The market closed moderately lower after a volatile truncated week ending April 11. The week was started off with a big crash after assessing the impact of higher-than-expected reciprocal tariffs imposed by US on all trade partners, however, in later part of the week, Mr Donald Trump's decision to pause tariffs for 90 days for all except China provided relief and helped the benchmark indices recouped most of those losses.

In the coming holiday-shortened week, the market is expected to maintain caution given the subdued start to the earnings season by TCS with reporting lower-than-expected numbers and acknowledging impact of trade tensions, and ongoing trade war between world's largest countries US and China. Apart from that, the participants will focus on quarterly earnings, inflation, China's GDP numbers, and ECB interest rate decision scheduled next week.

The Nifty 50 fell 76 points to finish the week at 22,829 after recouping nearly 1,100 points from last Monday's low and the BSE Sensex declined 207 points to end at 75,157. The Nifty Midcap 100 index was down 0.3 percent and Smallcap 100 index gained 0.13 percent. Most beaten down sectors like technology, metal, and capital goods saw a relief rally.

"The upcoming holiday-shortened week will remain sensitive to further developments on the US-China tariff front," said Ajit Mishra – SVP, Research at Religare Broking.

Siddhartha Khemka, Head - Research, Wealth Management at Motilal Oswal Financial Services expects the Indian markets to remain volatile, tracking global market cues, developments on the US tariffs and the Q4 corporate earnings announcements.

The market will remain shut on April 14 for Dr Baba Saheb Ambedkar Jayanti, and April 18 for Good Friday.

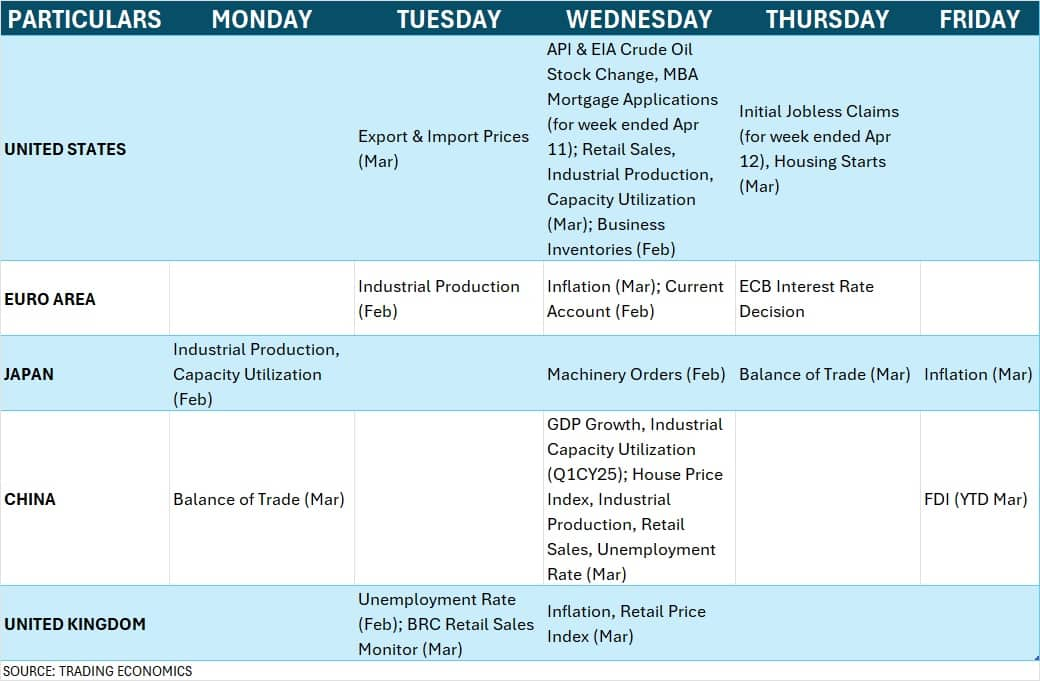

Here are 10 key factors to watch out for next week:

The corporate earnings season will gradually be in full swing in the coming week as top IT companies (Infosys, Wipro) and banks (HDFC Bank, ICICI Bank) along with HDFC Life Insurance Company will release their March quarter numbers.

