The market sustained a downward bias for the second consecutive week, ending May 30, amid volatility and range-bound trading, as weak global cues and a lack of major positive triggers weighed on sentiment. However, the hope for a third interest rate cut by the RBI this week, along with a benign inflation trajectory, a better monsoon forecast, and healthy GDP growth in Q4FY25, restricted the weekly loss to 0.4 percent.

On a monthly basis, the index gained 1.71 percent in May, continuing its northward journey and higher highs formation along with a Three White Soldiers-like pattern formation for the third consecutive month.

The market, in the coming week starting from June 2, is expected to first react to the monthly automobile sales data announced by corporates effective last Sunday. Overall, the sentiment may turn positive amid possible range-bound trading with a buy-on-dips strategy. The rising hope of interest rate cut due to supportive inflation trajectory and positive auto sales data may support the market mood, while the market participants will keep an eye on the monsoon progress, manufacturing & services PMI data, US jobs data and ECB interest rate decision along with further fresh developments with respect to US tariffs, experts said.

The Nifty 50 was down 102 points (0.41 percent) at 24,751, and the BSE Sensex slipped 270 points (0.33 percent) to 81,451, while the Nifty Midcap 100 and Smallcap 100 indices outperformed the benchmark indices, rising around 1.29 percent and 1.36 percent respectively, for the week.

Next week, "interest rate-sensitive sectors—particularly PSU banks—are likely to remain in focus amid growing hopes of an RBI rate cut. Additionally, the release of monthly auto sales and volume data could trigger sector-specific moves in the automobile space," Siddhartha Khemka, Head - Research, Wealth Management at Motilal Oswal Financial Services, said.

Further, he expects markets to maintain their positive momentum in June on the back of strong Q4 GDP numbers, hopes of an RBI rate cut, and consistent institutional inflows.

Here are 10 key factors to watch out for next week:

RBI Interest Rate Decision

The key factor to focus on next week would be the interest rate decision by the RBI Monetary Policy Committee due on June 6. Most economists expect the central bank to cut the interest rate for the third time this year by 25 bps to 5.75 percent,t given the inflation below its 4 percent target, which experts feel is already discounted by the market. The commentary over the further rate cut path and any change in full year inflation and growth forecast will be watched.

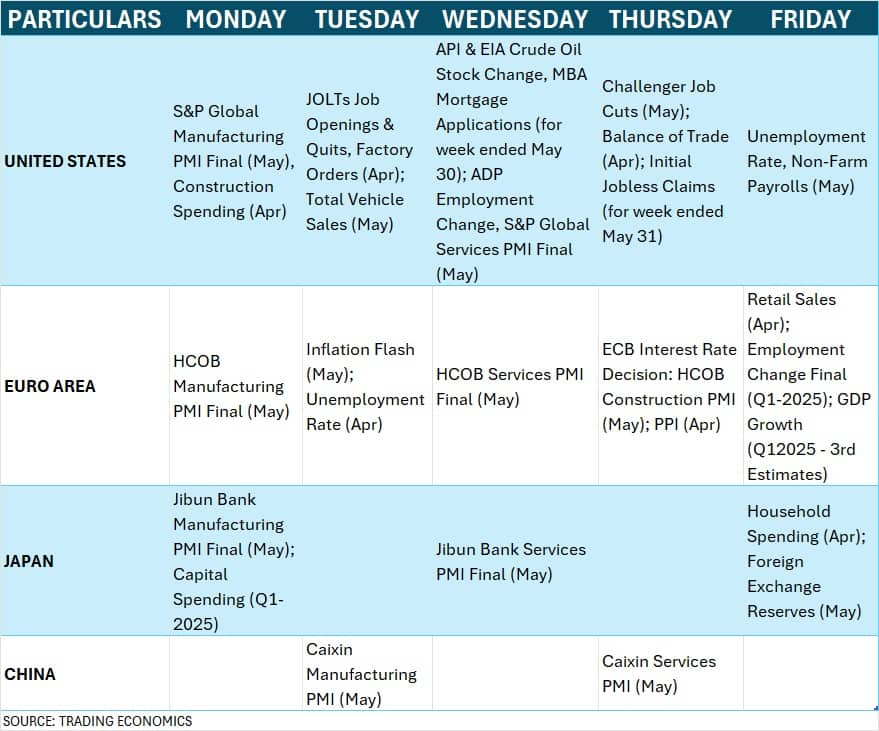

Domestic Economic Data

Apart from RBI policy meeting, the market participants will keep an eye on the final manufacturing and services PMI numbers due on June 2, and 4, respectively. According to the preliminary estimates, the manufacturing PMI increases to 58.3 in May against 58.2 in April and services PMI jumped sharply to 61.2 from 58.7 in the previous month.

