to 24,631, and the BSE Sensex climbed 740 points (0.93 percent) to 80,598, while the Nifty Midcap and Smallcap 100 indices gained 0.9 percent and 0.7 percent, respectively.")

The market staged a healthy performance for the truncated week ended August 14 after a six-week losing streak, recording a 1 percent rally backed by robust DIIs inflow. In fact, it was a kind of relief rally, especially after the nervousness driven by Trump's tariffs. Falling retail inflation to an 8-year low, subdued WPI inflation, and increasing hope for a Fed funds rate cut in the September policy meeting boosted market sentiment.

On Monday, the market may react to the Trump-Putin meeting in Alaska that concluded with no deal to end the war between Russia and Ukraine (though both signalled positive progress), and the expected changes in GST rate structure to boost consumption and growth signalled by Prime Minister Narendra Modi in his Independence Day Speech last week.

The market is expected to be consolidative and rangebound until it sees a strong follow-up buying interest this week, starting from August 18, with focus more on global cues, including the Jackson Hole Symposium, FOMC minutes, due to the absence of a domestic trigger. Tarriff-related developments, if any, could also be watched, while the S&P’s upgrade of India’s sovereign credit rating (after 18 years) to BBB with a stable outlook is expected to support the market, according to experts.

The Nifty 50 rallied 268 points (1.1 percent) to 24,631, and the BSE Sensex climbed 740 points (0.93 percent) to 80,598, while the Nifty Midcap and Smallcap 100 indices gained 0.9 percent and 0.7 percent, respectively.

With the end of the Q1 earnings season, investor focus would shift towards the upcoming geopolitical developments, while markets would likely remain in a consolidation mode, said Siddhartha Khemka, Head of Research, Wealth Management at Motilal Oswal Financial Services.

According to Vinod Nair, Head of Research at Geojit Investments, global cues remain positive due to softer US inflation data and a fall in the US 10-year bond yield, reflecting conviction for a Fed rate cut in the September policy meeting.

In the near term, stock-specific movements are likely to persist with attention toward domestic consumption-led sectors to beat volatility. The geopolitical developments could act as a catalyst for near-term market sentiment, he said.

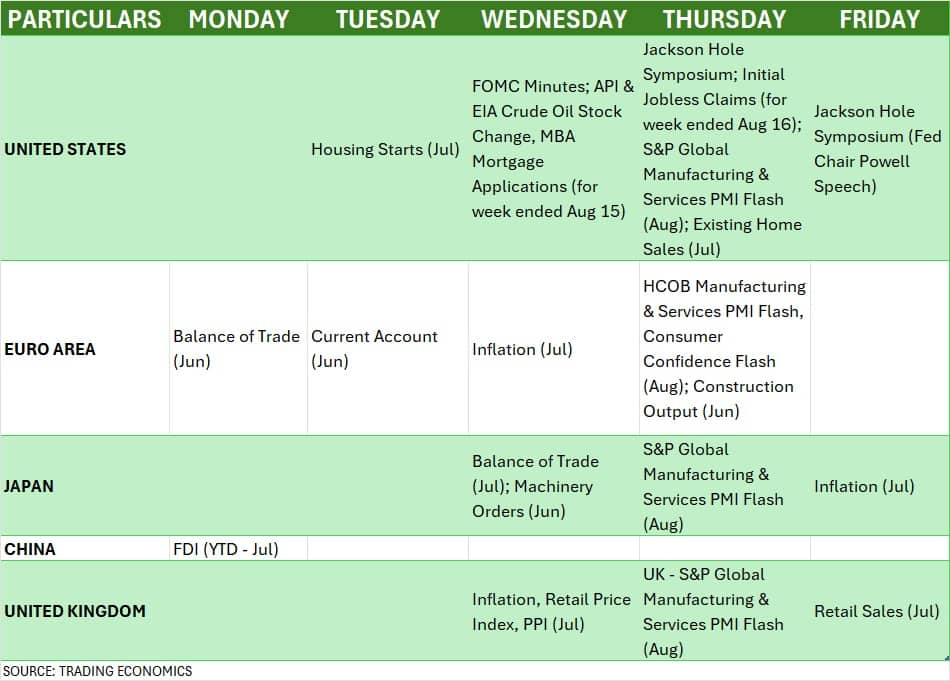

Here are 10 key factors to watch this week:

Jackson Hole Symposium

Globally, the focus would be on the Jackson Hole Symposium, the annual economic policy symposium scheduled to be held in Jackson Hole, Wyoming, during August 21-23. Central bankers, policymakers, and economists from around the world will be attending this symposium. This will be the first economic policy symposium after the US President Donald Trump kicked off his tariff war with its trade partners.

