The market saw some profit booking amid consolidation, falling 0.7 percent for the week ended July 4 after rising nearly 4 percent in the previous couple of weeks, while the subdued VIX remained supportive.

The market participants looked cautious ahead of the US tariff deadline ending this week and possible tariff-related announcements by the Trump administration; however, it ignored the Jane Street issue, wherein the SEBI has temporarily barred Jane Street from trading in the Indian stock market.

The ongoing consolidation is expected to continue this week too, starting from July 7 as the market would like to get clarity over the trade deals by the Trump administration. Further, the stock-specific action will be seen as the companies have been releasing provisional business updates ahead of the June quarter earnings season starting this week, according to experts.

The Nifty 50 fell by 177 points to 25,461, and the BSE Sensex shed 626 points to 83,433, while the Nifty Midcap and Smallcap 100 indices gained 0.5 percent and 0.3 percent, respectively during the last week.

Overall, Siddhartha Khemka, Head - Research, Wealth Management at Motilal Oswal Financial Services, expects the market to remain in consolidation mode, awaiting clarity on the India-US trade deal.

"A positive outcome from the US-India trade negotiations could further lift market sentiment, particularly benefiting trade-sensitive sectors like IT, pharma, and auto," Vinod Nair, Head of Research at Geojit Investments, said.

Considering the broader indices currently trading at elevated levels, the market participants will closely watch for signs of earnings catch-up from upcoming Q1FY26 numbers, he added.

According to Siddhartha Khemka, the early onset and strong progress of the 2025 southwest monsoon has provided a timely boost to the agricultural sector, which is likely to drive rural demand, agri-input consumption, and broader economic recovery in the coming quarters.

Here are 10 key factors to watch this week:

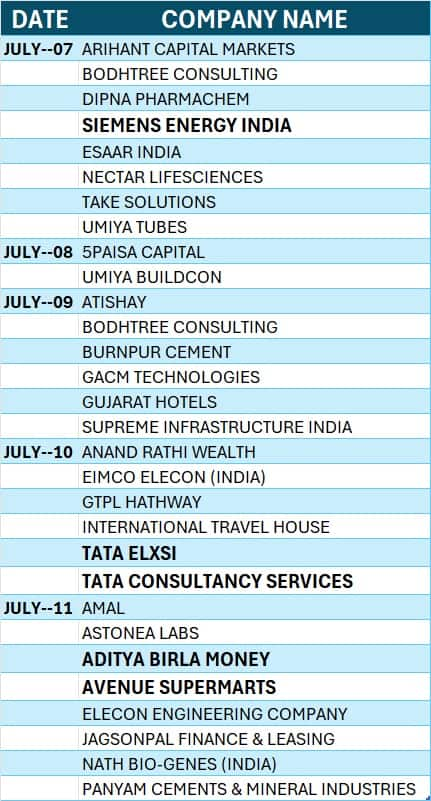

The market participants will focus on the much-awaited corporate earnings season (April-June quarter 2025) that will kick off this week with the TCS, Avenue Supermarts, Tata Elxsi, Siemens Energy India, and Aditya Birla Money.

Most experts are betting big on this quarterly earnings season as they hope that numbers and management commentaries may show strong revival signs for the year ahead and hopefully get the chance to revise the earnings upward from the current projection of 12-13 percent full-year growth. Some of the reasons behind their hope are the significant tax changes in the Budget, interest rate cuts by the RBI, easing geopolitical tensions, and increasing government capex.

Trump Tariff Developments

Globally, the most important factor to watch will be Trump’s action after July 9 — the date when the 90-day pause on significant reciprocal tariff rates for all trade partners, announced in April this year, comes to an end. Further, any revision in tariff rates, the fixing of baseline rates, and potential announcements regarding the conclusion of trade deals by the United States with various partners will also be watched.

According to the latest reports, President Trump has threatened to impose tariffs of “30 percent or 35 percent” on Japan if a trade deal is not finalised by the July 9 deadline. While agreements have been reached with the UK, China, and Vietnam, a deal with India appears imminent. The European Union may also soon announce a basic agreement to avoid new tariffs.