In addition, HDFC Asset Management Company, ICICI Lombard General Insurance Company, ICICI Prudential Life Insurance Company, Tata Elxsi, Mastek, Indian Renewable Energy Development Agency, Angel One, Waaree Renewable Technologies, Indosolar, Mahindra EPC Irrigation, Network 18 Media & Investments, and Yes Bank will also announce their quarterly earnings next week.

Hence, the stock-specific action is likely to be seen. Vinod Nair believes the market has entered the result season with a subdued expectation. "The initial results from the IT major TCS acknowledge the impact of trade tensions and expect a delay in discretionary spending," he said.

Tariff Developments

Globally investors will keep an eye on the US tariff developments given the US-China trade war intensified, though the unexpected 90-day pause in imposition of reciprocal tariffs on all trade partners except China announced by the Trump smoothened market sentiments.

The markets are still worried about global growth given the US and China imposed high tariffs on each other last week, but are also somewhat hopeful that the most countries can manage to reach trade deal with the US through negotiations within 90 days.

The Trump raised the tariff rate on Chinese goods to 145 percent while exempting smartphones, computers, and other tech devices and components from reciprocal tariffs (giving a relief for Apple Inc). However, as a revenge, China increased tariff rate on all US products to 125 percent, signalling endless trade war until they amicably solve the issue through negotiations.

"The intensity of the US-China trade war will be crucially viewed by the market, which can have the potential to offset the impact of the current pause on trade tariffs on other emerging markets," Vinod Nair said.

He further said also the focus would be on the outcome of the ongoing bilateral trade negotiations between India and the US, which will add more colour to the trade potential of the domestic market.

Jerome Powell Speech

The market participants will also focus on the speech by Fed Chair Jerome Powell scheduled on April 16 as well as other FOMC officials during the coming week, to know about further rate cut cycle path amid ongoing tariff war. After the intensified trade war, Powell in his latest speech in early part of this month said the Fed was well positioned to wait for greater clarity before considering any adjustments to its policy stance. "It is too soon to say what will be the appropriate path for monetary policy."

Apart from that the weekly US jobs data, and retail sales & industrial production numbers for March will also be watched.

ECB Meet, China GDP & other Global Economic Data

Further, the focus will also be on the ECB meet outcome and first quarter GDP numbers from China along with March inflation data by Eurozone scheduled next week. European Central Bank is most likely to reduce deposit facility rate by another 25 bps to 2.25 percent given the growth concerns and rising global trade tensions.

Considering the escalating trade tensions with the US, recent Reuters poll suggested that the China's GDP growth in expected to slow down to 5.1 percent in Q1-CY25 from 5.4 percent in Q4-2024.

Inflation

Back home, the market participants will keep an eye on inflation numbers for March due on April 15, which are either steady or moderate compared to 3.61 percent seen in February. "We expect inflation is likely to moderate further on account of cooling food prices and would give room for RBI to remain accommodative," Vinod Nair said.

On April 18, the foreign exchange reserves for week ended April 11 and passenger vehicle sales data for March will be released.

Oil Prices

The movement in oil prices will also be watched as the Brent crude futures dropped to nearly four-year low last week amid rising trade tensions (between US and China) and fear of global economic slowdown, before recouping losses and closing 1.25 percent lower at $64.76 a barrel for the week. The downtrend in oil prices is always favourable for importers like India as it provided good support to the Indian equity markets. Generally it not only lowers the impact on several companies' balance sheets but also reduces the fiscal deficit risk. Technically, the prices traded well below all key moving averages (10, 20, 50, 100 and 200-week EMAs) and also these EMAs trending down, signalling weakness.