This year’s theme is 'Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy', the Federal Reserve Bank of Kansas City portal showed.

The most noteworthy factor to watch will be the speech by US Federal Reserve Chair Jerome Powell scheduled for the evening on August 22. Further rate cut path, comments on the economic progress and jobs data, especially after Trump tariffs, are some of the factors to watch in his speech. Powell has been getting consistent pressure from the Trump administration to cut rates, but he is worried about the impact of recent tariffs on the US economy and a possible increase in inflation.

FOMC Minutes

The second factor to watch would be the minutes of the FOMC's monetary policy meeting held in July, which will be released on August 20. In the said meeting, the Federal Reserve kept rates unchanged at 4.25-4.50 percent for the fifth consecutive meeting amid fears that the ongoing tariff war may push inflation higher, and saw a moderation in economic activity in the first half of 2025, though the unemployment rate remains low.

Global Economic Data

Apart from the Jackson Hole Symposium and FOMC minutes, the market participants will also keep an eye on the monthly housing starts, existing home sales, and weekly jobs data from the United States.

Also, the manufacturing and services PMI flash data for August by several nations, including the US, Europe, and Japan, will also be watched. Further, inflation numbers for July will also be released by Europe, Japan, and the UK this week.

India meets with officials from China and Russia

Back home, the focus would be on the Indian government's high-level meetings with China and Russia scheduled this week, which are important, especially after Trump imposed 50 percent tariffs on Indian goods.

According to media reports, Chinese Foreign Minister Wang Yi is slated to visit India on August 18 for talks under the Special Representatives (SR) mechanism, while India’s External Affairs Minister will be visiting Russia, meeting Russian counterpart Sergey Lavrov on August 21, which will be important to watch especially before the Russia-India annual summit for which President Vladimir Putin is likely to visit India in the final quarter of this calendar year.

Domestic Economic Data

On the economic data front, the unemployment rate for July will be released on August 18, which may decline from 5.6 percent seen in the previous month.

HSBC Manufacturing and Services PMI flash data for August will also be out this week on August 21. In July, Manufacturing and Services PMI increased to 59.1 and 60.5 in July, up from 58.4 and 60.4 in the previous month.

Foreign exchange reserves for the week ending August 15 will also be released on August 22.

Further, the mood at Foreign Institutional Investors' desk will also be checked by the market participants this week as they remained net sellers last week and current month, to the tune of Rs 10,173 crore, and Rs 24,192 crore, respectively, especially after Trump's tariffs, mixed earnings growth, and elevated valuations. In fact, this is the second consecutive month when they are net sellers after net buying in the previous four months.

According to experts, going forward, further tariff-related developments will influence the FII activity, though S&P's rating upgrade on India provided a positive signal to FIIs.

On the other side, Domestic Institutional Investors (DIIs) continued to lend robust support to the equity, net buying Rs 19,000 crore worth shares last week and Rs 55,795 crore net purchases in the current month. In fact, they maintained buy on dips strategy given the expected healthy economic growth, and recovery in earnings from second half of FY26.

On the primary market front, participants will see eight new IPOs worth Rs 3,724 crore hitting Dalal Street this week, including five from the mainboard segment worth Rs 3,584 crore.

In the mainboard segment, Vikram Solar (the largest amongst them), Gem Aromatics, Patel Retail, and Shreeji Shipping Global will be launching their public issues on August 19, followed by Mangal Electrical Industries' IPO on August 20.

In the SME segment, there will be three maiden public issues - Studio LSD, LGT Business Connextions, and Classic Electrodes (India) this week, opening for subscription on August 18, August 19, and August 22, respectively.

On the listing front, seven companies - BlueStone Jewellery & Lifestyle, Regaal Resources, Star Imaging & Path Lab, Medistep Healthcare, ANB Metal Cast, Icodex Publishing Solutions, and Mahendra Realtors & Infrastructure will debut on the bourses this week.

Technical View

Technically, the market is still looking weak as the benchmark Nifty 50 traded below the 10-week EMA on the weekly charts, though it formed a Tweezer Bottom kind of bullish reversal pattern, which needs strong follow-up buying this week for confirmation. The momentum indicator RSI inched up last week but still maintained a bearish crossover. The MACD still has a bearish crossover with further weakness in the histogram. Until the index surpasses and holds above short-term moving averages, the consolidation may continue with support at the 24,350-24,300 zone as below it, the bears may tighten their grip; however, on the higher side, 24,750-24,800 are expected to be key hurdles, as sustaining above it can open doors for a strong rally, experts said.

