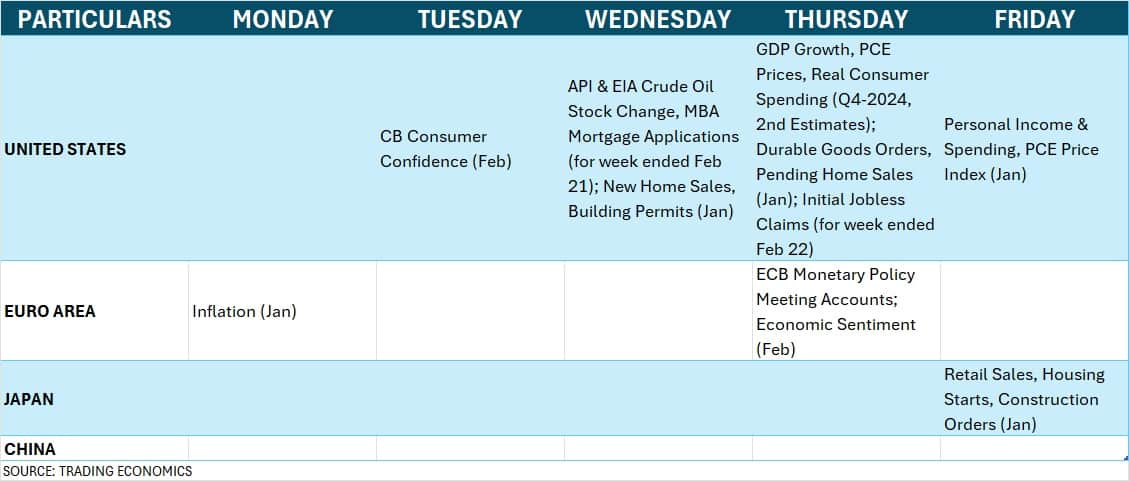

Here are 10 key factors to watch next week:

US GDP

Globally, all eyes will be on the second estimates for US GDP numbers for fourth quarter of 2024 due on February 27. According to advance estimates published last month, the US economy grew 2.3 percent in Q4-2024, much lower compared to 3.1 percent growth reported in Q3-2024.

Other upcoming pivotal indicators such as the second estimates for Core PCE prices and real consumer spending in Q4; CB consumer confidence data for February; and PCE price index, new home sales and personal income & spending numbers for January; and weekly jobs data from US will also be watched next week.

All these data points are important to get clues about the central bank’s future monetary policy.

Further, the US trade policy developments will also be watched next week as recently the Donald Trump said he would introduce around 25 percent tariffs on pharma, auto and chips. He also promised reciprocal tariffs for India and China for trade fairness.

Global Economic Data

Further, the focus will also be on the January inflation numbers from Euro zone, ECB monetary policy meeting accounts, and retail sales for January from Japan.

India GDP

Back home, the market participants will keep an eye on the GDP growth numbers for December 2024 quarter and second estimates for the full year (FY25) economic growth figures due on February 28. As per the preliminary estimates, the economy in the full year grew 6.4 percent against 8.2 percent growth in the previous year. Further, most economists expect some improvement in Q3FY25 GDP numbers (December quarter) against 5.4 percent expansion in Q2FY25.

Additionally, on the same date, the focus will also be on the fiscal deficit numbers, and infrastructure output for January along with bank loan and deposit growth for fortnight ended February 14, and foreign exchange reserves for week ended February 21.

Auto Sales

Auto stocks will be in focus as over the next weekend, two-wheeler, four-wheeler, tractor and commercial vehicle companies will release their monthly sales volume numbers for February. Two-wheeler segment reported healthy numbers, but there was mixed trend in passenger vehicle, commercial vehicle and tractor segments in January.

Further, the activity at the institutions desk will also be watched next week as foreign institutional investors (FIIs) remained net sellers for the passing week but domestic institutional investors (DIIs) consistently managed to compensate the FII outflow, in fact, giving major support on every fall in the market.

FIIs net sold Rs 7,793 crore worth of shares in the cash segment last week (ended February 21), taking the total selling for current month to Rs 36,977 crore, however, DIIs net bought Rs 16,582 crore worth shares during the week, and Rs 42,601 crore in February.

According to most experts, the FII flow may not return to India, until there is a strong revival in economic and earnings growth.

