The week ending March 13 was a nightmare for the Indian equity markets, as the benchmark Nifty 50 recorded its biggest weekly decline since June 2022. This mirrored weakness in global peers amid escalated tensions between the US, Israel, and Iran, which kept oil prices elevated, raising fears over corporate earnings and economic growth. The turmoil also led to an elevated VIX, pressure on the rupee, and sustained FII outflows. Selling pressure was seen across sectors, while overall market breadth remained fragile, as tighter gas availability began to affect daily activity and higher crude prices reignited fiscal and inflation concerns.

Going forward, the market is expected to remain dominated by bears amid the ongoing US-Iran conflict and rising oil prices, with market stability unlikely until Middle East tensions ease. Further, market attention will focus on the FOMC meeting outcome and interest rate decisions of other central banks—ECB, BoJ, and BoE—scheduled for the week ahead, starting March 16, according to experts.

During the week, the Nifty 50 crashed 1,299 points (5.31 percent) to close at 23,151, while the BSE Sensex plunged 4,355 points (5.52 percent) to 74,564. The Nifty Midcap and Smallcap 100 indices declined 4.6 percent and 3.66 percent, respectively.

According to Vinod Nair, Head of Research at Geojit Investments, market direction is likely to remain influenced by the Israel-US conflict with Iran and crude trends, given their knock-on effects on inflation, corporate margins, the current account, and RBI policy space.

"A firm dollar and higher US yields may keep FIIs selective and volatility elevated. Selective value opportunities should persist in fundamentally resilient and domestically anchored themes, while energy-sensitive sectors may remain under pressure if oil prices stay elevated," he said.

With buying support from domestic institutions and cautious retail investors, a sustained recovery will likely require clear signs of geopolitical de-escalation, stabilization in crude prices, and improved clarity on LPG availability and sector-specific demand, he added.

Siddhartha Khemka, Head of Research, Wealth Management at Motilal Oswal Financial Services also agreed with Vinod, saying sustained foreign outflows and elevated oil prices could keep market sentiment cautious, while any signs of easing geopolitical tensions may provide relief.