F&O Cues

The weekly options data also suggested that the 24,700-24,800 is expected to be immediate hurdle for the Nifty 50, followed by 25,000 where the maximum Call open interest and writing is placed, however, the 24,600-24,500 is likely to be immediate support, followed by 24,000 being crucial support, where the maximum Put open interest and writing were seen.

Meanwhile, the India VIX, the fear index, has been inching higher for the third consecutive week, which signals caution for bulls. It was up by 2.68 percent last week to 12.36 zone, taking the total rally to 9.6 percent in the last three weeks.

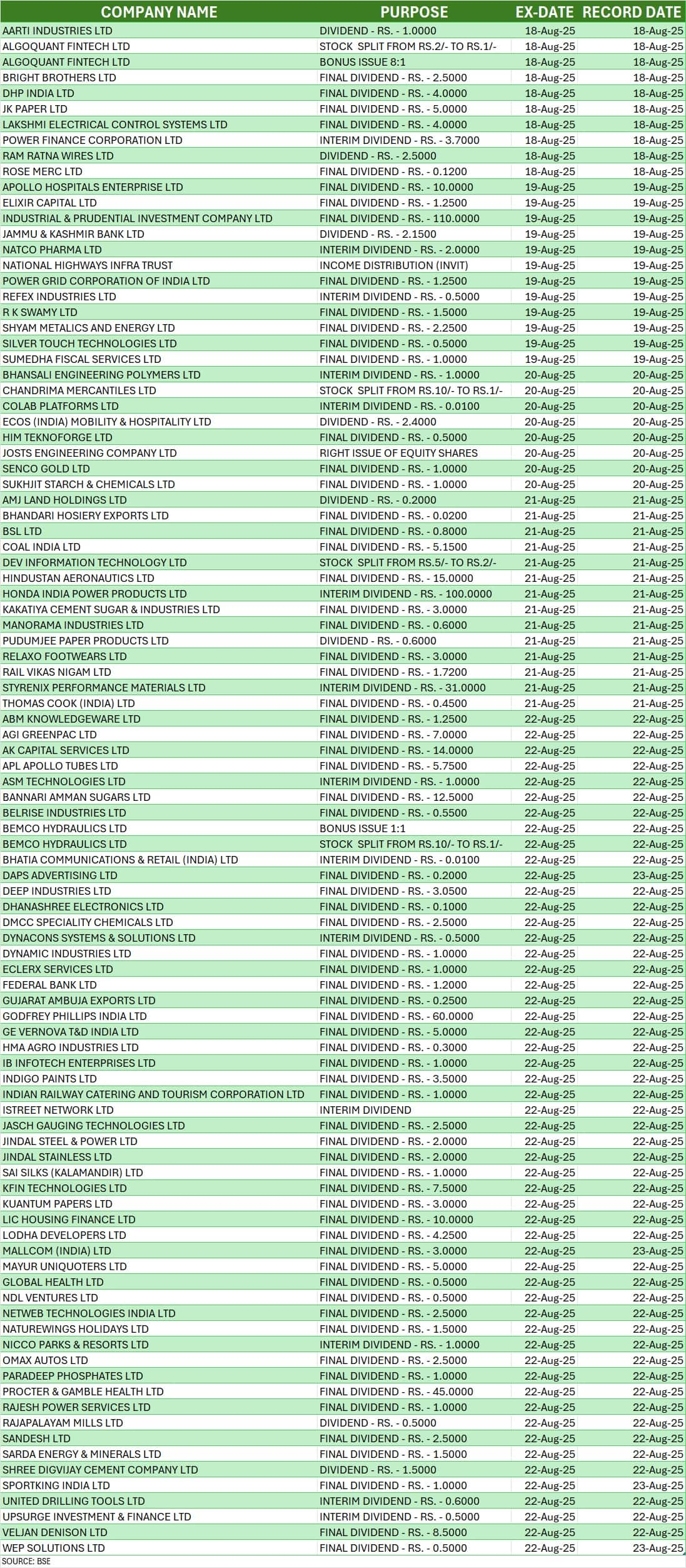

Corporate Action

Here are key corporate actions taking place this week:

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.