Meanwhile, the US dollar index, which measures the dollar value against leading six currencies, fell by 0.14 percent during the week to 106.64, trading tad below the midline of Bollinger bands, while the US 10 year Treasury yield also dropped further by 1.05 percent to 4.431 percent, continuing downtrend for six consecutive weeks.

Oil Prices

The movement in oil prices will also be watched next week as subdued prices remained favourable for oil importers like India, in fact, acting as a supportive factor for equity markets. Brent crude futures, the international oil benchmark, failed to sustain above $80 a barrel for several months now, down by 0.41 percent during the week to settle at $74.43 a barrel. The price continued to trade below all key moving averages (10, 20, 50, 100 and 200-week EMAs), signalling weakness.

Additionally, "short-term movements in oil prices will depend on whether the US increases or reduces sanctions, a decision likely influenced by Russia’s willingness to negotiate an end to its conflict with Ukraine," Kaynat Chainwala of Kotak Securities said.

The mainboard segment will be quiet next week, may be due to subdued market conditions, but the action remains in the SME section with three IPOs opening for public subscription. Nukleus Office Solutions will hit Dalal Street on February 24, followed by Shreenath Paper Products on February 25, and Balaji Phosphates on February 28.

Further, HP Telecom India, and Swasth Foodtech India will close their initial public offerings on February 24, while the subscription for Beezaasan Explotech issue will remain open till February 25.

On the listing front, investors can start trading in Royal Arc Electrodes, and Tejas Cargo India shares effective February 24, followed by HP Telecom India, and Swasth Foodtech India shares on February 28. In the mainboard segment, Quality Power Electrical Equipments will be the last debut on the bourses for the current month, on February 24.

Technical View

Technically, the trend is looking week given the Nifty 50 traded near the lower band of Bollinger bands along with below key moving averages (10, 20, and 50-week EMAs) and continuation of lower tops-lower bottoms formation for another week. The momentum indicators RSI and MACD also showed negative bias. The 22,600 (the trendline support) can act as a support in the near term as below it 22,000 (100-week EMA) being a major support, however, in case of rebound, 23,000-23,100 is acting as a stiff resistance as above this zone, 23,400 (10-week EMA) is the possible level to watch, according to experts.

F&O Cues, India VIX

The options data suggested that the Nifty 50 is expected to be in the broad range of 22,200-23,500 for the monthly F&O expiry week and the immediate range could be 22,500-23,100.

On the Call side, the 23,000 strike holds the maximum Call open interest, followed by 23,500 and 23,100 strikes, with the maximum Call writing at the 23,100 strike, followed by the 22,800 and 23,000 strikes. On the Put side, the maximum open interest was reported at 22,000 strike, followed by the 22,500 and 22,300 strikes, with the maximum Put writing at the 22,500 strike, followed by the 22,300 and 22,400 strikes.

The India VIX, which measures the expected market volatility, fell by 3.23 percent during the week to 14.53, but still near the higher zone. Bulls may get into comfort zone only if the VIX drops below 14 mark.

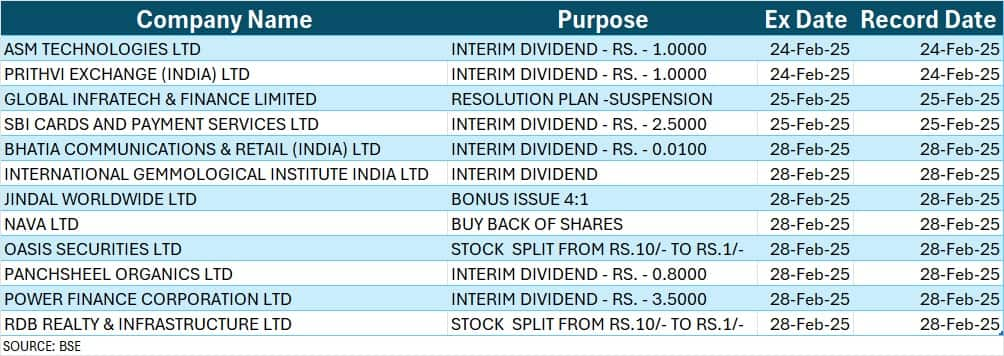

Corporate Action

Here are key corporate actions to watch out for next week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.