Adding to the bearish outlook, the Energy Information Administration (EIA) has slashed its global oil demand by 4 lakh barrels per day to 9 lakh barrels per day for 2025 citing trade war. The upcoming OPEC+ meeting on May 5 could prove decisive, signalling appetite to intervene in support of market stability. "The short-term trend looks bearish, but subject to change on any news of US-China engaging in trade negotiations and China injecting stimulus," said Mohammed Imran – Research Analyst at Mirae Asset Sharekhan.

Further, the market participants will also focus on the activity at the foreign institutional investors (FIIs) desk as they remained net sellers throughout the current month due to Trump's tariff war, net offloading Rs 34,641.79 crore worth of shares in the cash segment (as per provisional data). If they continue selling in India, the market upside may be capped until they reverse their flow, though DIIs (domestic institutional investors) sustained their strong support. DIIs net bought Rs 27,588.18 crore worth shares during the month.

Meanwhile, the US dollar index closed below 100 mark after a long time as foreign investors sold US assets due to protectionist policies announced by Trump. The fear of growth slowdown also weighed on the sentiment. The DXY fell 3.02 percent for the week to 99.783, the lowest closing level since March 28, 2022. However, US 10-year Treasury yield rebounded sharply during the week, rising 12.42 percent to finish at 4.497 percent against 4 percent in previous week, forming the large bullish candle on the weekly charts.

Technical View

Technically, the Nifty 50 managed to defend 100-week EMA on closing basis with the formation of long bullish candle on the weekly charts, which is positive sign, but lower highs-lower lows formation for another week and trading below short-to-medium moving averages (5, 10, 20 and 50-week EMAs) indicated bearish trend for the short term. Further, the index also failed to close above its 20-day EMA, while momentum indicators and oscillators are suggesting a lack of clear directional bias, hence the index is likely to consolidate in the coming week. According to experts, 22,900 is immediate hurdle for the index as above it 23,000-23,050 zone (which coincides with 50-day EMA) can be possible, however, the immediate support is placed at the 22,700 followed by 22,550 and then 22,250.

F&O Cues

According to weekly options data, the 23,000 is likely to be resistance for the Nifty 50, while the support is placed at 22,500. On the Call side, the maximum Call open interest was observed at the 23,500 strike, followed by the 23,000 and 23,800 strikes, with the maximum Call writing at the 23,500 strike, and then the 22,900 and 22,800 strikes. On the Put side, the 22,500 strike holds the maximum open interest, followed by the 22,800 and 22,400 strikes, with the maximum writing at the 22,800 strike and then the 22,900 and 23,000 strikes.

Meanwhile, the India VIX, the fear factor, remained on the higher side and closed above 20 mark, signalling the caution for bulls. It was down by 6.17 percent for the week at 20.11.

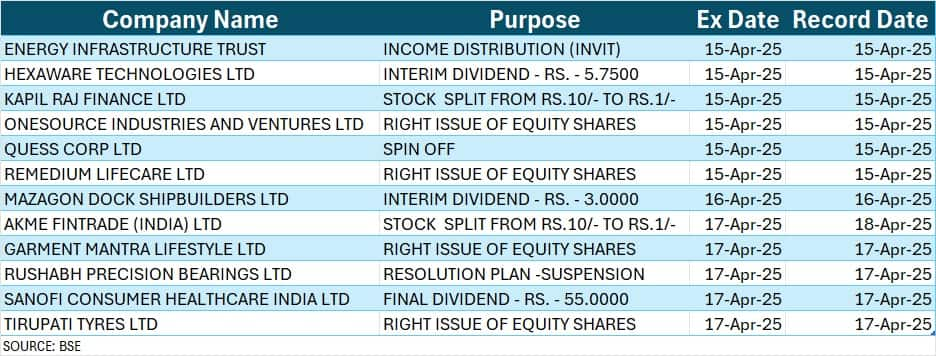

Corporate Action

Here are key corporate actions taking place next week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.