Further, as the week progressed, bank loan & deposit growth for the fortnight ending May 23, and foreign exchange reserves for the week ending May 30 will be released on June 6.

US Jobs Data

On the global front, the focus would be on the jobs data (unemployment rate, non-farm payrolls for, JOLTs jobs opening & quits for May, etc) along with the developments with respect to US bond market and Trump tariffs, which will give indication about further rate cut path of the US Federal Reserve. The unemployment rate of the US is expected to be steady at 4.2 percent for May compared to the previous month.

Last week, the US trade court blocked Trump’s global tariff agenda. However, later the Trump administration appealed the court ruling that had declared the tariffs illegal. White House trade adviser Peter Navarro said that the Trump administration will seek to enact tariffs through other means if it ultimately loses the court fights over its trade policy. "While industry-specific tariffs on steel, aluminum, and autos stay in place, the fate of broader duties depends on the ongoing court appeal. Trump’s accusations of China violating the trade truce add another layer of uncertainty for markets," Kaynat Chainwala of Kotak Securities told Moneycontrol. Last week, despite stalled US-China trade talks and renewed tariff concerns, the US markets had a healthy closing.

Meanwhile, the US 10-year Treasury yields snapped a four-week winning streak, falling 2.46 percent to 4.398 percent but still in the broad trading range of 3.88 percent to 4.59 percent of the week ended April 11.

Global Economic Data and ECB Interest Rate Decision

Further, globally, investors will keep an eye on the final manufacturing and services PMI data for May from several key nations, including the US, China, and Japan. Inflation flash data for May, retail sales for April, and third estimates for Q1-2025 GDP numbers from Europe will also be watched next week.

Meanwhile, the focus will also be on the interest rate decision by the European Central Bank due on June 5. Most economists expect the central bank to slash the interest rate by 25 bps to 2 percent, given that inflation is under control and despite the uncertainty caused by Trump's trade tariffs.

Oil Prices

The subdued oil prices remained supportive for oil importing countries like India as the Brent crude futures, the international oil benchmark, dropped 3.09 percent during the last week to $62.78 a barrel, continuing downtrend for another week. The prices remained well below all key moving averages with EMAs trending downward, signalling weakness in prices. In fact, the prices have been under $70 a barrel since April. The legal disputes between the White House and US courts over the legality of trade tariffs also weighed on prices.

Investors turned cautious ahead of the OPEC+ meeting, amid speculation of a third consecutive production increase. "Oil prices are likely to extend declines next week as OPEC+ agreed to yet another super-sized production hike of 411,000 barrels a day for July, fuelling concerns of a supply glut," Kaynat Chainwala said.

Back home, the market participants will closely watch the mood of FIIs (Foreign Institutional Investors) as they remained net sellers for another week, offloading Rs 418 crore worth of shares last week, which was far lower than the Rs 11,591 crore worth of shares sold in the previous week. For the month, FIIs remained buyers for the third consecutive month, acquiring Rs 11,773 crore worth of shares in May. Experts are hopeful that the FIIs may remain buyers in Indian equities given the subdued US dollar index, slowing US and Chinese economies, and healthy India growth, and likely further rate cuts by RBI to support growth while a benign inflation trajectory.

On the contrary, DIIs (Domestic Institutional Investors) were strong buyers to the tune of Rs 33,145 crore last week, giving strong support to the equity. Their net buying for May was Rs 67,642 crore, the highest monthly inflow since January.

After significant activity, there is expected to be muted action in the primary market next week as there will be no new public issues opening in the mainboard segment, while one public issue is lined up in the SME segment. So far, Ganga Bath Fittings is the only new IPO hitting Dalal Street next week on June 4, from the SME segment, planning to raise Rs 32.65 crore via public issue and 3B Films will close its Rs 33.75-crore offer on June 3.

On the listing front, Aegis Vopak Terminals and Schloss Bangalore will make their debut on the bourses effective June 2, followed by Prostarm Info Systems on June 3 and Scoda Tubes on June 4.

In the SME segment, the trading in Blue Water Logistics, Nikita Papers, and Astonea Labs shares will commence effective June 3, while N R Vandana Tex Industries and Neptune Petrochemicals will debut on June 4, followed by 3B Films on June 6.

Technical View

Technically, the Nifty still looks positive as it sustained well above all key moving averages (10, 20, and 50-week EMAs) and the midline of Bollinger bands, with moving averages trending upward, despite range-bound trading near the upper line of Bollinger Bands. The Bollinger bands remained in expansion mode with 25,100 (swing high) likely acting as a strong hurdle. Further, the RSI at 59.03 maintained positive crossover, though inclined downward a bit, while the MACD sustained positive crossover with the above zero line. Above 25,100, 25,200-25,500 are the levels to watch. On the flip side, 24,650 (near last week's low) can be immediate support, followed by 24,500-24,400 being a crucial support zone as below it the bears may see more action, according to experts.