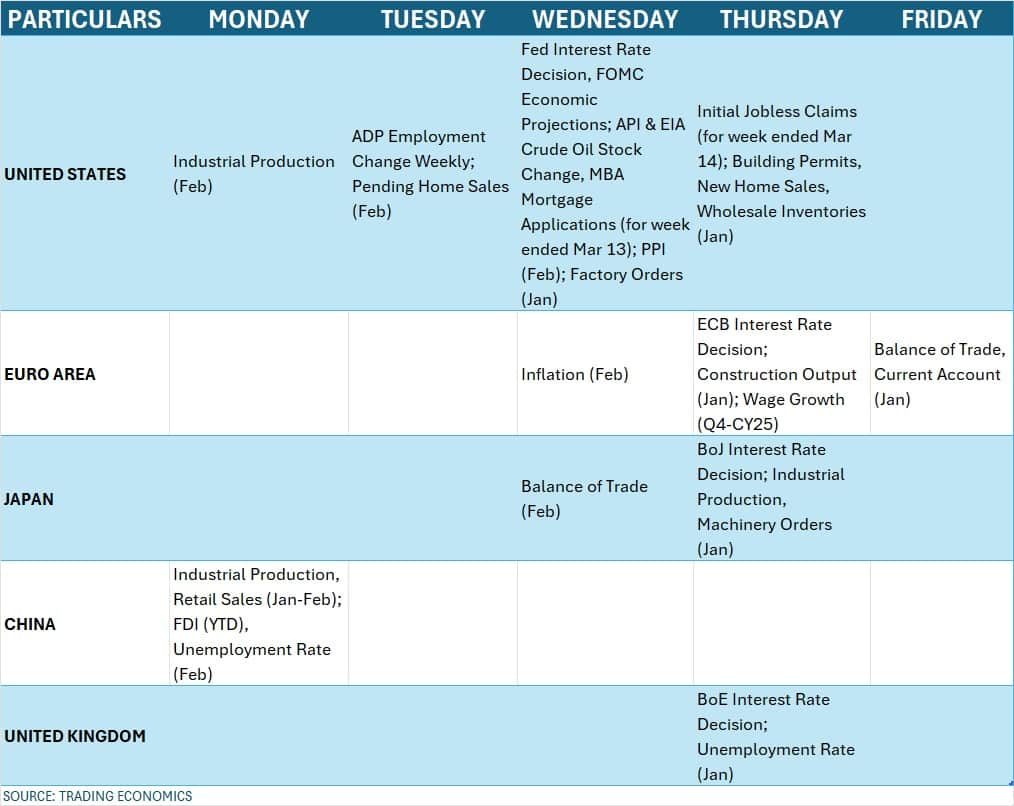

Here are 10 key factors to watch next week:

Strait of Hormuz-led Oil Crisis

The Middle East conflict that entered into third week will be the key factor to watch by the markets participants across asset classes, as the US-Iran standoff is unlikely to end soon considering the consistent attack by US defence forces and warning signals by Donald Trump to Iran to clear hurdles in the Strait of Hormuz waterway, a critical oil choke point through which 20 percent of global oil passes but Iran is not ready to do that as it demands removal of economic sanctions, assurances for no future military action, and no involvement in regime change. Ultimately, it has increased fears of oil supply disruptions.

As per latest news, the US defence forces targetted the military sites near Kharg Island, an important terminal for Iranian oil exports, adding more fuel to the ongoing West Asia tensions and becoming another reason to keep oil prices inflated in near future. Although the island’s energy infrastructure was not directly targeted, warnings from Donald Trump that Iranian oil facilities could be targeted if Tehran continues to disrupt shipping have heightened concerns over further supply risks, with traffic through the Strait of Hormuz already down to a fraction of normal levels.

Brent crude oil prices, which fell sharply from $119.5 a barrel level to $83.75 intraday on Monday but rebounded and maintained uptrend in following days, closed the week above $100 a barrel at $103.81, up 11.77 percent. Prices being above $100 a barrel is a major cause of concern for oil importing countries like India as it directly impacts the import bill, fiscal deficit numbers, inflation, earnings and economic growth.

In his first public remarks since assuming the role of Iran’s supreme leader, Mojtaba Khamenei reiterated that closing the Strait of Hormuz should remain a strategic tool to pressure the US and Israel, while warning neighbouring countries hosting US military bases that they could become potential targets. Additional support for oil prices came as the US Navy is not yet ready to escort commercial oil tankers through the Strait, suggesting supply flows may remain constrained in the near term.

Meanwhile, the International Energy Agency has agreed to release around 400 million barrels from strategic reserves, though even a record coordinated draw would cover only about 20 days of the roughly 20 million barrels per day of oil flows that could be at risk if the Strait were significantly disrupted, said Kaynat Chainwala of Kotak Securities.

FOMC Meet

Apart from West Asia crisis, globally, markets across asset classes will focus on the upcoming policy decision from the Federal Reserve, where rates are widely expected to remain unchanged but updated economic projections and commentary amid geopolitical tensions between US-Israel and Iran will be closely watched. The minutes of the last Federal Reserve policy meeting indicated that the Fed officials are mixed in their opinion with respect to interest rates.

Global Economic Data

Further, decisions from the European Central Bank, the Bank of England, and the Bank of Japan, along with US producer price index, factory orders, new home sales data, and weekly jobless claims, will also be in focus. All these central banks are expected to keep interest rates unchanged in their policy meetings next week.

China's industrial production, retail sales, unemployment rate, and Europe's inflation will also be watched in the coming week.

Domestic Economic Data

Back home, the participants will focus on the WPI inflation, unemployment rate and balance of trade data for the month of February due on March 16. According to economists, the inflation rate based on movement of Wholesale Price Index is expected to increase further in February from 1.81 percent in January.

Bank loan & deposit growth for fortnight ended March 6, and the foreign exchange reserves for week ended March 13 along with infrastructure output for February will release on the last day of week, i.e. March 20.