Kaynat Chainwala of Kotak Securities noted that caution may persist, as Trump is expected to announce tariff notices on 12 countries this Monday (July 7), with some levies potentially reaching as high as 70 percent. Most of these tariffs are expected to take effect by August 1.

In addition, she said, “The US has threatened to impose 17 percent tariffs on European Union agricultural exports, escalating trade tensions just ahead of the deadline, while optimism for deals with Japan and South Korea is fading.”

FOMC Minutes

Further, the market will look for cues from the minutes of the last Federal Reserve policy meeting held in June month. The said meeting and several Fed officials speeches signalled caution about further rate cuts citing the possible tariff rates-led inflation risks, while the strong labour data indicated that there is no need for immediate Fed funds rate cut. Still some experts expect the possible rate cut in July or September given the mounting pressure from the US President Donald Trump.

The federal funds rate was unchanged at 4.25-4.50 percent for fourth consecutive meeting in June. "The unemployment rate remains low, and labour market conditions remain solid. Inflation remains somewhat elevated. Uncertainty about the economic outlook has diminished but remains elevated," the Fed had said in its policy note after the June meeting.

Global Economic Data

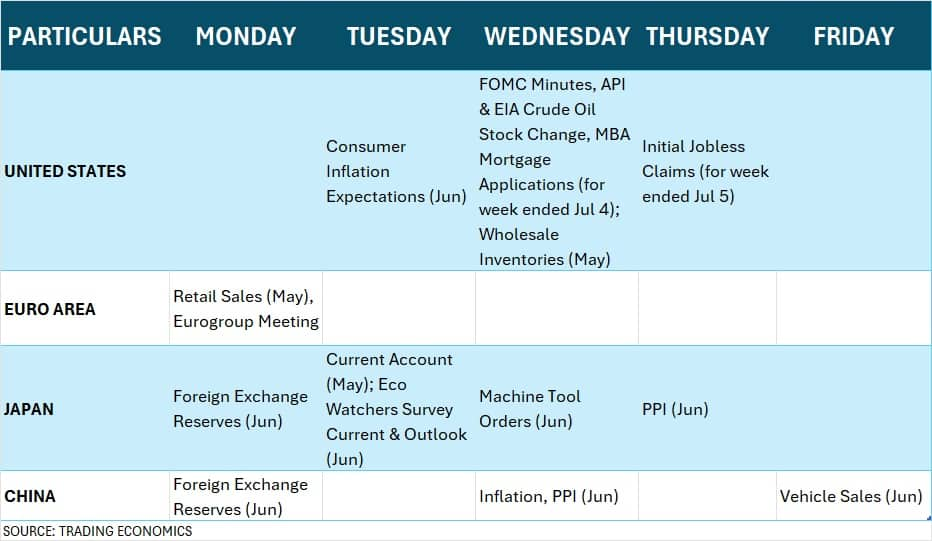

Apart from FOMC minutes, the US weekly jobs data and consumer inflation expectations for June month will also be watched this week. Further, the focus will also be on Europe's monthly retail sales data, Japan's PPI, along with China's inflation, and PPI numbers.

Oil Prices

The focus will also be on the oil prices, which remain favourable for net importers like India, especially after the OPEC+ meeting concluded over the last weekend, and ahead of Trump's fresh action on tariff rates this week. "Oil prices may come under pressure as OPEC+ agreed to a larger-than-expected production increase of 5,48,000 barrels per day for August, well above the 4,11,000 bpd added in each of the past three months," Kaynat Chainwala said.

Brent crude futures, the international benchmark for oil prices, rebounded by 3 percent to finish the week at $68.8 a barrel, after more than 13 percent correction in the previous week. Prices were supported by stronger-than-expected US and Chinese economic data, but gains were modest amid pressure from renewed US tariff threats.