F&O Cues

The weekly options data indicated that the Nifty may trade in the range of 24,400-25,000 in the short term. The 25,500 strike holds the maximum Call open interest, followed by the 25,000 and 24,800 strikes, with the maximum Call writing at the 25,500 strike, followed by the 24,800 and 25,700 strikes. On the Put side, the maximum Put open interest was seen at the 24,000 strike, followed by the 24,800 and 24,400 strikes, with the maximum Put writing at the 24,400 strike, followed by the 24,000 and 23,900 strikes.

Meanwhile, the fear index - India VIX seems to have lifted the mood at the bulls' desk as it fell 6.95 percent during the last week to 16.08 levels. If the VIX drops and sustains below 15 mark, the bulls will enter into a comfort zone.

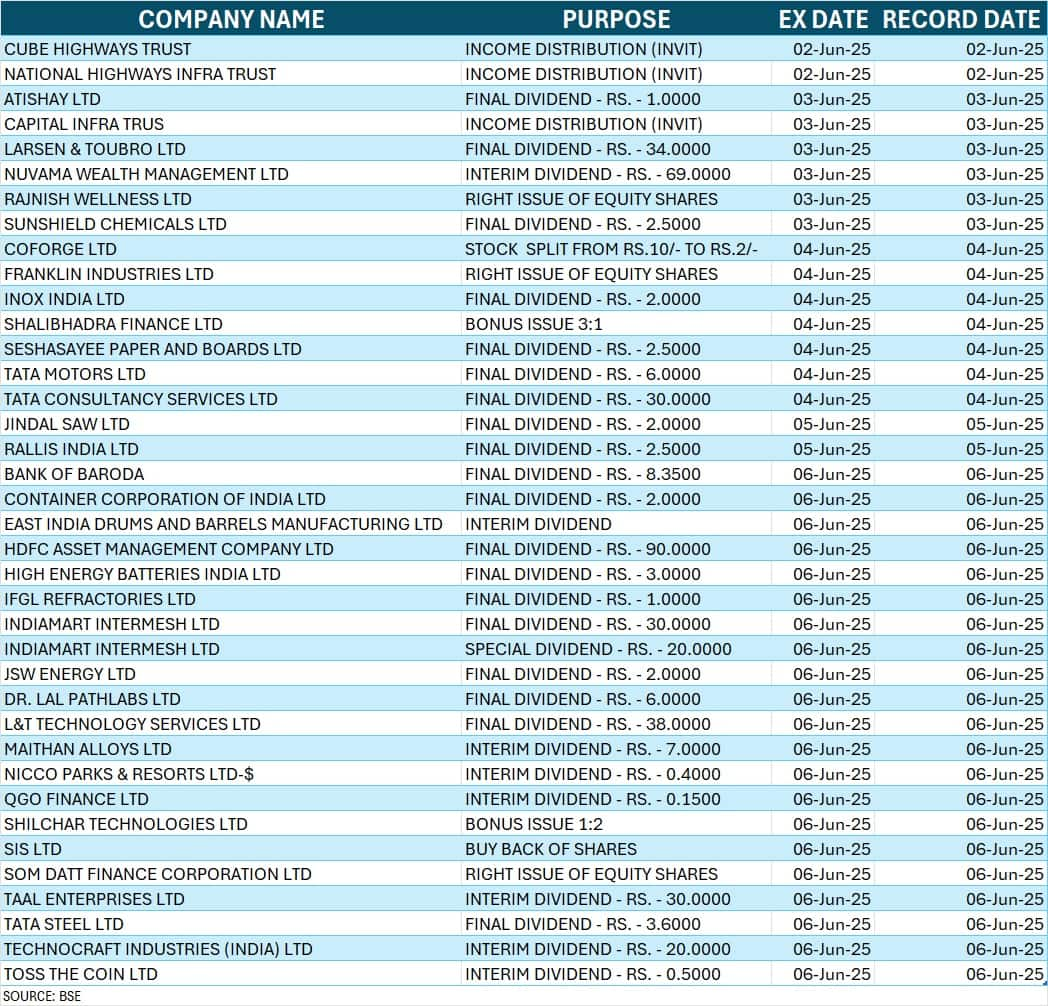

Corporate Action

Here are the key corporate actions taking place in the coming week:

Disclaimer: The views and investment tips expressed by experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.