The Foreign Institutional Investors (FIIs) flow will also be closely watched next week as they remained persistent sellers in the Indian equity markets following the geopolitical tensions in the Middle East, weakening rupee against the US dollar, and rising oil prices which pressured earnings and economic growth. Now, the strong FII inflow to India requires healthy earnings recovery and easing of West Asia tensions.

FIIs have net sold more than Rs 35,000 crore in the passing week, taking the total selling in current month to over Rs 56,800 crore so far, the highest monthly outflow since February 2025. Remember, this is only first half of the month data.

On the contrary, Domestic Institutional Investors (DIIs) have net bought Rs 37,700 crore in recent week and more than Rs 70,000 crore worth shares in current month, fully offsetting FII outflow. This also could mean they have been providing strong support to the market in every correction.

Meanwhile, the Indian rupee weakened by 0.63 percent during the week to 92.49 against the US dollar, the fresh all-time closing low, and experts expect the currency to depreciate further if oil prices remain elevated which could hit India's fiscal deficit.

The US dollar index reached closer to upper Bollinger bands and hit 10-month high due to increasing demand for safe-haven amid geopolitical turmoil and market volatility, rising 1.66 percent to 100.49 in addition to 1.24 percent rally in previous week.

The primary market will see three new initial public offerings (IPOs) next week with two - agrochemical company GSP Crop Science, and Coal India subsidiary Central Mine Planning & Design Institute - from the mainboard segment opening on March 16 and March 20, while Novus Loyalty is the only SME company launching public issue next week on March 17.

Further in the mainboard segment, Innovision, which has extended IPO subscription period due to muted response from investors, will close its IPO on March 17. In last four sessions, the offer was subscribed only 30 percent. Meanwhile, Rajputana Stainless has provided an additional window to the investors to withdraw their bids till March 16. Hence, if both manage to close their IPOs successfully, then their listings can be possible next week.

On the listing front, Apsis Aerocom is the only company scheduled for its market debut on the NSE Emerge next week on March 18.

Technical View

Technically, the Nifty 50 remains completely under the bears' control, with the lower high–lower low formation still intact. The index is decisively trading below the 20-, 50-, and 100-week moving averages, closing not only below the long upward-sloping trendline (which previously acted as support but now acts as resistance) but also below the 61.8 percent Fibonacci retracement level (of the 21,744 low to the 26,373 high).

Overall, the trend is expected to remain weak despite intermittent pullbacks due to oversold conditions. The immediate support for the index is placed at 23,000 (a psychological level), followed by 22,800-22,700 as the crucial support (78.6 percent Fibonacci level). However, the 23,300–23,500 zone can act as immediate resistance, followed by 23,700.

F&O Cues

The weekly options data indicated that the 23,000 is expected to be crucial zone in the near term as breaking below it can open door for 22,800 and 22,500 levels, where the maximum Put open interest are placed. However, the 23,500 is expected to be resistance for the Nifty 50, followed by 23,600 and 23,700, which attracted maximum Call open interest.

The maximum Put writing was seen at the 22,800 strike, followed by the 22,500 and 22,600 strikes while the maximum Call writing was observed at the 23,500 strike, followed by the 23,600 and 23,200 strikes.

India VIX

The elevated volatility is expected to keep uncertainty in the equity markets. The fear gauge India VIX spiked 13.91 percent during the week to 22.64, the highest closing level since May 2024, in addition to 45 percent surge in previous week, signalling major discomfort for bulls. It is necessary for VIX to fall decisively below 13 level to get the bulls back into comfort zone.

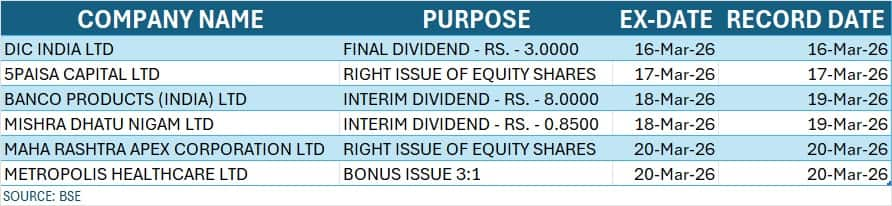

Corporate Action

Here are key corporate actions taking place next week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.