Back home, the market participants will also focus on the mood at the desk of Foreign Institutional Investors (FIIs). There has still been volatility in their flow as last week (June 30-July 4 or the first week of July), they turned net sellers to the tune of Rs 6,605 crore in the cash segment (amid elevated market valuations) after their buying in previous week and previous couple of months. However, Domestic Institutional Investors (DIIs) continued to compensate the FII outflow by net buying of Rs 7,609 crore worth shares during the last week, and sustained their strong net monthly purchases since August 2023.

Going forward, "resumption of FII buying will hinge on two things: One, if a trade deal happens between India and US that will be positive for markets and FII flows; two, Q1FY26 result indications," Vijayakumar, Chief Investment Strategist at Geojit Investments said.

Meanwhile, the US dollar index continued to trend down for another week, falling by 0.28 percent last week to 96.985, the lowest closing level since February 2022, however, for the month, it was marginally up by 0.21 percent after falling 12.15 percent (during January-June) from its current year's high of 110.176 in January amid US fiscal deficit concerns, the Donald Trump's America first approach to foreign policies, increasing tariff rates and pressure on Federal Reserve to cut rates.

The primary market action will remain strong in the coming week with six new initial public offerings (IPOs) hitting Dalal Street. The list includes two from the mainboard segment: Travel Food Services' Rs 2,000-crore IPO will open on July 7, followed by Smartworks Coworking Spaces' IPO on July 10.

In the SME segment, Smarten Power Systems, and Chemkart India will launch their Rs 50-crore and Rs 80-crore worth public issues, respectively on July 7. This follows GLEN Industries' Rs 63-crore initial share sale on July 8, and Asston Pharmaceuticals' Rs 27.6-crore IPO on July 9. Also, there will be one follow-on public offering worth Rs 87.8-crore from the listed entity - CFF FLuid Control, opening on July 9.

Further, Cryogenic OGS and Happy Square Outsourcing Services will close their IPOs on July 7, followed by their listing scheduled on July 10. Meta Infotech will close its public offer on July 8 and make its debut on July 11. On July 7, investors will see a total of five companies listing on the bourses - Marc Loire Fashions, Vandan Foods, Pushpa Jewellers, Cedaar Textile, and Silky Overseas.

In the mainboard segment, Crizac is the only company listed on the bourses this week, on July 9.

Technical View

Technically, in the last week, the Nifty 50 ranged at 25,300-25,700, which is broadly in the previous week's range, signalling indecision and lack of clear directional strength. In the coming week, if the index decisively breaks 25,300 (which also coincides with the 78.6 percent Fibonacci retracement from a record high of 26,277 to April low of 21,744), the next support is placed at 25,200 as breaking of it can drive the index down toward 25,000-24,800 zone, however, sustaining above 25,600-25,700 on the higher size can open door of 25,800-26,000 levels, according to experts. The MACD still sustained well above the zero line with an upward bias, and the Stochastic RSI sustained positive crossovers on the weekly charts. The RSI still sustained above 60 at the 62.4 zone, though tilted down last week.

F&O Cues

The weekly options data suggested the broader range for the Nifty at 25,000-26,000 and the 25,200-25,700 will be the immediate range. The maximum Call open interest was placed at the 26,000 strike, followed by the 25,500 and 25,700 strikes, with the maximum Call writing at the 26,000 strike, followed by the 26,200 and 25,700 strikes. On the Put side, the 25,000 strike holds the maximum Put open interest followed by the 25,200 and 25,400 strikes, with the maximum Put writing at the 25,200 strike, followed by the 25,300 and 25,400 strikes.

Meanwhile, the India VIX, the fear index, maintained downward journey for third consecutive week and sustained below all key moving averages, giving the comfort for bulls. It fell by 0.59 percent during the week to 12.32, the lowest closing level since September 2024.

Corporate Action, Domestic Economic Data

Here are key corporate actions taking place in the coming week:

The foreign exchange reserves for the week ending July 4 will be released this week on July 11. In the previous week ended June 27, foreign exchange reserves jumped to $702.78 billion, up from $697.94 billion in the earlier week.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.